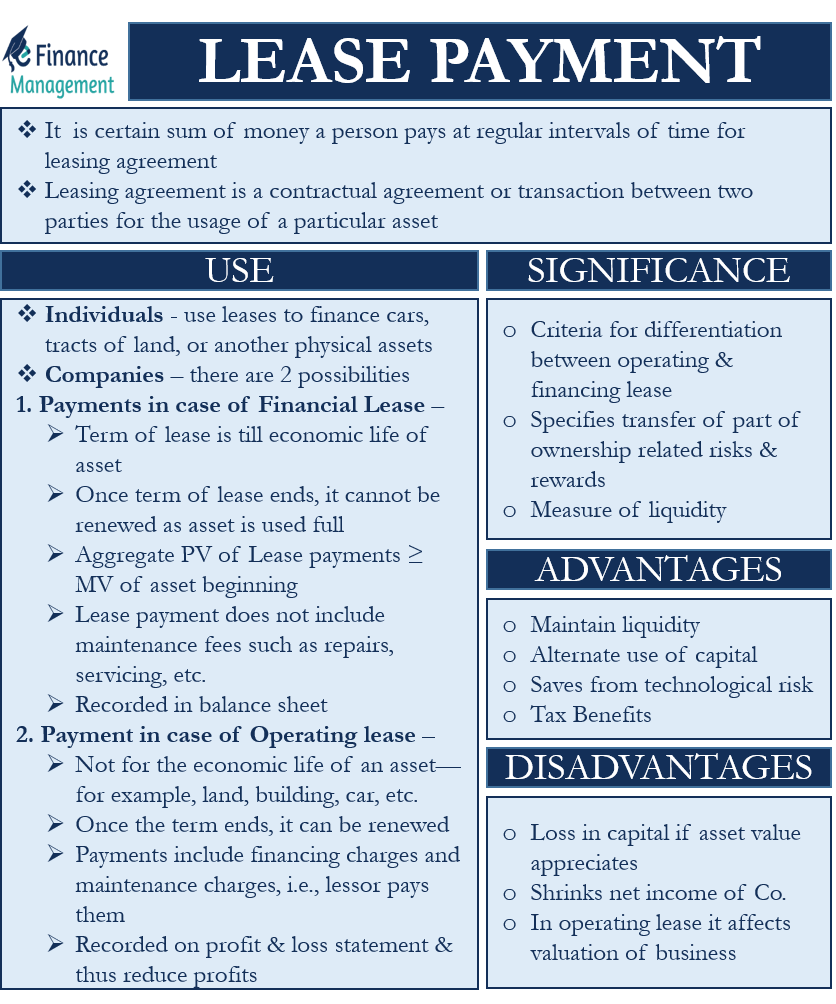

What is Lease Payment?

Lease payment is a certain sum of money that a person pays at regular intervals of time for a leasing agreement. The regular interval is mostly a month.

Factors considered to decide lease payments include assets value, local market value, discount rates, a lessee’s credit score, depreciation fee, finance fee ( interest on a loan), and tax.

Further explaining the leasing agreement, it is a contractual agreement or transaction between two parties for the usage of a particular asset. The party owning the asset is the lessor. He provides the asset for use to another person called the lessee. Lessor does not transfer the ownership of an asset. As a result, at the end of the leasing period, the asset returns back to the lessor. There may be a provision of extension for lease. Indeed, the lease payments may increase in such cases.

Lease rentals or Lease payments are considerations that the lessee pays to the lessor for the lease transaction. Structured lease rentals compensate the lessor in the form of depreciation. The compensation is for the investment made in assets & for expenses like interest on investment, repairs, and service charges borne by the lessor over the lease period.

Also Read: Finance / Capital Lease

Lease rentals are different from rent paid in the case of rental agreements. (Click here to read more)

Different types of lease agreements from a base to structure lease payments. Accounting of Capital lease payments is different from the accounting of Operating lease.

Breaking down Lease payment

Individuals

They mostly use leases to finance cars, Tracts of land, or another physical asset.

Companies

In the case of Lease payment of a company, there are two possibilities:

Payments in case of Financial Lease.

Here the term of the lease is till the economic life of an asset, for Example, Heavy machinery, aircraft, and Railway wagons. Once the term of the lease ends, it cannot be renewed as the asset is used fully.

In this case, the present value of minimum lease payments throughout the leasing period is greater than or equal to the market value of the asset at the beginning of the lease period.

i.e., Aggregate PV of Lease payments ≥ MV of asset beginning. So, the lessor gets full value for the assets given. Because when the asset returns to him, he may not be able to generate further money from it.

Also Read: Lease Finance vs. Installment Sale

Here, Lease payment does not include maintenance fees such as repairs, servicing, etc., i.e., the lessee has to pay them. Generally, payments made under such leasing options are recorded in the balance sheet. Hence, they do not reduce profits.

Payment in case of Operating lease.

The term of the lease is not for the economic life of an asset—for example, land, building, car, etc. Once the term ends, it can be renewed.

Such payments include financing charges and maintenance charges, i.e., the lessor pays them. Lease payments made for a capital lease go on the Profit & loss statement and thus reduce profits.

Significance

Lease payments are one of the many criteria based on which Operating lease & Financial lease are differentiated.

For instance, a lease is called a finance lease if it transfers substantially all risks & rewards related to ownership. Likewise, if it does not transfer, it becomes an operating lease. If on a scale, the transfer of risk & reward is towards 0%, it is an operating lease, and if it is towards 100%, it is a financial risk.

Now, what role does lease payments play here?

The IAS 17 specifies that the transfer of an important part of ownership related risks and rewards takes place when the payments are made over a non-cancellable lease period. The total payments are sufficient to amortize the capital outlay of the lessor. Also, leave some profit. To clarify, PV Lease payments ≥ cost of equipment. The cutoff point is when the present value is> 90% fair market value of the equipment.

Further, the calculation of the company’s fixed charge covering ratio includes lease payments. This ratio is a measure of liquidity.

Advantages

Maintain Liquidity

Lease rentals do not burden the financial statements. One-time payment is not made & the cost is spread over a long period of time.

Alternate use of capital

When one goes for leasing, he saves the capital and can put it to other next best alternative.

Saves from technological Risk

A company safeguards itself from investing heavily in technology that can be obsolete anytime in the near future.

Tax Benefits of Lease Payments

- To lessor: The greatest advantage of the lessor is tax relief by way of depreciation. When the lessor is in a high tax bracket, he may give assets on lease with increased depreciation rates. Hence, it reduces his tax liability substantially. The rentals may be lowered to pass the part of the tax benefit to the lessee If the lessor is in the tax paying position. Thus, adjusting rentals suitably postpones taxes.

- To lessee: By suitable structuring of lease payments, many tax advantages can be obtained. The rental may be increased to lower his taxable income if the lessee is in a tax-paying position. The cost of an asset is thus amortized more rapidly than in the case where the asset is owned by the lessee because depreciation is allowable at prescribed rates.

Disadvantages

- Leasing agreements of buildings, land, etc., do not allow appreciation of the value of such assets. This may cause the business certain capital losses if the market value of the asset rises.

- Lease expenses shrink the net income of a company. As a result, the income available to equity shareholders reduces.

- In the case of operating lease, rentals do not form a part of the balance sheet. It affects the valuation of the business.

Structuring of Lease Payment

Lease rentals may be structured to accommodate the cash flow position of the lessee, making the amount of rentals convenient to him. Lease rentals are so tailor-made that the lessee is capable of paying the rentals from funds created from operations. The lease term is also taken so as to suit the lessee’s ability to pay rentals and take into account the operating lifespan of the asset. Some of the approaches to structure lease rentals are illustrated underneath.

The following data relate to Hypothetical leasing Company Ltd:

- Investment cost / outflow $100,00,000

- Pre-tax required rate of return, 20% p.a

- Primary lease period, 5 years.

- Residual value (after a primary period), Nil.

ALternate payment structures:

- Equated

- Stepped (15% increase per annum)

- Ballooned (annual rental of $ 10,00,000 for years 1-4)

- Deferred (deferment period of 2 years.

Computation:

Y= equated annual rent to be charged.

Equated Annual Lease Rental

Here, equal rent is charged for all the years of the leasing term.

it is calculated by using the following formula:

Y: $ 100,00,000 = Y * PVIFA [ (@20% for 5 years i.e (20,5)]

Stepped Lease Rental

In this type of structuring, the rental is increased by a certain percentage every year. This is beneficial for the lessor as with increasing inflation. He can increase the income generated from his asset. It is calculated using the following formula:

Y: $100,00,000 = Y* PVIF (20,1) + (1.15) Y * PVIF (20,2) + (1.15)2 Y * PVIF (20,3) +(1.15)3 Y * PVIF (20,4) +(1.15)4 Y * PVIF (20,5)

Ballooned Leased Rental

In this type of structuring, the lease rentals are kept the same for all the years. But, the are increased heavily in the last years. Hence, if 100 was the value of the asset, say 25% can be spread over all years & 75% can be charged in the last year. The formula used to calculate such rental as per our illustration terms is:

Y : [10*PVIFA (20,4) + Y*PVIF (20,5)] = $100,00,000

Deferred Lease Rental

Here, the period of lease rentals does not start as soon as both parties enter into a leasing agreement. But there is a fixed interval after which the lease rentals are charged. This benefits the lessee. He has to not incur the expense immediately as he takes assets in hand. Also, when there is a long Gestation period of the benefit that the lessee receives through the use of the asset, this method is very useful. The formula to calculate lease rentals under this method, as per our illustration, would be Denoting Y as equated lease rentals charged in years 3-5.

Y: $100,00,000 = Y * PVIF (20,3) + Y * PVIF ( 20,4 ) + Y * PVIF (20,5).

Conclusion

One can choose any structure to suit the lessee & lessor with mutual understanding. This flexibility is not possible in the debt servicing model of the traditional loan, institutional borrowings, etc. Such loans have to be typically repaid over a specific number of installments resulting in heavy debt servicing burden in the earlier years of the business. In contrast, the business may actually generate substantial cash flows in later years.

Learn more about What is a Lease?