In order to understand the coupon rate, it is important to understand fixed-income securities first. Every now and again, government institutions and public companies are in need of funds. The funds come in two forms – Equity & Debt. Fixed-income security comes under the latter. Whenever an institution wants to raise debt from the open market, they issue fixed income securities such as bonds, mortgage-backed securities, asset-backed securities, etc.

These fixed-income securities come with a maturity and coupon rate.

Today we are going to limit our discussion to the coupon rate.

What is a Coupon Rate?

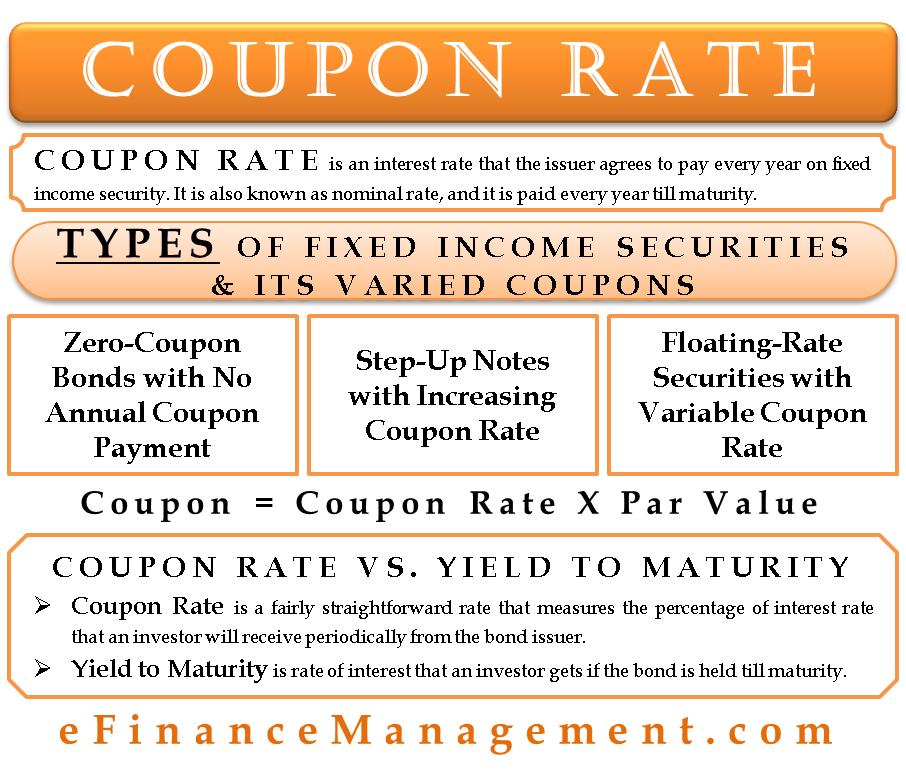

The coupon rate is an interest rate that the issuer agrees to pay every year on fixed income security. It is also known as the nominal rate, and it is paid every year till maturity.

The method to calculate coupons is fairly straightforward. The coupon is calculated by multiplying the coupon rate by the par value (also known as face value) of the bond. The par value of a bond is the amount that the issuer agrees to repay to the bondholder at the time of maturity of the bond. In formula it can be written as follows:

Coupon = Coupon Rate X Par Value

Let’s understand this by taking an example.

Example of Coupon Rate

Suppose Maxwell Ltd. has issued a bond at a par value of USD 500.00 & a coupon rate of 9% maturing in December 2024.

Thus the coupon would be-

Coupon = 0.09 X 500.00 = USD 45.00

This means that bondholders will get USD 45.00 every year up until 2024, i.e., the year of maturity.

The tricky thing is the coupon rate of a bond also affects the price of the bonds in the secondary market. The bond price is sensitive to the coupon rate.

At this point, we can discuss the different types of coupon rates in different types of fixed income securities. Not all fixed income securities are the same; therefore, there is a difference in coupons. Let’s understand this better.

Types of Fixed Income Securities and its Varied Coupons

Zero-Coupon Bonds with No Annual Coupon Payment

It is impossible not to discuss zero-coupon bonds when talking about coupon rates. The zero-coupon bonds do not make any coupon payments. The holder of these bonds buys them at a substantially lower price than the par value (i.e., discounted price). So, let’s say an investor purchases a zero-coupon bond at USD 12.00 with a par value of USD 20.00 at maturity; therefore, the coupon is actually USD 8.00 that the investor will get only at the time of maturity, with no annual payments.

Step-Up Notes with Increasing Coupon Rate

Another security that has a unique coupon structure is step-up bonds. These are bonds that have a coupon rate that increases over time. For example, a 5-year step-up bond of the par value of USD 100.00 may have a coupon rate of 5% for the first 3 years and 7% for the last two years. Thus the coupon payment looks as follows –

| YEAR | COUPON RATE | COUPON PAYMENT |

| Year 1 | 5% | USD 5.00 (0.05 x 100.00) |

| Year 2 | 5% | USD 5.00 (0.05 x 100.00) |

| Year 3 | 5% | USD 5.00 (0.05 x 100.00) |

| Year 4 | 7% | USD 7.00 (0.07 x 100.00) |

| Year 5 | 7% | USD 7.00 (0.07 x 100.00) |

Floating-Rate Securities with Variable Coupon Rate

In floating-rate securities, the coupon rate need not be fixed over the life of the security. These securities have coupons tied to a reference rate, and the coupons are reset periodically according to changes in the reference rate.

Also Read: Deferred Coupon Bonds

A typical coupon rate formula would be –

Coupon Rate = Reference Rate + Quoted Margin

The quoted margin is the additional amount that the issuer agrees to pay over the reference rate. For example, suppose the reference rate is a 5-year Treasury Yield, and the quoted margin is 0.5%, then the coupon rate would be –

Coupon Rate = 5-Year Treasury Yield + .05%

So if the 5-Year Treasury Yield is 7%, then the coupon rate for this security will be 7.5%. Now, if this coupon is revised every six months and after six months, the 5-Year Treasury Yield is 6.5%, then the revised coupon rate will be 7%.

The coupon rates of such floating-rate securities come with a floor and a cap, which means the rate cannot decrease below the floor and cannot increase above the cap. Following our above example, suppose the bond comes with a floor of 5% and a cap of 10%. Therefore, if the 5-Year Treasury Yield becomes 4%, still the coupon rate will remain 5%, and if the 5-Year Treasury Yield increases to 12% yet, the coupon rate will remain 10%.

Coupon Rate Vs. Yield to Maturity

Many people get confused between coupon rate and yield to maturity. In reality, both are very different measures of returns. As discussed, a coupon rate is a fairly straightforward rate that measures the percentage of interest rate that an investor will receive periodically from the bond issuer. However, the yield to maturity is slightly complicated. To understand yield to maturity, we must be familiar with some characteristics of a bond as follows:

- Bonds are traded in the secondary market.

- The market price of a bond can be at a discount, at a premium, or at par with the face value of the bond.

- The investor can buy or sell the bond anytime, and an issuer does have an option to call a bond before its maturity. This means it is not necessary that the bonds will be held up until the date of maturity.

Now let’s understand yield to maturity. Yield to maturity is the rate of interest that an investor gets if the bond is held till maturity. Breaking it down to a little more easy language – if you buy a bond today and hold it until maturity, the return that you earn on that bond is yield to maturity. Calculation of yield to maturity considers the bond’s market price, its coupon payments, and its face value.

As a matter of fact, the market price of a bond is determined by comparing the coupon rate with the yield to maturity of that bond –

| Coupon Rate – Yield to Maturity Relationship | Bond Selling at – i.e. (Market Price of Bond) |

| Coupon Rate = Current Yield = Yield to maturity | Par |

| Coupon Rate < Current Yield < Yield to maturity | Discount |

| Coupon Rate > Current Yield > Yield to maturity | Premium |

Quiz on Coupon Rate