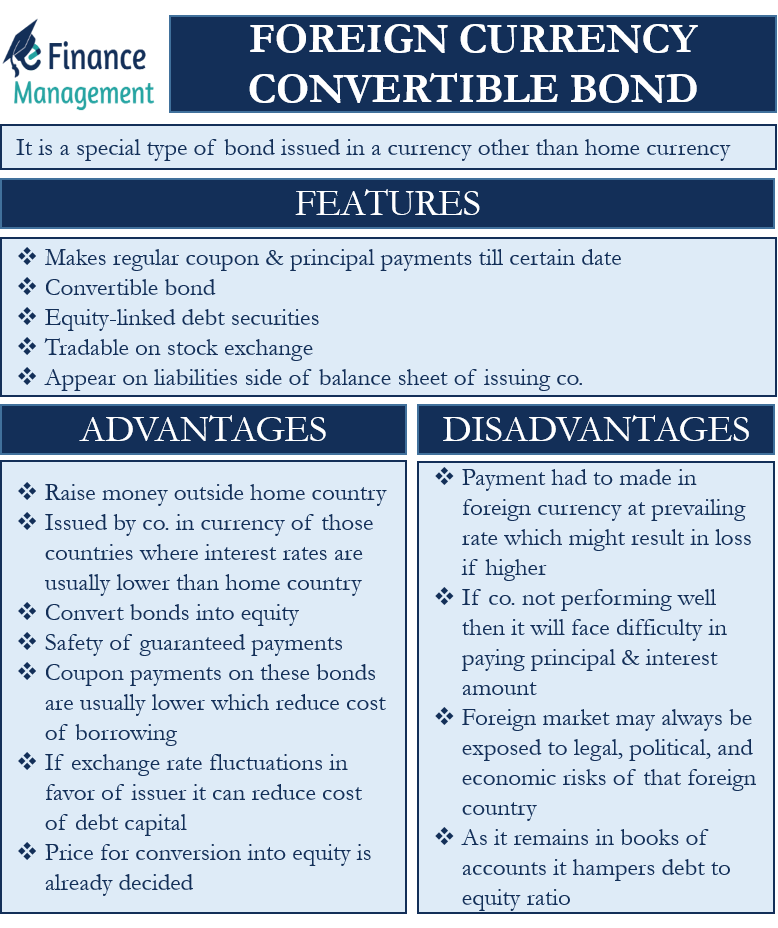

A foreign currency convertible bond is a special type of bond issued in a currency other than the home currency. In other words, companies issue convertible foreign currency bonds to raise money in foreign currency.

In today’s globalization scenario, FCCBs hold high significance, especially for multi-national companies that are constantly dealing with different world currencies. Let us look at some peculiar features of FCCBs that make them a luring investment option for investors.

Features of FCCBs

- Like any other type of bond, an FCCB makes regular coupon and principal payments till a certain date, after which it can be converted into equity.

- FCCBs retain all the convertible bond features and hence remain attractive to both issuers and investors.

- Another attractive feature of FCCBs is that these are equity-linked debt securities that give the holder the right to convert the bond into equity or a depository receipt (DR) after a certain period of time.

- FCCBs are tradable on the stock exchange.

- Like any other debt-raising instrument, FCCBs appear on the liabilities side of the balance sheet of the company issuing them.

Let us look at the merits and demerits of FCCB to understand this investment option in detail.

Advantages of FCCB

- FCCBs issuance allows companies to raise money outside the home country, thereby enabling tapping new markets for investment options.

- FCCBs are generally issued by companies in the currency of those countries where interest rates are usually lower than the home country, or the foreign country’s economy is more stable than the home country’s economy.

- FCCB holders may choose to convert the bonds into equity to benefit from the equity price appreciation that may have taken place.

- FCCB holders enjoy the safety of guaranteed payments on the bond and may opt to continue with the bond if equity or depository receipt if conversion isn’t more beneficial.

- Since these bonds come with an advantage to the bondholder, the coupon payments on these bonds are usually lower than a straight coupon-bearing plain vanilla bond. This helps the issuer to reduce the cost of borrowing.

- Exchange rate fluctuations in favor of the issuer can further reduce the cost of debt capital.

- The conversion of FCCBs into equity usually happens at a price already decided at the time of issuance. It is generally at a premium, so the company’s dilution is lower.

Disadvantages of FCCB

- Companies that borrow funds via FCCB in foreign currency shall have to make the repayment in foreign currency on the bond’s maturity. If it has moved considerably as compared to the rate prevailing on the day of the borrowing, the exchange rate prevailing on the day of the borrowing may result in losses for the company. The exchange rate in a volatile scenario may cause cash outflows on repayment to be much higher than the saving in the interest rate. Thus, a cost-saving motive may be totally taken off if the home currency depreciates beyond the interest rate saving.

- Suppose the stock prices do not appreciate and instead depreciate. In that case, the bondholders might refrain from converting bonds to equity, and the money might have to be repaid by the issuer on bond maturity. Hence, if the company is going through a bad phase, the stocks may not do well and, therefore, may not be converted to equity by FCCB holders. In such a scenario, the already troubled company may face an additional burden of interest and principal repayment to be made to the bondholders. Hence, an FCCB may be suitable in a bull market scenario and may be affected by bear market phases.

- Issuing bonds in foreign currency in a foreign market may always be exposed to legal, political, and economic risks of that foreign country. One may have a much better idea about the macro-economic conditions of the home country compared to those in a foreign country.

- FCCBs continue to remain on the books of accounts as a debt until the time it is converted and continues to hamper the debt to equity ratio and other debt and interest service coverage ratios.

Conclusion

These days, a foreign currency convertible bond has been in vogue primarily due to interest rate differential between different economies of the world and lower regulations for raising money via this route. The FCCBs can be issued along with call option (whereby the right of redemption lies with the bond issuer) or put options (whereby the right of redemption lies with the bondholder). The coupons on the bond can be zero coupons or usually lower coupons. Also, the bonds can be issued at a premium or discount depending on the coupon provided. Given these flexibility and cost-saving attributes, the volumes on the issuance of foreign currency convertible bonds have gone up considerably, with more and more investors trying to get into this option.