Bridge Loan: Meaning

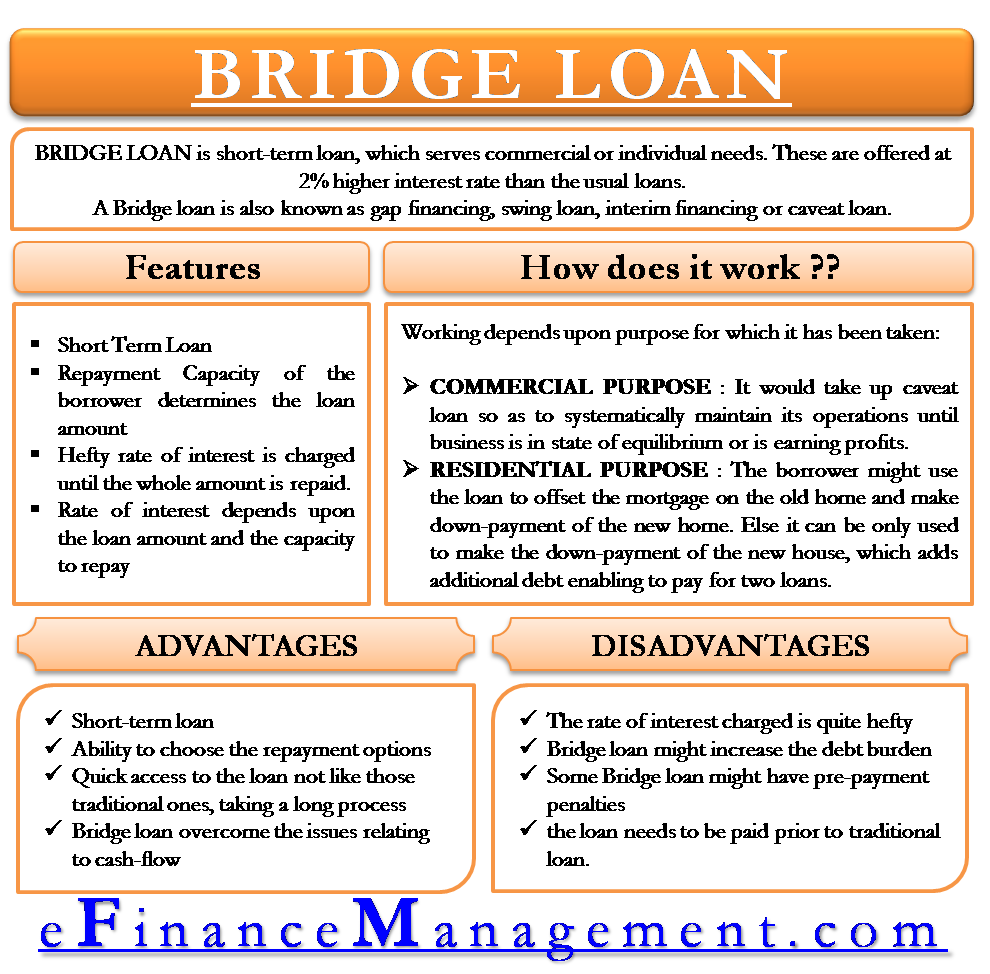

A bridge loan is a type of short-term loan which serves commercial or individual needs. The loan is backed by collateral securities like bonds, debentures, real estate property, etc. It is offered at a 2% higher interest rate than the usual loans. Until a permanent source of funding is generated, the loan bridges the gap between two consecutive funding periods. The loan gives borrowers access to a short-term loan, enabling quick liquidity, i.e., cash in hand to fulfill the current obligations. The loan term ranges from 2 to 3 weeks and can extend up to 12 months.

A bridge loan is also known as gap financing, swing loan, interim financing, or caveat loan. The loan can be used for various purposes, such as investing in a home property or for commercial uses like development. Suppose considering today’s increasing needs of environment and society with no appropriate resources available on time. An individual is looking for something that can meet their current need, such as a bridge loan, which does not take a long time to process the loan application as in the case of traditional loans.

Features of Bridge Loan

- It is a short-term loan.

- The repayment capacity of the borrower determines the loan amount.

- A hefty rate of interest is chargeable on the whole loan amount.

- The rate of interest depends upon the loan amount and the capacity to repay of the borrower, and the collateral offered.

You may like watching the Video on the article Bridge Loan.

How does the Bridge Loan Work

Working of the Bridge loan depends on the purpose of the loan.

Commercial Purpose

A commercial bridge loan can be used to renovate, expand the existing business, and shift to a new office. It can be used to overcome issues related to cash flow and so on. One can even use this loan to improve their credit score. For example, an early start-up might be struggling with finances. Therefore, for the smooth, hassle-free working of the start-up, it would take up the caveat loan to systematically maintain its operations until the business is in the state of equilibrium or is earning profits.

Residential Purpose

A residential bridge loan can be taken up when an individual is planning to buy a new house before selling the old one. He might use the loan to offset the mortgage on the old home and make a down payment for the new home. Note that the borrower can use it to pay for the down payment of the new house. This is also an additional debt allowing to pay for two loans.

Also Read: Types of Term Loans

For example: Suppose you have a house worth $500,000 with a mortgage loan amount ranging from $600,000. You are still liable for making the down payment of a new house and paying off $100,000 for the remains of the mortgage loan. If you sell the house, you still need to pay $100,000. If you feel stuck, then you can go for interim financing for a loan amount of $200,000. By using this amount, one can repay both mortgage loans.

How to Get a Bridge Loan?

One can avail gap financing from a bank, private lender, or credit union for residential or commercial purposes. But one should avail of this loan by going to a Financial Conduct Authority regulated broker. There might be some lenders who do not follow the strict guidelines of underwriting, enabling no hard fast rule for a credit score, debt-service coverage ratio, or other such requirements. There are two grounds for approval of this loan –

- Cash generating Purpose

- Repayment capability of the borrower.

Advantages of the Bridge Loan

- Short-term loan

- Ability to choose the repayment options

- Quick access to the loan is not like those traditional ones; taking a long process.

- This loan overcome the issues relating to cash-flow

Disadvantages of a Bridge Loan

- The rate of interest charged is quite hefty

- This loan might increase the debt burden

- Some Bridge loans might have pre-payment penalties

- This loan has a shorter payback duration

Bridge loan vs. Traditional loans

Bridge loans break the norms of traditional loans with faster procedure, funding, and approval. The loan is a short-term duration with a high rate of interest and origination fees. Borrowers accept the terms and conditions of this loan before availing it. This can be easily done as it is not a time-consuming process and provides quick access to funds.

Fee Structure for Bridge Loan

- Administration fee

- Appraisal fee

- Escrow fee

- Title policy fee

- Notary fee

- Recording fee

- Wire/courier/drawing fee

Few Examples of Bridge Loan Lenders

- Veristone

- Thorofare Capital

- George Mason Mortgage

- GUD Capital

Conclusion

Before deciding on a Bridge loan, the borrower must decide and compare it with various other loan products available. Every product comes with its own set of risks and rewards. A bridge loan might be a viable option for many borrowers. There are many risk exposures one needs to take. The borrower needs to have a bridge loan – Whether the old property will sell or not if buying a new one, to set off the mortgage loan of the old property and make the down payment for the new one.