Personal Loans are meant to cover emergency financial requirements, if any. Undoubtedly, these are some of the simplest ways of getting funds through a legit source. Banks can lend money and decide on the amount depending on various parameters that are in place. Personal loans might seem a fairly simple process for a person with financial knowledge. However, most still struggle to understand the financial jargons and requirements that come with it. Moreover, many are ignorant of the types of personal loans available. So, in this article, we will be discussing different types of personal loans available to a borrower.

Types of Personal Loans

There are different types of personal loans with their pros and cons. A borrower can decide the type of loan they want depending on their need. Let’s understand different types of personal loans and their pros and cons.

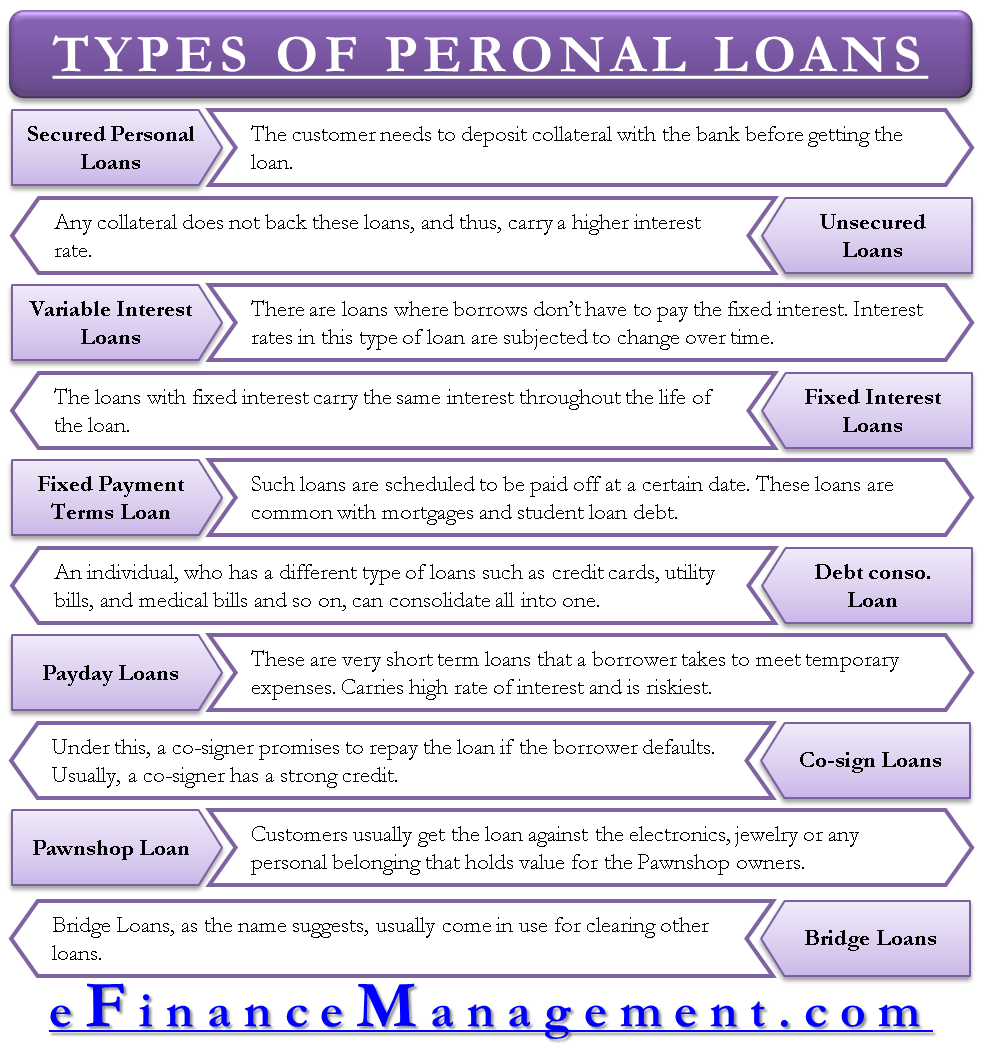

Secured Personal Loans

As the name suggests, a secured Personal Loan is a loan where the customer needs to deposit collateral with the bank before getting the loan. Such types of loans are undertaken when the banks do not want to take the risk of users defaulting on the payments. A user can keep anything such as savings, bonds, cars, and more as collateral with the bank to get the loan. Banks will sell the asset to realize the loan amount if the user defaults.

Unsecured Loans

An unsecured personal loan is a loan where the collateral does not back these loans and thus, carries a higher interest rate. A high rate of interest acts as compensation for the bank taking a higher risk by not asking for any collateral. This means that banks do not have any safety net to fall back on if the user defaults.

On the customer front, credit scores play an important role in deciding the type of loan you are eligible for. If a user has a good credit score, they are more likely to get an unsecured loan. For those unaware, credit score means how promptly you have made the payments on the credits taken previously, including payments for credit cards, pay later apps, etc.

Variable Interest Loans

There are loans where borrowers don’t have to pay the fixed interest. Interest rates in this type of loan are subjected to change over time. As the interest rate keeps fluctuating, it might sound like a good idea to take the benefit of low-interest rates. However, on the flip side, you might end up paying a high-interest rate as the metric shoots up. If the credit score of a user is not up to the mark, they might not be able to borrow a large sum of money using the variable interest rate.

Fixed Interest Loans

Unlike the loans with variable interest, the loans with fixed interest carry the same interest throughout the life of the loan.

Fixed Payment Terms Loan

Such loans are scheduled to be paid off at a certain date. These loans are common with mortgages and student loan debt.

Debt-consolidation Loan

Customers can avail of this loan if they need to pay any other debt. It is never a good idea to get into one debt to clear another debt. However, the exact way in which this type of loan works is different. An individual, who has different types of loans, such as credit cards, utility bills, medical bills, and so on, can consolidate them all into one. After that, a borrower can use the debt consolidation loan to pay off all such loans.

The idea is that instead of serving different loans, a borrower needs to focus on paying just one loan. Although some debt consolidation companies are legitimate, customers need to be extra careful while availing such loans. Before selecting the company, you would need to take advice from a financial expert on the legitimacy of the company offering the loan.

Payday Loans

One of the quickest ways of getting a loan is by applying to payday loan providers. However, customers should know that payday loans are also one of the riskiest loans you can avail of. These are very short-term loans that a borrower takes to meet temporary expenses. Therefore, they carry a very high-interest rate.

There are endless stories of how borrowers end up in a debt trap after availing of payday loans. People should only consider availing such loans if they have no other option left and require the money urgently.

Co-sign Loans

Such type of loan is for borrowers with little or no credit history. Under this, a co-signer promises to repay the loan if the borrower defaults. Usually, a co-signer with strong credit enhances borrowers’ chance of getting a loan at a lower rate and with favorable terms.

Pawnshop Loan

Just like payday loans, these loans come with very high risks and are for the short term. Customers usually get the loan against the electronics, jewelry, or any personal belonging that holds value for the Pawnshop owners. The interest rates are very high.

Bridge Loans

These are also short-term loans offered to customers. The maximum tenure of such loans is a year, but sometimes it can be beyond that. As the name suggests, Bridge Loans usually come in use for clearing other loans. The interest rate is high on these types of loans.

Top-up Loans

These loans are similar to bridge loans. Such loans are for the borrowers who already have a personal loan but need more funds. These loans carry a relatively lower interest rate than personal loans and may also offer tax benefits. However, these loans are given to the borrowers with a good repayment record on the personal loan.

Signature Loans

In a signature loan, if a customer agrees to offer a signature as an assurance of paying the loan back, the lender agrees to offer them the loan. In this type of loan, the borrowers’ signature acts as collateral. Such loans are fit for those with good credit ratings.

Personal Line of Credit

A personal line of credit is not exactly a loan; rather a revolving credit, or we can say a credit card. Under this, the borrower doesn’t get a lump sum but rather gets access to a credit line. From this credit line, a borrower can borrow as per their need. Moreover, the borrower pays interest on what they borrow. Such types of loans are best for paying ongoing expenses or emergencies.

Which Loan to Choose?

Before going for any loan, a borrower should thoroughly evaluate all types of personal loans. A borrower must evaluate each option on the basis of interest rates, processing fees, monthly payments, and more.