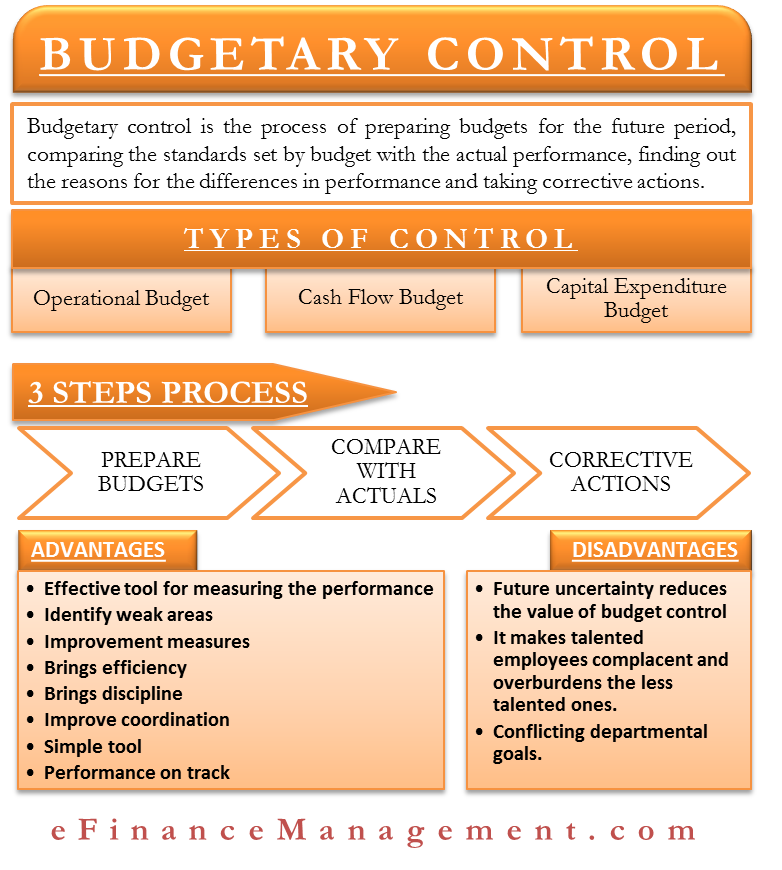

Budgetary control is the process of preparing budgets for the future period, comparing the standards set by the budget with the actual performance, finding out the reasons for the differences in performance, and taking corrective actions.

Budgetary Control Process Steps

Typically, there are 3 steps in a budget control process. These are as follows:

Prepare Budgets

First, the budget needs to be prepared. This budget is simply a set of financial goals that the management wants to achieve. E.g. the goal may be to increase sales by 12% this year. Or the goal may be to cut down the labor costs by 5% this year.

Compare with Actuals

Second, when a company gets the actual performance results, the management compares it with the performance/standards set in the budget. The goal is to find out to what extent the actual performance is in line with the budgeted performance and to what extent is the performance off-track. E.g., the company may find out that the budget goal was to increase the sales by 12%, but the sales increased by only 7%.

Corrective Actions

Third, the company analyses the reasons for the deviation in the actual performance and takes corrective actions. E.g., the company may find out that the sales didn’t increase by 12% because of the shortage of workforce faced by the sales team. So, the company takes corrective action in order to improve the performance of underperforming operations. Thus, the company may decide to increase its workforce by a certain percentage so as to achieve the desired increase in sales.

Also, read Why is Budgeting important?

Types of Budget Control

There are various types of budget controls that an organization can implement.

Operation Budget Control

Operating budget control covers the revenues and operating expenses of the firm. This budget control is important for running the day-to-day operations of the firm smoothly. Usually, firms compare the performance of this budget with the actual performance on a monthly basis since a monthly comparison enables the organization to take corrective actions in a more timely manner. This budget control helps in achieving a desired level of EBITDA – Earnings before Interest, Tax, Depreciation, and Amortization.

Cash Flow Budget Control

This budget control compares the forecasted cash inflows and cash outflows from various sources to the actual inflows and outflows of cash. This provides an important control in the organization since it ensures that the organization has enough cash to meet its requirements and obligations. Cash budget control also involves investing the excess cash available, thereby making profits out of idle cash.

Capital Expenditure Budget Control

This budget control covers capital expenditures like buying a plant or machinery. This budget control helps the organization to plan and manage its capital expenditure. Capital expenditures involve huge sums of money. So, it becomes very important to take steps that ensure that the firm makes only profitable investments and takes decisions at the right time.

Advantages of Budgetary Control

- In a budget control system, a firm assigns targets to each department, individual, etc. It then compares the budgeted performance with the actual one. The firm then reports the performance of each department to the top management. Hence, budget control serves as an effective tool for measuring the performance of departments, individuals, and cost centers.

- The difference between budgeted performance and actual performance helps the management to identify its weak areas. The firm gives special attention to such areas.

- Budget control helps the management to identify what improvement measures can be taken. E.g., an actual performance of 6% growth in sales instead of the budgeted 12% may help the management to take corrective actions such as an increase in workforce, increase in advertisement expenses, etc. If there were no budget, the corrective action would not have been taken.

- It brings efficiency (each department does its best to achieve the budgeted performance) and cost reduction by proper planning, which ultimately results in profit maximization.

- Budgetary control brings discipline to the organization. The managers perform better because they know that their performance will be measured.

- It improves coordination between different departments since the performance and results of one department are often dependent on another department. E.g., the sales department may have the target of increasing sales, and the production department may have the target of increasing production this year. Since the goal of one depends on another, this improves coordination between the two departments.

- Budget control helps the organization to understand its strengths and weaknesses simply by measuring the performance of departments, cost centers, etc., over a period of time.

- It helps the organization keep its performance on track (by comparing actual performance against budgeted ones regularly or several times a year and taking corrective actions) and achieving its long-term goals.

Disadvantages of Budgetary Control

- Organizations prepare budgets for the future period. However, the predictions of the budget may not come true. This is because the future is uncertain and the conditions which are presumed to prevail in the future may change. These change in conditions upsets the budget which is prepared on the basis of some assumptions about the future. Hence, future uncertainty reduces the value of budget control.

- Under a budgetary control system, targets are given to every person. The common tendency of people is to achieve only the targets and work nothing more. Some employees or managers may exceed the budget performance, but they feel satisfied with achieving only the targets given to them. Hence, budgetary targets may lead to under realization of employee’s potential. It makes talented employees complacent and overburdens the less talented ones.

- A budget control system may create added conflict between the departments. Every department has its own budgetary goal to achieve. The goal of one department may conflict with the goal of another department. For e.g., it may happen that the production department decides to reduce the quality of the product in order to achieve its target of cutting down production costs. But, the marketing department wants the same quality product to be manufactured. Hence, budget control may create conflict between the two departments.

- The coordination which is required between different departments is both an advantage as well as a disadvantage. It may happen that two departments may not go well with each other despite being interdependent on each other. This lack of coordination may lead to poor performance from both the departments who could have performed better individually.

Thank for this assignment .This is very helpful for me.

Thank you sir it’s really helpful for our exam. And it is understood too.