Parents usually take student loans to fund the higher studies of their kids. Generally, these loans come with easy repayment options. The financial institutions usually allow the borrower to start paying the loan a couple of years after finishing the degree. This grace period is usually given to the students to ensure that they complete the course and get into a job and, therefore, are able to pay easily. The interest rates and other conditions on a student loan differ depending on the type of loan and the agency from which the loan is availed. Let’s understand the different kinds of student loans in detail.

Different Types of Student Loans

Broadly there are two different types of student loans on the basis of the agency from which the loan is taken – Federal Loans and Private Loans. Under a Federal loan, it is the government that extends the loan to the student, while the private banks or Credit Unions give private loans.

Federal Loans

There are several types of federal loans.

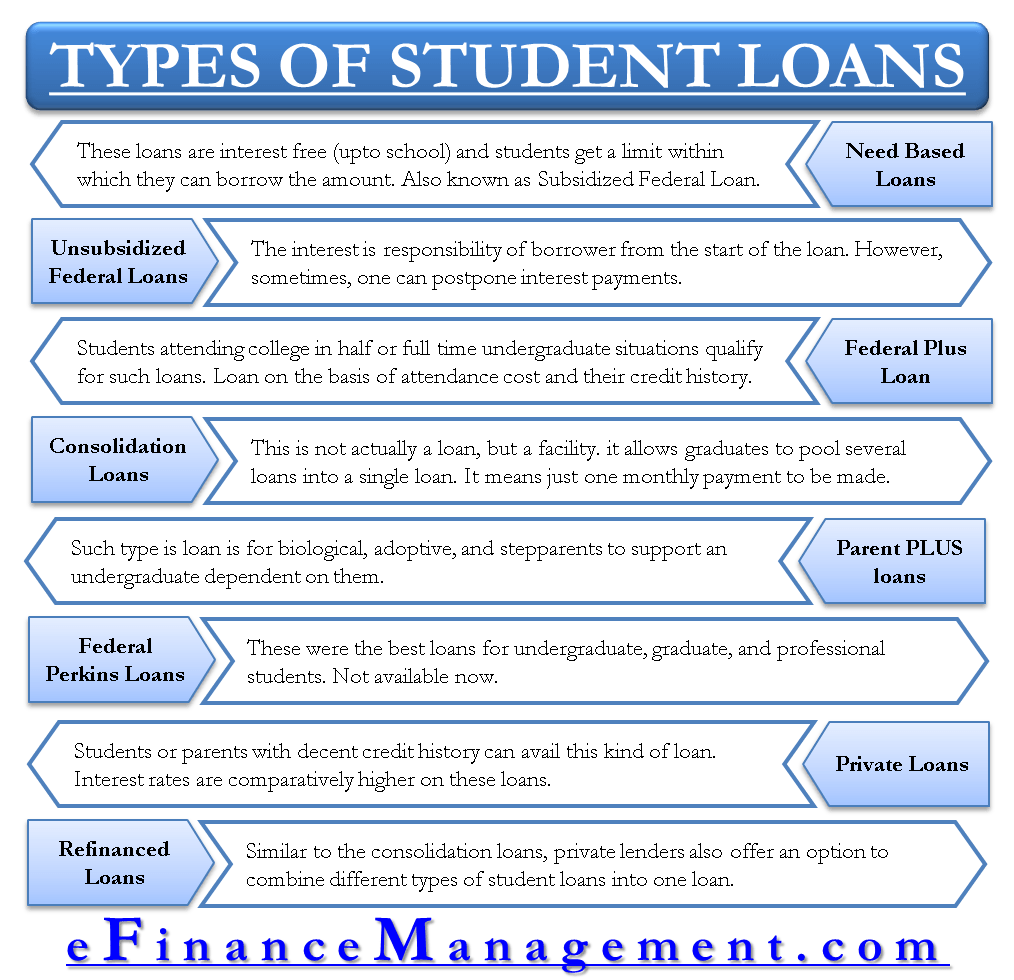

Need-Based Loans or Subsidized Federal Loans

Students who cannot afford higher studies but have shown promise in academics are eligible for need-based loans. These loans are interest-free (while students are in school), and students get a limit within which they can borrow the amount. This limit may increase each year, meaning a student would be able to withdraw more money every year of their college than the previous one.

Also known as Subsidized Federal Loans, these are the most generous type of loans for a student to complete their higher education as they carry a low interest and are long-term.

Unsubsidized Federal Loans

It is a long-term loan but is not on the basis of need. Under this, the interest is the responsibility of the borrower from the start of the loan. However, in some cases, one can postpone interest payments.

Unsubsidized federal loans also carry a low interest and are best for a student who doesn’t qualify for other financial aid. Moreover, these loans are also helpful for those who need more funds to cover their financial expense.

Read Subsidized vs. Unsubsidized Loan for more details.

Federal Plus Loans

Students attending the college in half or full-time undergraduate situations qualify for such loans. Parents get loans for the education of the student on the basis of attendance cost and their credit history. Just like the need-based loans, the Federal plus loans also carry low interest, and repayment is scheduled within 60 to 90 days after the full loan disbursement or after the completion of the course. Such a loan comes in handy in bearing other college expenses after using other financial aids.

Direct Consolidation Loans

This is not actually a loan but a facility. As the name suggests, it allows graduates to pool several loans into a single loan. It means the borrower has to make just one monthly payment. Moreover, it can help lower the monthly liability by extending the loan to more years.

Parent PLUS loans

Parent plus loan is a type of loan for biological, adoptive, and stepparents to support an undergraduate dependent on them. It is different from other loans in a way that the government expects parents to make the payment until the child is in school. However, one may request a deferment while applying for the loan.

Federal Perkins Loans

Federal Perkins Loans are not available anymore. These were the best loans for undergraduate, graduate, and professional students. They were given on the basis of extreme financial need, and the interest rate was also very low.

Other Types of Student Loans

Private Loans

Students or parents with decent credit history can avail this kind of loan. The credit unions or the financial institutions that give such loans are authorized but not banked by the government. In case the student does not have a credit history, the guardian can apply for the loan, and the student has to be a co-signer.

Interest rates are comparatively higher on these loans. Therefore, such a loan is suitable for those who are confident of repaying even with a high-interest rate. However, there are some private institutions that offer lower interest loans for certain colleges.

One should opt for student loans from private institutions only when they do not get one from any Federal bank. Make sure that you understand all terms before availing of a loan from a private organization.

Refinanced Loans

Like consolidation loans, private lenders also offer an option to combine different types of student loans – Federal and private loans – into one loan. Such an option may not be a very good idea as it does not result in a saving. Such a type of consolidation would expand the repayment term and can increase the cost.

One advantage of refinancing is the lower interest rate that would convert into savings. But, a borrower will need a robust credit score and steady income to qualify for a lower interest rate. You would see many private lenders talk about the saving of an average customer through refinancing the loan.

Applying for a Student Loan

The process is simple, and institutions ask for online applications. A few simple steps that a student needs to follow are:

- Open the website of the lender from who you want to avail of the loan.

- Before applying for a loan, you should always check the interest rates, repayment time, duration, and flexibility provided by the banks.

- Banks also ask the students or the applicants to select the type of loan they would want to apply for.

- An important tip is to add a co-signer, as this increases the chances of getting a loan.

- Once you send the application, the lender will follow due diligence and go through the details. If everything is in-line with the requirements, the lender approves the loan application. If not, then the lender would give you the reason.

- Once you get approval for your loan, you need to sign and submit the financial aid award letter.

Though federal loans are usually the best, private loan companies have been enjoying success lately as they are able to customize a loan. If you are looking for a student loan, you must evaluate all the options you have. Also, you must understand every key detail, like interest rate, payment terms, penalty, and more.

RELATED POSTS

- Subsidized vs Unsubsidized Loan: Meaning, Differences and Similarities

- Federal Perkins Loan – Meaning, Eligibility, and Benefits

- Sources of Loan

- Types of Personal Loans – These Are The Options You Have

- Unsecured Personal Loans – Meaning, Benefits, Criteria, and Application

- Signature Loan – Meaning, Features, How it Works, and Use