Advantages and Disadvantages of Zero Based Budgeting

Zero-based budgeting is a method of budgeting wherein no base is considered in the preparation of the budget. Having learned zero-based budgeting in the… Read Article

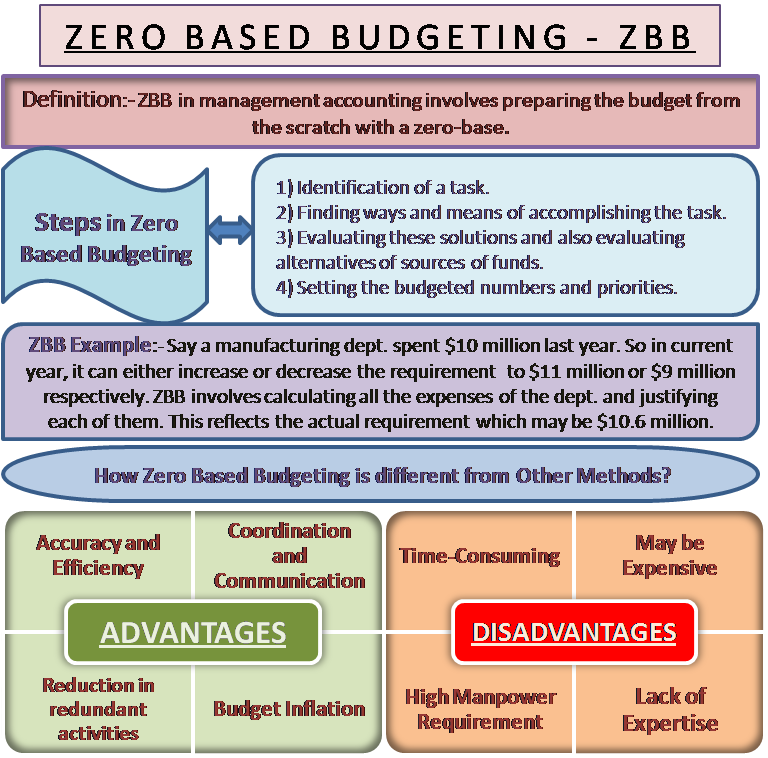

Zero-based budgeting in management accounting involves preparing the budget from scratch, that is, with a zero-base. It involves re-evaluating every line item of the cash flow statement and justifying all the expenditures a department will incur.

Thus, the definition goes as “a method of budgeting whereby all the expenses for the new period are calculated on the basis of actual expenses that are to be incurred and not on the differential basis which involves just changing the expenses incurred taking into account change in operational activity.” Under this method, every activity needs to be justified, explaining the revenue that every cost will generate for the company.

Contrary to traditional budgeting, in which past trends or past sales/expenditures are expected to continue, zero-based budgeting assumes that there are no balances to be carried forward or there are no expenses that are pre-committed. In the literal sense, it is a method for building the budget with zero prior bases. It emphasizes identifying a task and then funding these expenses irrespective of the current expenditure structure.

1) Identification of a task

2) Finding ways and means of accomplishing the task

3) Evaluating these solutions and also evaluating alternatives of sources of funds

4) Setting the budgeted numbers and priorities

To understand the Steps in Zero Based Budgeting, an example is given below to understand how it works.

Let us take an example of a manufacturing department of a company ABC that spent $ 10 million last year. The problem is to budget the expenditure for the current year. There are multiple ways of doing so:

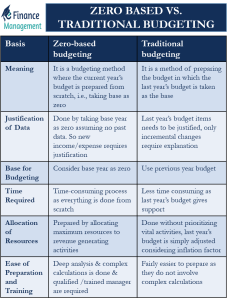

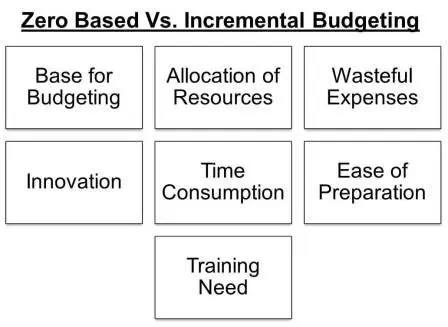

To have a clear understanding, it is necessary to understand the key differences between zero-based budgeting and other methods of budgeting.

Having understood the calculation, let us move to some of its advantages and disadvantages, as stated below:

The following are the Advantages of zero-based budgeting:

The following can be disadvantages of zero-based budgeting:

Conclusion: Zero-based budgeting aims at reflecting true expenses to be incurred by a department or a state (in the case of budget-making by the government). Although being time-consuming, this is a more appropriate way of budgeting. At the end of the day, it is a company’s call as to whether it wants to invest time and manpower in the budgeting exercise to provide more accurate numbers or go for an easier method of incremental budgeting.

Must read Budgeting for other types of budgeting