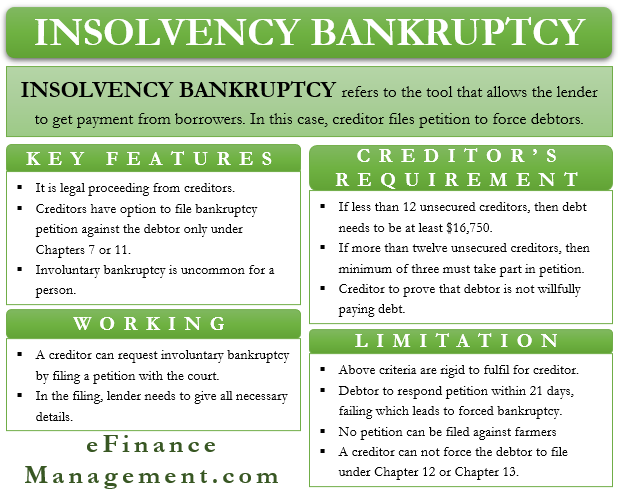

Chapter 12 Bankruptcy

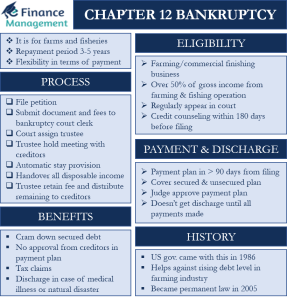

What is chapter 12 Bankruptcy?Chapter 12 bankruptcy is applicable to the farms and fisheries businesses. This means this bankruptcy assists the owners of farms… Read Article

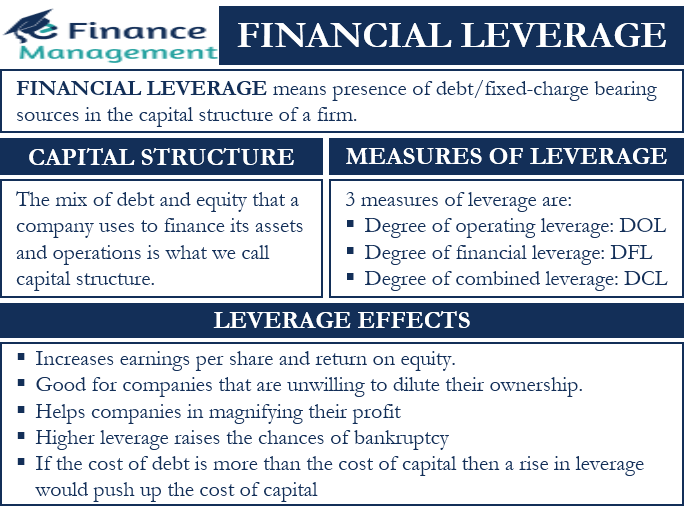

Financial leverage means the presence of debt in the capital structure of a firm. In other words, it is the existence of fixed-charge bearing capital, which may include preference shares along with debentures, term loans, etc. The objective of introducing leverage to the capital is to achieve the maximization of the wealth of the shareholder.

Financial leverage deals with profit magnification in general. It is also well known as gearing or ‘trading on equity.’ The concept of financial leverage is not just relevant to businesses, but it is equally true for individuals. Debt is an integral part of the financial planning of anybody, whether it is an individual, firm, or company. However, in this article, we will try to understand it from the business point of view. But before diving deep into the concept, let’s have a quick look at what capital structure is.

A company can use debt as well as equity in the form of capital. So, the mix of debt and equity that a company uses to finance its assets and operations is what we call capital structure. Or, we can say capital structure refers to different combinations of debt and equity that a company uses.

To learn more about it, refer to Capital Structure & its Theories. Now, let’s move further.

In a business, debt (short or long term) is acquired not only on the grounds of ‘need for capital’ but also taken to enlarge the profits accruing to the shareholders. Let’s clarify this further. An introduction of debt in the capital structure will not have an impact on the sales, operating profits, etc. But it will increase the share of profit of the equity shareholders, the ROE % (Return on Equity).

Try to understand this with the example below.

The calculation below clearly shows the effect of having debt in the capital. The table shows two options of financing, one by equity only and another by debt and equity.

| Particulars | Only Equity | Debt + Equity |

| Equity Shares of Rs. 10 Each | 5,00,000 | 2,50,000 |

| Debt @ 12 % | 2,50,000 | |

| EBIT | 1,20,000 | 1,20,000 |

| Interest | 30,000 | |

| PBT | 1,20,000 | 90,000 |

| Tax – 50% | 60,000 | 45,000 |

| PAT | 60,000 | 45,000 |

| No. of Shares | 50,000 | 25,000 |

| EPS | 1.2 | 1.8 |

| ROE | 12% | 18% |

The return on equity (ROE) and the EPS both are higher in the case of debt and equity structure. It shows that the return on equity has increased with the introduction of leverage in the capital structure.

The picture shown in the above illustration does not bring all aspects of leverage. Hence, we shall go further inside to know the reason for having higher EPS and ROE in the case of a levered firm. Let us calculate one more important ratio – ROI (Return on Investment). ROI in both the options is 24% (EBIT / Total Investment = 120000 / 500000).

Now, here we see that the ROI is more than the interest rate charged by the lender, i.e., 12%. This is the reason behind the higher EPS as well as ROE in the case of a levered firm. So, leverage would not always be profitable. The following matrix explains the behavior of levering a firm.

| Favorable | ROI > Interest rate |

| Unfavorable | ROI < Interest Rate |

| Neutral | ROI = Interest Rate |

In the current example, the first situation, i.e. ROI > Interest Rate is true, and that is why the results are favorable as we can see. If the ROI is less than the interest rate, the ROE will decline, and on the other hand, if ROI is the same as the interest rate, it will make no difference.

Going through the following points will help in understanding the effects of leverage (both positive and negative):

Too much leverage can have an adverse impact on the cost of capital as well. If the cost of debt is more than the total cost of capital, then a rise in leverage would push up the cost of capital. And, if the cost of debt is less than the total cost of capital, then taking on more debt reduces the cost of capital.

Leverage has a similar impact on ROE as it does on net income. If the sales are rising, then higher leverage would boost the ROE. Similarly, when sales are dropping, higher leverage would accelerate the drop in ROE as well.

Higher leverage raises the chances of bankruptcy. This is because higher leverage means more borrowing, as well as more interest commitments. This raises the chances of failure to honor the interest commitments. And, if the conditions aren’t favorable, it may even result in bankruptcy.

Measuring the impact of leverage means quantifying how much risk a business is experiencing due to its current capital structure. We can say that measuring the leverage shows how a company’s fixed and variable costs can affect profitability. There are three measures of leverage, and these are:

This measure shows how the changes in ROA (Return on Assets) impact the profitability of a firm. It primarily measures the operational risk. Or how sensitive a firm’s operating income is to the change in revenue. The formula to calculate this is:

| DOL = (% change in operating income) / (% change in units sold). |

A firm with more debt in its capital structure is considered riskier. This is because such companies would have more fixed commitments in the form of interest payments. Such firms are more operationally leveraged as well. The formula to calculate DFL is:

| DFL = (% change in net income) / (% change in operating income) |

As the word suggests, it is a combination of both the above leverages – operating and financial. So, we can say that it tells about a company’s overall state of leverage. It considers all financial and operational leverages to quantify a company’s overall business risk. Following is the formula to calculate DCL:

| DCL = (% change in net income) / (% change in units sold) |

Read about the Types of Leverage in detail.

There are various measures of Financial Leverage