Bootstrapping: Meaning

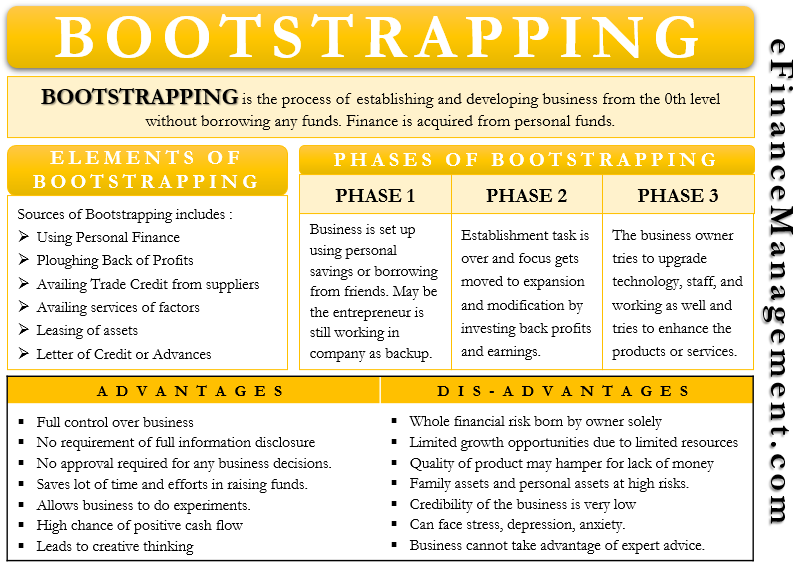

Bootstrapping is the process of establishing and developing the business from the 0th level without borrowing any funds. Here the owner of the business finances the business with their personal funds. Under no circumstances investments from investors or debt from debtors are entertained here. In rare cases, only minimal external capital is acceptable.

Under this method, whether it is an expansion or the establishment of a new outfit, financing of all such things takes place from the personal funds of the owner(s) only. Here the sources of finance are either the contribution from the owner or partners and the revenues generated from the company or personal resources (including sweat equity) of the owner; there is no other way out. Apart from cash also, there is no borrowing or any other support for the business. Bootstrapping, the source of finance is not only applicable to startups. However, any business at any point in its growth cycle can opt for this method of financing.

Understanding the term: Bootstrapping

Tracing of the term ‘Bootstrapping’ goes back to the 18th and 19th Centuries. At that point in time, the meaning of the term was some impossible assignment or unattainable task. Eventually, over the years, there has been a lot of evolution in the term. And today, it means developing and expanding business from almost nothing or without any external financial help, in the current eco-system that is slowly becoming though not impossible but difficult to execute and attain.

Various elements useful for bootstrapping

These are a few elements or areas or sources that help the business owners to manage their finances in a better efficient way and thus avoid the need for any external borrowings. Apart from personal finance and plowing back the profit, these sources are also useful for enhancing bootstrapping.

Also Read: Financing Strategies

Trade Credit

Trade Credits given by the suppliers at the time of supplying goods are the best method for managing short-term finances. This credit is given for 30, 60 days and may even stretch up to 90 to 120 days. The quantum and period of trade credit depend upon the relationship with the suppliers. Thus, businesses can avail interest-free credit (finance) for a few days to months.

However, the Trade Credit can only remain useful in the short term. The business owner ultimately has to pay the suppliers in the long term. Moreover, a huge amount of dependence on the trade credit given by a particular supplier is also not good. It has its own many shortcomings. Thus at times, this method or source can turn costly.

Factoring

It is a method where the commercial finance company buys the receivables at 80-95% of the face value of receivables. As a result of this, the business owner gets the money instantly and also has not to bear the risk of default. Even after recovering only 80-90% of the selling price, the business owner can still make profits if there is a high margin on the products.

Thus this method avoids taking debt for meeting working capital or any other short-term requirement by instantly getting the money on the one hand. On the other hand, it frees the owner to spend time and effort for recovery. Instead, he can concentrate on business growth.

Leasing

In the initial setup, the businesses would like to conserve the resources. Hence they prefer not to put a huge amount of money into arranging fixed assets like land, building, machinery, equipment, etc. Thus instead of borrowing loans and making outright purchases, they would prefer leasing these assets. And that works the best in such circumstances. The business owners take such fixed assets on leases for a long duration of time and thus avoid any interest payments or blocking large investments. In Leasing, payment is only made for the portion which is used and not for the full fixed asset.

Letter of Credit or Advances

This is another source that can loosely be referred to as self-funding. Under this, either the big customer placing a large order on a continual basis can issue a Letter of Credit in favor of the business. This Letter of Credit becomes much-needed security for various purchases required for the business. Another way is partial or full advance payment by the customers; depending upon the demand for the product and the credibility of the owner, the customers may be making advance payments to the business.

Thus, this becomes a sort of working capital financing by the customers, and the business can buy, produce and use these funds to operate the business and sell the product ultimately to the customers.

Phases of Bootstrapping

Phase 1

In the first stage, all establishment activities of business take place. Here, in the beginner’s phase, the business owner has commenced their business with personal saving money or borrowing from friends. Here it might be possible that the entrepreneur is still working in a company and starting a side business like this.

Phase 2

In the second phase, the establishment task is over. Now the business owner focuses on expansion and modification. At this stage, investing back the profits and earnings take place. After investing a lot of personal finance, the business owner now starts investing a certain portion of profits. The other name of phase 2 is the ‘Customer-funded stage.’

Phase 3

Until businesses reach this stage, it is in a good state. The business owner tries to upgrade technology, staff, and working as well. It even tries to enhance its products and services. Now looking to the potential even business would like to hire a team to manage the increased business affairs. And all that requires a good amount of funding, which may not be possible with the existing resources anymore. At this stage, the business owner needs to take a conscious call on whether to continue at the current scale and avoid external funding arrangements or to make a change in the funding policy to achieve the potential and scale up the business.

Therefore, at this juncture or crossroads, businesses often make a conscious call and decide to dilute their bootstrapping and allow venture capitalists or other investors to invest. The other name for phase 3 is the ‘Credit Stage.’

Advantages of Bootstrapping

- The owner of the business has full control over the business.

- The requirement of disclosure of all business details to the shareholders, investors, and debtors is not seen here. As a result of this, the maintenance of secrecy in the business prevails.

- The Entrepreneur solely makes all the business decisions without taking anybody’s approval. Or without getting influenced by the advice and guidance of others.

- All the budding entrepreneurs invest a lot of time and energy in finding prospective venture capitalists or prospective angel investors for raising funds. Thus Bootstrapping saves a lot of such time and energy.

- It allows the business owner to do enough experiments with the products to finally come up with the best suitable product. Thus there exists completely no pressure from the investor’s end.

- It makes interest rate payments almost nil, thus reducing the cost of debt.

- There are high chances of getting positive cash flow by following this method.

- Lack of funding at times leads to creative thinking.

- When the business reaches the third stage and expects to fund, it becomes very easy. Venture Capitalists give preference to Bootstrapped businesses.

Disadvantages of Bootstrapping

- All financial risk is borne by the business owner only. Dilution of risk amongst investors and debtors doesn’t takes place.

- In Bootstrapping, limited growth opportunities are seen because of limited resources available.

- At times the quality of products and services also gets hampered due to a lack of monetary, physical, and technological assistance.

- Family assets and personal assets are at high risk here.

- The Credibility of the business is very low in bootstrapping. A business with investors, shareholders, and the debtor is more credible than a business following bootstrapping.

- Bootstrapping is only suitable for small or medium-scale businesses. As the business expands, it becomes really difficult to rely only on personal finances.

- The business owner can face stress, depression, anxiety, or even a nervous breakdown in such a situation.

- An owner may not be an expert in all the fields of the business, and hiring that skill may be a costly affair for the business at such a low operating level. And thus, the business can not take advantage of the advice and suggestions of experts.

Conclusion

Most entrepreneurs and business owner adopts Bootstrapping method at the start-up and expansion stage of the business. Thus, according to experts, the financing of almost more than 80% of start-ups takes place on personal finance only. As a result of its several positive factors, despite limitations, it is still one of the best ways to finance a business at an early stage. So the business can contribute and work on the core idea and, in the process, develops the idea. And also get the hang of the other surrounding needs. So once the initial phase is over, the owner has a credible past and rich exposure to managing the business. All this bodes well for the next level of funding arrangement and both the parties – promoters as well as financiers.

Continue reading about various other sources of finance for startups.