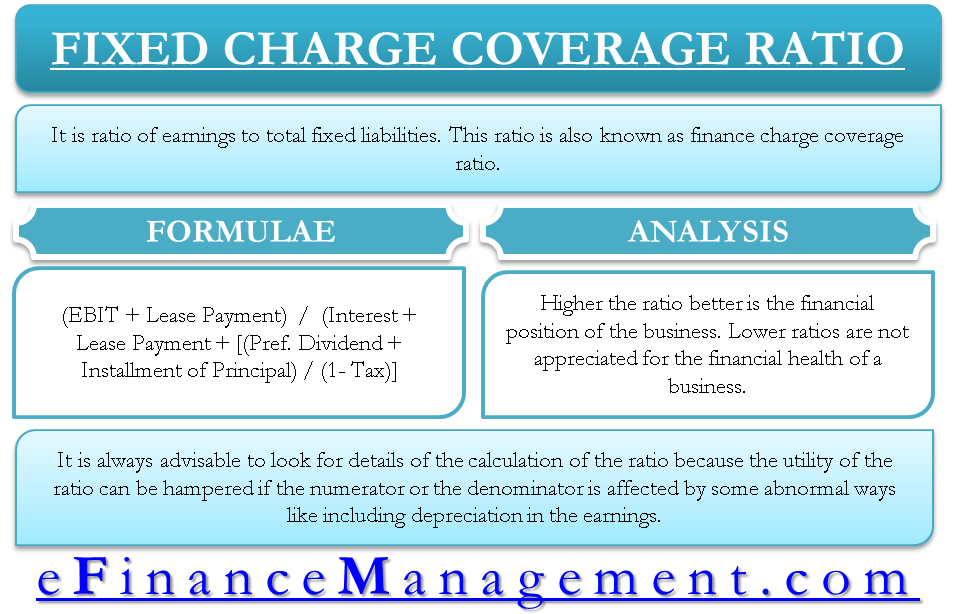

The fixed charge coverage ratio is the most meaningful ratio out of all the coverage ratios from a general point of view. It is a ratio of earnings to total fixed liabilities. Since it covers all the fixed liabilities, its coverage is broader than other ratios such as debt service coverage ratio, dividend ratio, interest service ratio, etc.

As suggested by its name, the fixed-charge coverage ratio is a ratio in relation to the fixed charges. In this reference, the other name for fixed charges is finance charges. Therefore the ratio is term as the finance charge coverage ratio, apart from the total fixed charge coverage ratio. Fixed charges are those charges in any business which occur irrespective of the revenues and other things. They are fixed by their nature and do not change with a marginal increase in the business’s activity. Here, the fixed charges mean the interest charge, lease payments, preference dividend, installments of a loan, etc.

We can easily understand with the example that with the increase in revenues of the business, the interest charges on loans (say) do not change.

How to calculate Fixed Charge Coverage Ratio (FCCR)?

The calculation of the total fixed charge coverage ratio requires many figures from the profit and loss statement. The items to ascertain from the P/L statement are EBIT, lease payments (if any), interest, preference dividend payments, installments of principal, and tax rate. The formulae for the total fixed charge coverage ratio are as follows:

PAT is generally available readily on the face of the Profit and loss account. It is the balance of the profit and loss account that transfers to the reserve and surplus fund of the business. Sometimes, in the absence of the profit and loss statement, we can also find it on the balance sheet by subtracting the current year’s P/L account from the previous year’s balance. And these balances are readily available under the head of reserve & surplus.

Lease Payments

Lease payments are the total amount of lease rentals paid or payable in the current financial year under concern.

Interest

It is also the amount of interest on loans paid or payable in the financial year under concern.

Preference Dividend

It is the total amount of dividend for which the distribution has already taken place to the preference shareholders in the concerned year.

Installment of Principal

The total amount of the loan is distributed over the loan term to be paid by the business. The part accrued or paid in the current year is considered an installment of principal.

Tax Rate

It is the rate of tax relevant to the business. The rate varies with the countries in which the operations are based. The government of the respective country monitors the rates.

Why do we divide the Installment and Preference Dividend by (1-Tax Rate)?

We divide the installment and preference dividend by (1- Tax Rate) because both are not tax-deductible expenses of a business. A business cannot claim dividends and installments as an expense against the company’s profits. And the payment is out of the net earnings of the company. Here in our formulae, we have taken EBIT as our earnings. Therefore, to compare the denominator and the numerator, it requires all fixed charges to be a before-tax item.

Interpretation of Total Fixed Charge Coverage Ratio

The interpretation of the ratio is very simple. The higher the ratio better is the financial position of the business. Lower ratios do not get an appreciation for the financial health of a business. It is because the lower ratio suggests the incapability of the business to sustain against the fixed charges. In simple words, the company or the firm is not earning enough to pay the liabilities, thereby creating bankruptcy risk.

As far as there is a consideration of a benchmark, the first danger line is a ratio of 1. If a company has a ratio of less than 1, it means that the company cannot serve its debts or fixed charges and is most likely to fail. Usually, the utilization of this ratio takes place when a bank or financial institution or rating agencies that rate the companies for different purposes such as bond rating, general rating, etc., have to sanction a limit for a loan or working capital.

It is always advisable to look for details of the ratio calculation because the utility of the ratio might hamper if some abnormal ways, like including depreciation in the earnings, affect the numerator or the denominator. Depreciation can affect the utility because, ultimately, the payment of fixed charges is from the cash available and not from the profits, which may contain non-cash items like depreciation.

Sanjay Borad, Founder of eFinanceManagement, is a Management Consultant with 7 years of MNC experience and 11 years in Consultancy. He caters to clients with turnovers from 200 Million to 12,000 Million, including listed entities, and has vast industry experience in over 20 sectors. Additionally, he serves as a visiting faculty for Finance and Costing in MBA Colleges and CA, CMA Coaching Classes.