A Leased Asset is an asset leased by the owner to another party in return for money or any other favor. While leasing an asset, the owner enters into a contract allowing the other party the temporary use of an asset.

Capital Lease and Operating Lease

In terms of accounting, one can lease an asset in two ways – Capital Lease and Operating Lease. The difference between the two is on the basis of whether or not the risk and reward with the asset are transferred to the lessor or not.

If the lessor gets the risks and rewards, it is a Capital lease or Financing lease under IFRS Standards. A lease qualifies as a capital lease if it meets any of the following conditions:

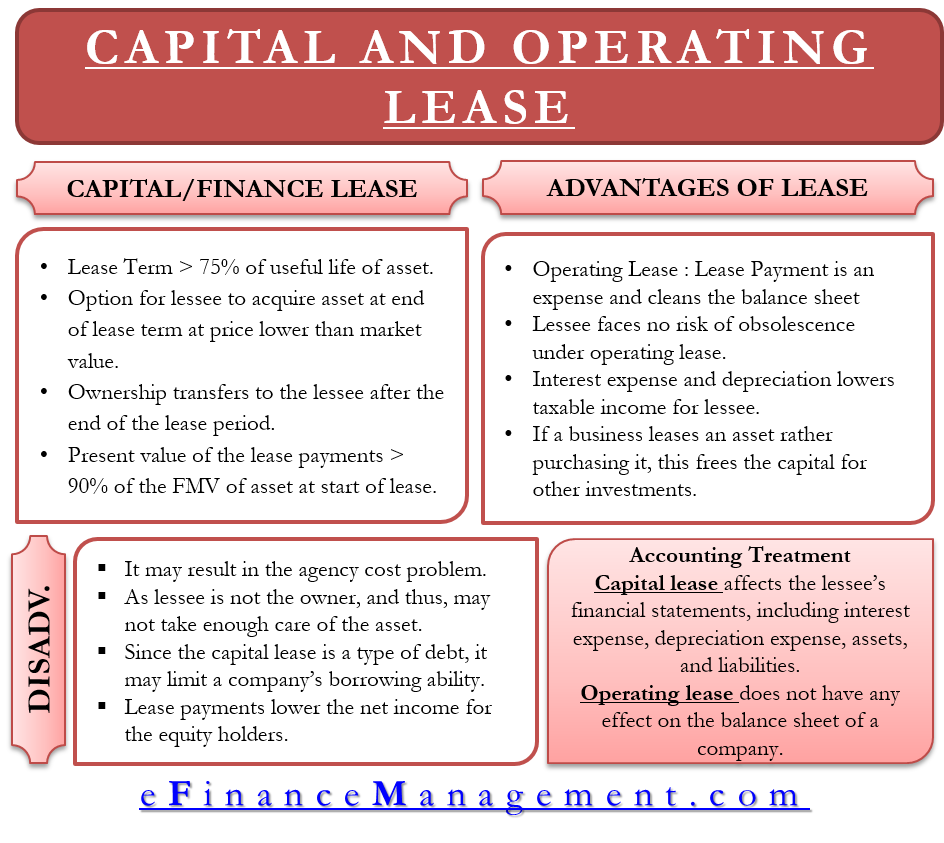

- The lease term must be greater than 75% of the asset’s useful life.

- There is an option for a lessee to acquire the asset at the end of the lease term at a price lower than the market value.

- Ownership transfers to the lessee after the end of the lease period.

- The present value of the lease payments is greater than 90% of the fair market value of the asset at the start of the lease.

All other types of lease come under operating lease and are the same as a rent contract between a landlord and renter.

Accounting Treatment Of Leased Asset

Capital Lease

In a finance lease, the lessee effectively assumes the risks and rewards of ownership, and the lease term is typically longer. Here’s the accounting treatment:

- Lessee: The lessee records the leased asset as an asset and a corresponding liability on their balance sheet. The liability represents the present value of lease payments. The asset is depreciated over its useful life, and the interest expense is recognized on the liability. Lease payments are allocated between reducing the liability and interest expense.

- Lessor: The lessor derecognizes the leased asset from their balance sheet and records the lease receivable. They also recognize interest income over the lease term based on the implicit interest rate in the lease and allocate the lease payments between reducing the receivable and interest income.

Operating Lease

An operating lease does not affect the balance sheet of a company. In an operating lease, the lessee (the company leasing the asset) does not assume the risks and rewards of ownership, and the lease term is usually shorter. Here’s the accounting treatment:

- Lessee: The lessee records lease payments as operating expenses on their income statement over the lease term. No asset or liability is recorded on the balance sheet.

- Lessor: The lessor continues to recognize the leased asset on their balance sheet and records lease payments as rental income over the lease term.

Read a detailed article on the Accounting of Capital And Operating Leases by Lessor and Lessee.

Advantages

- In the case of an operating lease, the company creates an expense and not a liability. This helps it to keep its balance sheet clean. That is why an operating lease is “off-balance sheet financing.”

- Lessee faces no risk of obsolescence under an operating lease as there is no transfer of ownership.

- Interest expense and depreciation lower taxable income for the lessee.

- Since cash outflow or lease payments are spread over several years, this lowers the burden of making one-time significant cash payments.

- If a business leases an asset instead purchasing it, this frees the capital for other investments.

- Lease expenses remain constant over the lease tenure or grow in line with inflation. This helps a business to accurately plan cash outflows.

- Leasing is a good option for startups as it means lower capital requirements.

Disadvantages

- A big disadvantage of leasing is that it may result in agency cost problems. Since the lessor transfers all rights to a lessee for a specific time, the lessee is free to use the asset the way they like, and this results in a moral hazard issue. As lessee is not the owner and thus, may not take enough care of the asset. This separation between the ownership and the control of the asset is known as the agency cost of leasing.

- Since the capital lease is a type of debt, it may limit a company’s borrowing ability.

- Lease payments lower the net income of the equity holders.

We own a piece of waterfront property on which an investor wants to build a pier. I do not want to sell the property at this time. I am considering leasing for a 5 or 10 year period. I know nothing about leasing.