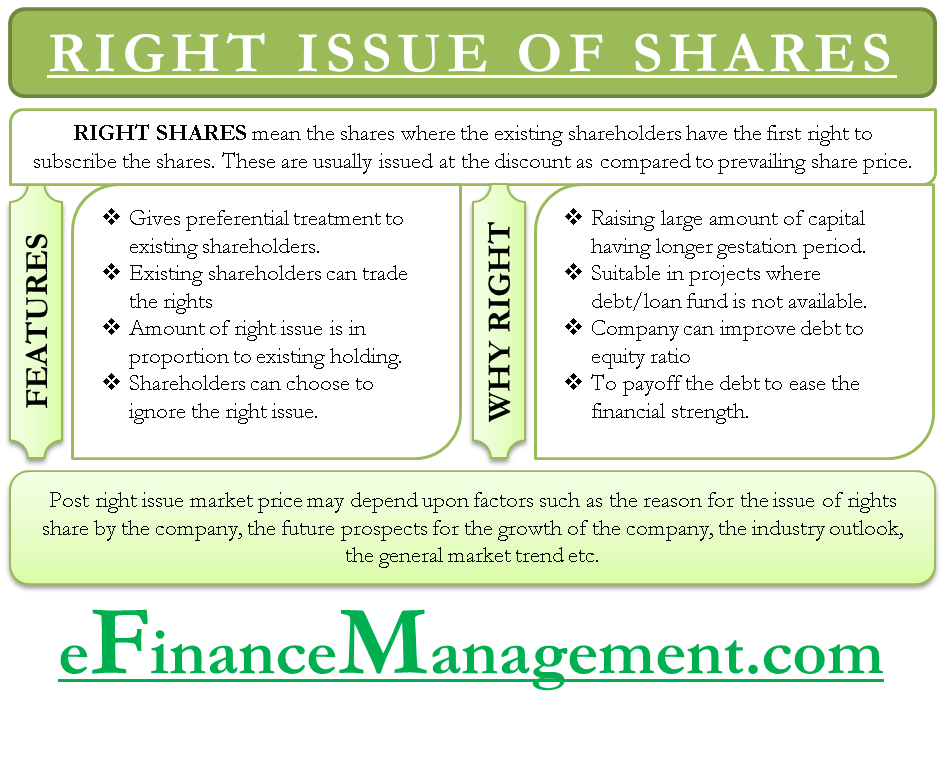

A rights issue is one of the ways by which a company can raise equity share capital among the various types of equity share capital sources available. These are slightly different from the standard-issue of shares. Right shares mean the shares where the existing shareholders have the first right to subscribe to the shares.

In layman’s terms, the rights issue gives a right to the existing shareholders to purchase additional new shares in the company. Rights shares are usually issued at a discount compared to the prevailing traded price in the market. The existing shareholders are allowed a prescribed time limit/date within which they need to exercise the right, or the right will thereafter be forgone.

Let us look at the features of the rights issue, reasons why rights shares are issued, accounting treatment of rights issue, and how market price reacts post rights issue. This will help us understand the concept better.

Features of Rights Issue of Shares

- The rights shares allow preferential treatment to existing shareholders, where existing shareholders have the right to purchase shares at a lower price on or before a specified date. The shares are issued at a discount as compensation for the stake dilution that will take place post issue of additional shares.

- The existing shareholders can trade the rights to other interested market participants until the date at which the new shares can be purchased. The rights are traded in a similar way as the normal equity shares.

- The amount of rights issue to the shareholders is usually at a proportion of existing holding.

- The existing shareholders can also choose to ignore the rights; however, one may not do so as existing shareholding will be diluted post issue of additional shares and will result in a loss (in valuation) for the existing shareholder.

Why Does a Company Issue Rights Shares?

- A company may look to raise a large amount of capital for expansion projects which may have a longer gestation period.

- A project where debt/loan funding may not be available/suitable or expensive usually makes the company raise capital via this route.

- Companies looking to improve the debt to equity ratio or looking to buy a new company may opt for funding via the rights issue route.

- Sometimes troubled companies may issue rights shares to pay off a debt to ease the financial strain.

Having looked at the features, let us look at an example of a rights issue.

Right Issue Example

Let us say an investor owns 1000 shares of ABC Ltd., and the shares are trading at a price of $10. ABC Ltd. announces a rights issue in the ratio of 2 for 5, i.e., each investor holding 5 shares will be eligible for 2 shares from the new issuance. The company announces a discounted price of, say, $6 per share. This means that for every 5 shares of the value of $10 held by an existing shareholder, ABC Ltd will offer 2 shares at a discounted price of $6.

Also Read: Equity Share and its Types

Portfolio Value before Rights Issue = 1000 shares X $ 10 = $ 10,000

No. of Right Shares to Be Received = (1000 X 2/5) = 400

Cost of Purchasing New Shares Using the Rights = 400 shares X $6 = $ 2,400

New quantity of shares = 1000 + 400 = 1400

New portfolio value = $ 10,000 + $2,400 = $12,400

Price per share post rights issue = $12,400 / 1400

= $8.86

The theoretical price per share post rights issue equals to $8.86 as against the initial price of $10. However, market reaction to the rights issue can be slightly different, depending on many other factors.

Let us look at the market price action by a company post rights issue.

Market Price Action Post Rights Issue

The price action post rights issue depends on various factors that include the reason for the issue of rights share by the company, the future prospects for the company’s growth, the industry outlook, the general market trend, etc., among many other things. It, therefore, does not mean that, as the rights issue is given a discount, it may always be beneficial to the existing shareholder.

Accounting Treatment for Rights Issue

The accounting treatment for rights issue is similar to the case when ordinary shares are issued at the premium since rights issue is usually above the face value but lower than the market price. Accounting entries shall be passed as follows.

Bank A/c

To Share Capital A/c

To Share Premium A/c

Conclusion

In summation, rights issues are a way by which companies can raise equity capital by giving the existing shareholders the privilege to buy a specified number of new securities at a specified price within a specified time frame. The rights issue is different from bonus shares. While both of them are issued to existing shareholders, bonus shares are for free, whereas rights shares are usually at a discount. Rights issue also differs from the initial public offer or follow-on public offer as rights are issued to existing shareholders at a discounted price compared to market value. In contrast, ordinary shares may be issued at face value or at a premium to the general public at large.

What to do when company wants to issue all the right shares to just one shareholder ( all other shareholders are agreeing to it). How to calculate the ideal ratio for the same? Is it lawfully allowed , if the company takes in written from remaining shareholders that they are relinquishing their right, so can company issue all its right shares to that one shareholder only?

In our opinion and to the best of our knowledge: In a right issue, one has to make the offer to all the shareholders and all the other can either deny or accept the offer. Thus, all the shares can be issued to one shareholder.

Pls enlighten if there is any restrictions regarding use of share application money pending allotment in case of rights issue. The same is found in case of preferential issue / IPO.