There are times when you require quick funds, such as a medical emergency, any major purchase, travel plans, etc. At such times, it might not be possible to arrange collateral to go for a secured loan. In this situation, the borrower has the option to go for unsecured personal loans.

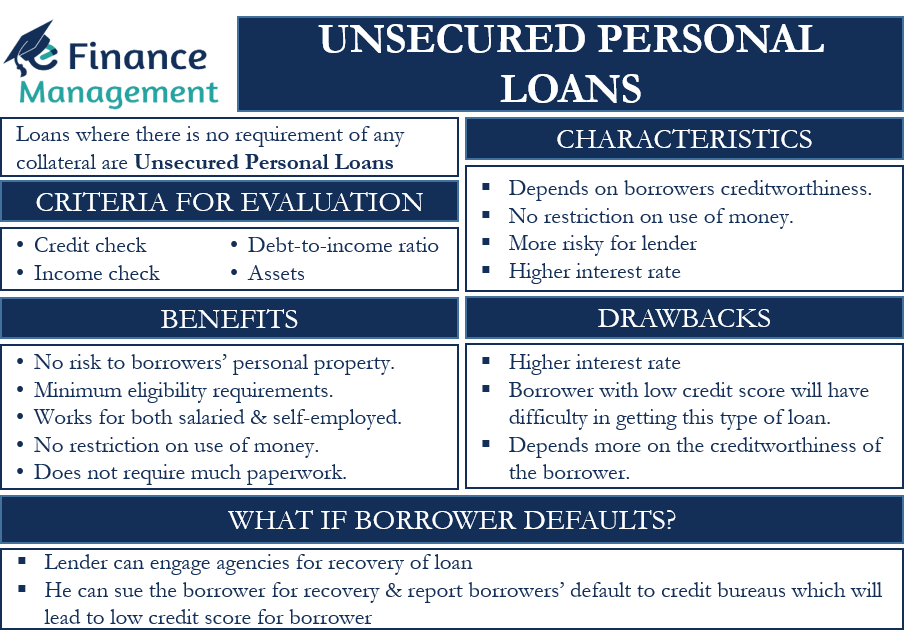

Unsecured Personal Loans are types of personal loans where there is no requirement of any collateral. Such loans depend entirely on the creditworthiness of the borrower, as well as the trust between the lender and the borrower. The borrower can use the loan money on anything as there are no restrictions on the use of the money. Moreover, the borrower needs not to provide the details of the utilization of the funds to the lender.

Since this loan does not involve any collateral or security, the risk level is more for the lender. Because of this, lenders charge a relatively higher interest rate on this type of loan than on secured personal loans.

Talking about how it works, when a borrower submits an application, the lender verifies the creditworthiness of the borrower. Also, the lender considers other factors, such as borrowers’ income, savings, and debt.

Unsecured Personal Loans: Benefits and Drawbacks

The benefits of taking unsecured personal loans are:

- Since this loan does not involve any collateral, there is no risk to borrowers’ personal property. This means if the borrower is unable to pay the loan, then they will not have to part away with their asset or any other security. So the risk of losing the property is not there. And that is the biggest advantage of this type of loan.

- These loans have minimum eligibility requirements.

- This loan works for both salaried and self-employed people.

- The money lent has no restrictions with regards to its usage. The borrower can use the loan money on almost anything, including holidays, weddings, medical expenses, and more.

- The rate on this type of loan is more than the secured loan, but it could offer a lower interest rate than many credit cards. So, if one is paying more interest rates on his credit card, then he could consider taking a personal loan.

- Such a type of loan does not require much paperwork as it does not involve any collateral documents. Since it does not include much paperwork, it leads to quick approval.

- Since it is a type of personal loan, the borrower may get an option to decide the repayment term and the money they want to shell out as EMIs.

There are, however, certain disadvantages of unsecured personal loans. And these are:

- Individual’s credit score is still relevant in this type of loan too. Hence, the borrower with a low credit score will have difficulty getting this type of loan. Or, those with a low credit score may qualify for a low loan amount.

- The Interest rates on these types of loans are usually higher than many other types of loans.

- This loan could be harder to get as it depends more on the creditworthiness of the borrower, as well as the terms between the lender and the borrower.

Criteria to Evaluate Borrower

The key concept of the repayment capacity of the borrower becomes very critical and important in the case of unsecured personal loans. As here also, the lender wants to ensure that the borrower repays the loan timely. The lenders provide this by verifying the following parameters:

Credit Check

Lenders verify your credit history, including how you are managing your current loan, as well as the past loans. They basically want to see responsible credit behavior. This means whether or not you make timely payments, how you use the credit, etc. Lenders also check your credit scores.

Income Check

In this check, the lenders want to know the source of the borrower’s regular income and how one would like to repay his loan. The lenders here want proof of stable and sufficient income to cover the loan amount.

Debt-to-Income Ratio

A debt-to-income ratio says a great deal about the financial condition of an individual. It tells how much debt you have for every dollar of your income. The lower the ratio or, the lower the total loans vis-a-vis income, the better it is. This ratio tells about your capability to pay back the loan. There is nothing like an ideal or standard benchmark ratio that the borrower needs to meet. Because different lenders have different criteria. But most lenders consider a debt-to-income ratio of over 40% as bad.

Assets

Even though such types of loans do not require any collateral, a lender still wants to know if the borrower has assets. If the borrower has the assets, it adds to his creditworthiness and gives borrowers some peace of mind.

What if a Borrower Default?

In the case of unsecured personal loans, the risk is more for the lender as it does not involve any collateral. So in case of a default for such types of loans, the lender has nothing to confiscate and dispose of to get his loan money back.

Still, defaulting on the unsecured personal loan could prove bad for the borrower. Yes, the lender can not take away the collateral, but they have several other recourses available.

- The first one is to engage a collection agency for the recovery of the loan granted to the borrower.

- Secondly, the lender can sue the borrower to recover his loan money.

- Thirdly, the lender can report about the borrowers’ default to the credit bureaus. Such an action from the lender could tarnish the image and reduce the borrower’s credit score. And it adversely hits the chances of borrowers to get further loans.

Unsecured Personal Loans: Who Should Go For It?

Borrowers who do not have collateral should consider this loan:

- If one is looking for money for a big upcoming expense, then one could consider taking such a loan.

- If one has a good credit score, then going for this type of loan could get the borrower more favorable loan terms.

- This type of loan could prove a good option for borrowers having a reliable income stream because the repayment capacity is an important aspect for grant of such loans. Hence, having a steady income source will make it easy for the borrower to get such a loan even in the absence of an asset/collateral.

- Such type of loan could prove a good option for borrowers who wish to consolidate their other loans. Consolidation of loans could make debt repayment simpler.

Unsecured Personal Loans: How to Apply?

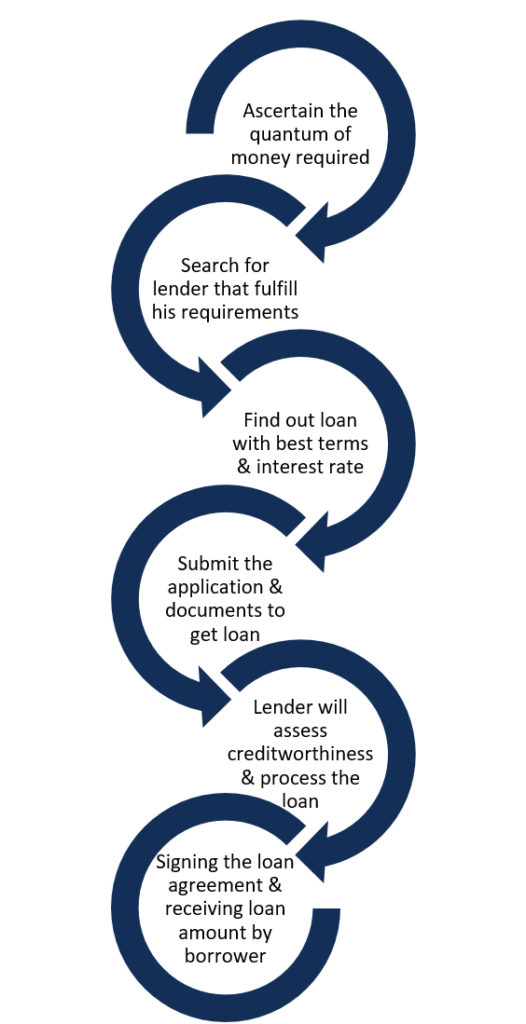

If one has decided that an unsecured personal loan is the right choice for him, then to apply for it, the borrower needs to follow the below simple steps:

- First of all, the borrower needs to decide the quantum of money he requires. One must take only the amount one needs. Even if the lender sanctions is willing to advance more money.

- There are many lenders in the marketplace that offer such loans. So, the borrower must research all the top lenders to decide on the lender that best fulfills his requirements.

- Next is to find out the loan one would qualify for. One lender could offer a variety of unsecured personal loans that differ in interest rate, loan terms, and more. So, one must find out from the lender the loan (or loan terms) one is qualified for.

- Once the borrower is sure about the lender and the loan terms, then one needs to submit an application to get the loan. This application can be submitted online or offline as per the process and requirements of the lender.

- Together with the application, all the supporting documents should also be submitted by the borrower. These documents will help the lender to assess the borrower’s creditworthiness.

- Upon approval of the loan by the lender, the borrower needs to sign off the loan agreement and other documents. These documents will in detail covers the quantum of loan, interest rate, repayment schedule, as well as other terms and conditions.

- The sanctioned loan money will be received once the loan documents are signed off by the borrower. The funds will usually be released in one go. And if it is a one-time facility, then also funds are released only once. However, if it is a revolving loan, then the borrower can draw the money out as and when one needs it.

Final Words

A borrower must consider the pros and cons of an unsecured personal loan against their own objectives to decide whether or not they want this type of loan. Moreover, they should compare the features of this loan with other types of loans to decide on the best alternative for them. And the same is applicable while deciding on the lender from whom they would prefer to borrow. The preference and selection depend upon the quantum of loan, interest rate, repayment period, penalties, and other terms and conditions.