What are Convertible Bonds?

A convertible bond is a type of debt instrument that comes with the option of getting converted into equity shares. It can be converted into the shares of the issuing company at a later date and at a pre-determined conversion price. It can also be classified as a derivative instrument because it derives its value from both the prevailing interest rates and the stock price of the company.

Convertible bonds are usually issued by companies with a lower credit rating. Because of the lower rating, they would need to pay a high coupon rate and a high yield to attract investors to their bonds. So instead of issuing plain bonds, they issue convertible bonds. Convertible bonds have a lower yield than plain bonds but provide additional upside to the investors through conversion to equity. If the investors are not able to convert their bonds, they will, anyways, be entitled to the regular coupon payments, albeit at a rate lower than the market. It is a win-win for both the issuer and the investor. Convertible bonds are also termed as just ‘convertibles’ or ‘converts.’

Characteristics of Convertible Bonds

The following are the features of a convertible bond:

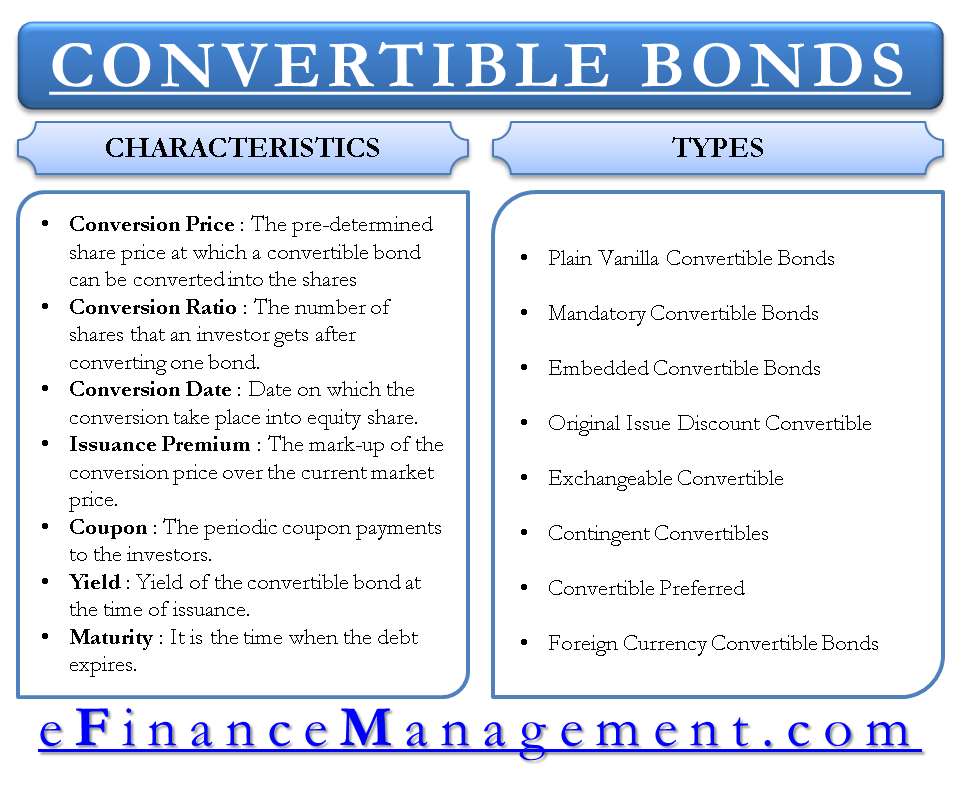

Conversion Option

The most distinctive feature of a convertible bond is its conversion option. This means that the bondholder has the right, but not the obligation, to convert the bond into a certain number of shares of the issuer’s common stock.

Conversion Price

The pre-determined share price at which a convertible bond can be converted into the company’s shares. The conversion price is usually at a high premium to the prevailing market price when the bonds are issued.

Also Read: Convertible Debentures

Conversion Ratio

The number of shares that an investor gets after converting one bond. A conversion ratio of 100:1 will mean that the investor will get 100 shares for each convertible bond that he holds.

Conversion Date

Convertibles can be designed to have certain periodic conversion dates or windows in which these can be converted into the shares of the issuing company.

Issuance Premium

The markup of the conversion price over the current market price at the time of issuing the convertible bonds. This is usually high to push the dilutive effects of the bonds in the future.

Coupon

The periodic coupon payments to the investors. The coupon rate is fixed at the time of issuance.

An Option like Characteristics

Convertibles can also be designed to have option-like features. The issuing company can have a right to call the bonds before the conversion date or maturity. Similarly, the investor can have a put option where he can redeem the bond and get full principal before maturity if the stock price goes below the conversion price.

Also Read: Difference Between Warrants and Convertibles

Types of Convertible Bonds

Convertible bonds can be classified based on the variation in their underlying characteristics.

Plain Vanilla Convertible

It is the simplest form of the convertible, which has a fixed conversion price and maturity. If the stock price reaches the conversion price before maturity, the investor can convert the bond to stocks. But the investor will have to forego any accrued interest between the last and the next coupon payment if he converts between two consecutive coupon dates. The investor can choose to convert or not to convert based on the stock price.

Mandatory Convertible

It has to be converted irrespective of at what price the share is currently trading.

Embedded Option Convertible

As explained in the characteristics of convertible bonds, these can be issued with a call option to the debt issuer or a put option to the bond investor.

Original Issue Discount Convertible

These are issued at zero coupons and a heavy discount on the bond’s par value. Naturally, they have a high yield and are issued by companies that are facing or expected to face a cash crunch.

Exchangeable Convertible

The bond can be converted into the shares of a different company or a different instrument altogether.

Contingent Convertible

The conversion is contingent upon the stock price reaching a certain markup over the conversion price and remaining there for a certain period of time.

Convertible Preferred

The originally issued instrument is a preference share instead of a bond. The features are similar to a convertible bond. The yield is higher than a convertible bond.

Foreign Currency Convertible Bond (FCCB)

If a company wants to raise money from a foreign country, it will issue FCCBs. FCCBs are denoted by a currency that is different from the currency in which the issuer does its business. These are prevalent amongst companies from developing nations like India, where they issue USD, GBP, and EUR-denominated FCCBs.

Advantages & Disadvantages of Convertible Bonds

Convertible bonds also pay the bondholders or investors regular interest as per the terms of the issue, like any other bond, non-convertible bond. However, with the addition of the convertible option, the bond becomes quite attractive. These bonds do have their pros and cons.

Advantages to Issuer

- It becomes easier to market the securities and arrange the funds for the organization.

- Due to the attraction of the conversion option, the issuer may be able to sell the bonds at cheaper interest rates than it would have to pay otherwise.

- This cheaper interest rate benefit is applicable through the tenure of the bond.

- This entails lower interest outgo in the initial setup period and helps the company to avoid cash flow stress and default risk.

- Moreover, a portion of the original bond price will become non-interest paying after conversion. So interest liability even in the later year stands reduced.

- The company’s debt eligibility and debt-raising capacity further increase once the conversion takes place.

Disadvantages to Issuer

The biggest issue with the issuer is that the company has to offer equity shares to these bondholders after some time at a price decided now. This price may not consider the actual business potential or growth of the business. Thus, it has to offer or shelve out the stake at a lower price.

Advantages to Bondholder

- Good opportunity to make an entry into a good company, where direct entry may be costlier.

- Continue to get interest till conversion, so money is earning a return always.

- Stock rights at a later time at cheaper rates. By the time of conversion, the company’s business establishes, and the stock price starts commanding a premium.

- Thus, dual advantage, fixed interest earnings, and participation in stock appreciation and dividend.

Disadvantages to Bondholder

- All this is good till there is no downward turn in the potential and prospects of the company. If the business growth is not on the expected lines, the share conversion may take place at a higher price.

- The company may not perform well, and it may run the risk of interest and principal payment default.

In all such situations, if the conversion right remains optional, at the will of the bondholder, then most of the risk with regard to a conversion price of a stock and future potential thereof can be well taken care of.

Refer to Bonds and their Types To know about various other types of bonds.

Really informative posts and ideas