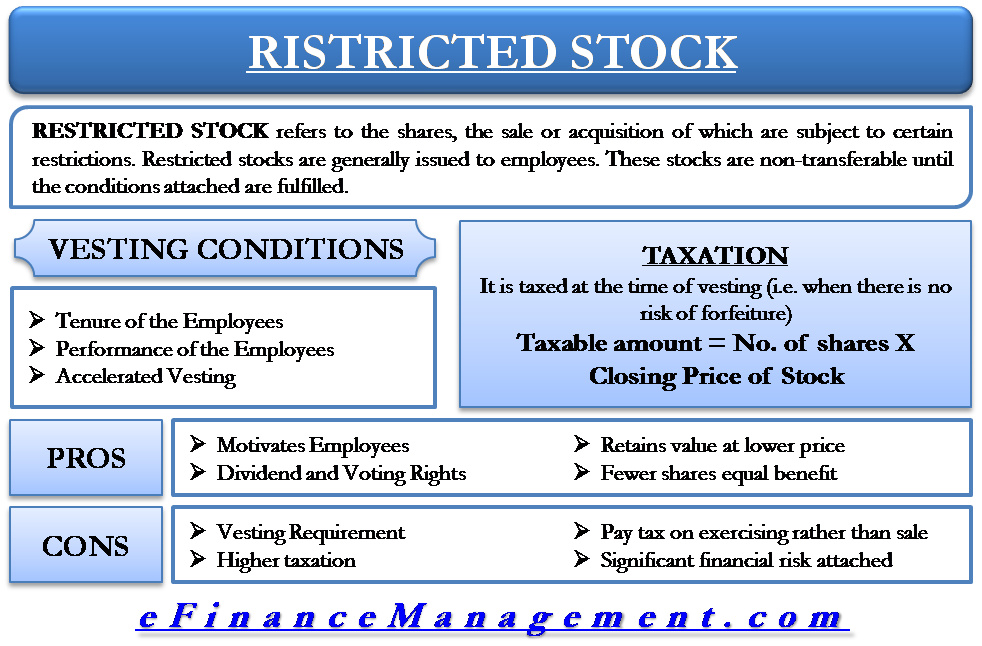

Restricted stock refers to the shares, the sale or acquisition of which are subject to certain restrictions. The shareholder of restricted shares has to meet these restrictions before they have the right to sell or transfer these stocks.

Employers use restricted stocks in employee compensation schemes (share-based compensation). The shares issued to the employees are non-transferable until the employee fulfills certain conditions. Some of the restrictions may include working for a certain period of time, or to fulfill pre-agreed individual performance goals, or achieving the specified corporate goal.

When the employee fulfills the conditions, the issuing company transfers the stocks to the grantee (employee). The issuing company will forfeit the shares in case the employee fails to fulfill the conditions.

Structure and Purpose

Company issue the restricted stocks to an employee on the issue date, similar to equity shares, preference shares, and other stock option plans. Though restricted stocks do not have any special features, the employee cannot take possession of these stocks until they complete the vesting schedule. A vesting schedule can be a program or task given to the employee by an employer. Restricted stock is classified as a “full-value grant,” whereby the shares carry the full value of the stock at the time of its issue.

These stocks resemble the traditional non-qualified plans; there is a substantial risk of forfeiting shares to the employees. Non-fulfillment of the requirements of the vesting schedule amounts to a forfeiture of stock.

Vesting Schedule

Employers issue restricted stock to employees to motivate them to accomplish corporate goals. There are generally three types of vesting conditions:

Tenure of the Employee

Various restricted stock plans require the employee to remain in the service for a certain time period of time, normally three to five years.

Performance of the Employee

The restricted stocks become transferrable when an employee accomplishes certain company goals like developing a new product or reaching a certain level of production.

Accelerated Vesting

A company might choose to shorten a vesting period to allow employees to gain access to their shares or stock options more quickly. This is known as accelerated vesting.

Companies use accelerated vesting where the company becomes insolvent or bankrupt (and to safeguard the employee so that he received at least something before the stock turns worthless) or in case of death of the employee or his disability.

Taxation of Restricted Stock

Restricted stocks do not create any taxable income at the time of issue. They are fully taxable when they become vested, i.e., when the risk of forfeiture is removed, and the employee receives the receipt of the shares or becomes the owner of shares. In simple words, when the time frame of the schedule gets over.

The taxable amount is equal to the number of shares that become vested on the date of vesting, multiplied by the closing price of the stock. The amount is taxable to the employee as compensation at the ordinary rate, regardless of the employee’s decision to retain or sell the shares.

Section 83(b) Election

Employees receiving the restricted stock have to make a very important choice once they enter these plans. They can pay the tax at the time when the stock is granted to them, or they can pay at the time of vesting. Section 83 (b) of IRC (Internal Revenue Code) permits this choice to employees. They can pay tax before vesting so that the burden of tax liability on the day of vesting can be minimized. But this strategy will work or not will depend on the performance of the stock as this is related to the price of the share on closing day.

Restricted Stock Advantages

Motivate the Employees

Companies would issue restricted stocks on the condition that an employee has to achieve certain performance targets and provide certain services before actually receiving shares and having the right to acquire them. It motivates the employees as it is the reward against the performance.

It is also beneficial for the company as the reward will be paid only after achieving the performance level.

Dividend and Voting Rights

The restricted stocks can carry the dividend and the voting right if the issuing company chooses. After the vesting period, the stock becomes the common stock.

An Advantage Over Stock Options

Restricted stocks require fewer shares to offer an equal level of benefit in comparison to what is needed for stock options. Because restricted stocks retain some value even if the share price declines.

Restricted Stock Disadvantages

Vesting Requirement

Let’s assume an employee is purchasing a stock at the market price. He does not get the actual possession of the stock. Buying such stocks may not seem very attractive to an employee. The situation of restricted stock is similar to this situation.

Higher Taxation

There is no capital gain treatment available for exercise. The entire amount of the vested stock becomes the ordinary income in the year of vesting. The capital gain treatment means paying tax only for any appreciation between the price at vesting and the sale of stock.

Timing of Taxes

The employee has to pay tax at the time of exercise regardless of when he sells the shares. Restricted stock usually becomes taxable upon the completion of the vesting schedule. The entire amount of vested stock becomes ordinary income for that year.

Significant Financial Risk

In comparison to other plans, restricted stocks have more complications. They involve financial risk for the employees when he makes a choice in Section 83 (b). After selection, if the price of stock declines or the employee leaves the company, he would end up paying unnecessary tax.