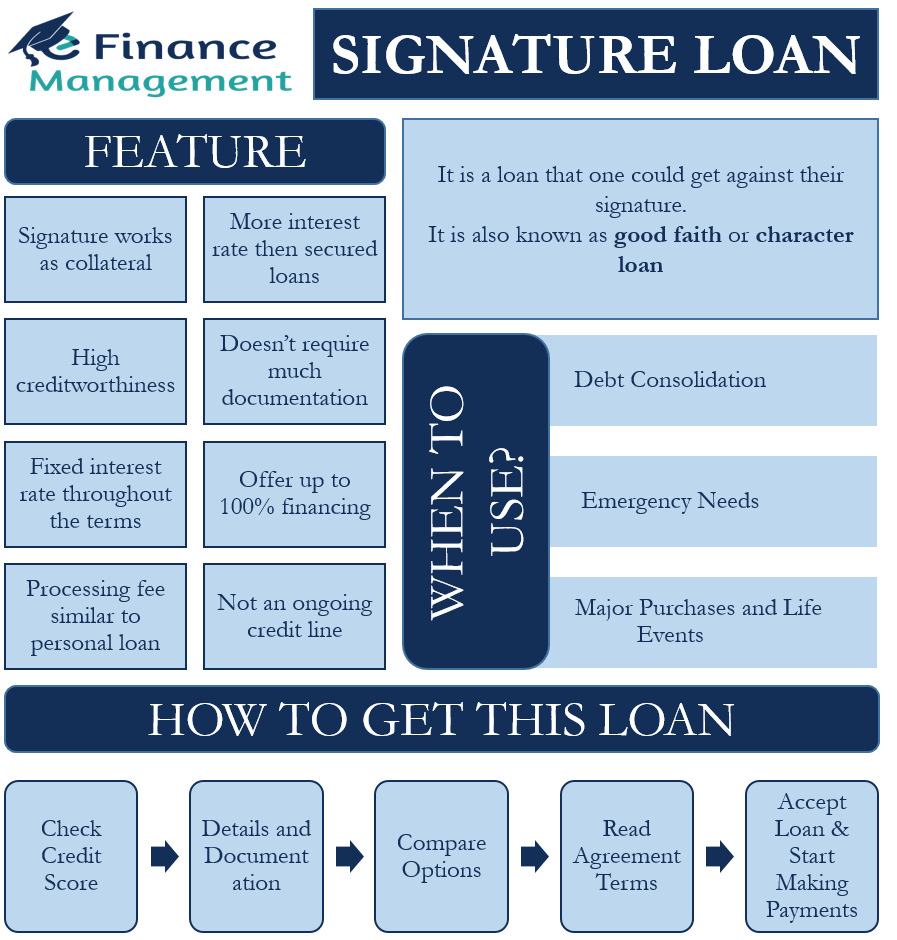

A Signature Loan, as the word suggests, is a loan that you could get against your signature. It is a type of personal loan where the lender gives the loan against the signature and promise from the borrower to repay the loan. So, we can say that the signature and promise of the borrower work as collateral in this type of loan. Other names for this loan are “good faith” or “character loan.”

A signature loan is a type of term loan. So this means a borrower can pay it off in monthly installments over the term of the loan. Also, these loans have comparatively higher interest rates than secured debt. An important point to note is that this loan is unlike many other types of loans in a way that once you pay it off, it ends. This means there is no ongoing line of credit, like with a credit card or a revolving loan.

Features of Signature Loans

Below are the features of this type of loan:

- This loan does not require the borrower to submit any collateral or asset to get the loan. The signature and promise of the borrower work as collateral.

- The interest rate on this type of loan is always relatively more than what is payable on secured loans. This is because the former does not need any collateral and, thus, is riskier for the lender.

- Borrowers with high creditworthiness are more likely to win approval for this type of loan.

- Before applying for this type of loan, do ensure that one has not failed any EMIs or declared bankruptcy for at least prior two years.

- If one uses a credit card, then ensure one has a low due amount. This raises the borrower’s chances of getting the loan.

- Lenders generally check borrowers’ debt-to-income ratio to decide whether or not to approve this loan.

- Such loans do not require much documentation, so the application process is quick and simple.

- These loans usually carry a fixed interest rate throughout the loan term.

- Such loans generally offer up to 100% financing so that one can fully meet his financial needs.

- The processing fee for this type of loan is similar to personal loans.

- It is not an ongoing credit line. This means it ends once a borrower fully pays back the signature loan.

How it Works?

Lenders basically evaluate the borrowers’ ability to repay the loan to approve the loan. Specifically, the lenders check the borrowers’ credit score, their credit history, as well as their debt-to-income ratio to decide whether or not to approve their loan application.

If borrowers’ application gets approval, they will get the loan in a lump sum. They need to repay the loan via monthly installments over a set term, which is usually two to seven years.

The approval of this loan is quick, and so is the disbursal. So, once the lender approves the loan, the borrower will get the loan amount faster. Such a feature makes it an attractive option for borrowers who need quick funds.

These loans carry a fixed annual percentage rate. And this includes the interest, as well as fees if any.

How to get a Signature Loan?

If the applicant is planning to go for this type of loan, then following the below steps will help you to get it faster:

Check Credit Score

Before applying for this loan, it is crucial that the borrower checks his credit score. In case the applicant’s score is less, then one should work on improving it. Because the higher the credit score, the higher would be chances of getting approval for the loan. Also, a higher score would help the borrower secure favorable loan terms. So, if one does not need the loan for any emergency, then it will be better to improve your credit score first.

Details and Documentation

Like other loans, when applying for the signature loan, one will need to share his personal and financial details with the lender. The applicant needs to share the details of his monthly income, his monthly expenses, his monthly repayments, EMI obligations, and similar other details with the lender.

A point to note is that with disclosing the details mentioned above, the borrower also needs to provide proof for the same.

Compare Options

It is important that the borrower evaluates all the options available for the signature loans. Doing this will help to make a better decision and get the most favorable loan terms. One must go for a lender with the best interest rate, flexible repayment terms, and quick approval without much hassle.

Also Read: Sources of Loan

A caution here is that in the process of finding better terms, one should not apply for too many loans as it affects the credit score, which might create a problem afterward.

Read Agreement Terms

Once the borrower finalizes the lender and the loan, one must not sign the documents straight away. Instead, carefully read the terms of the agreement before signing it. It is crucial that one is very clear on the prepayment penalties, late payment fees, and any other fee that can raise the overall cost of the loan.

Accept Loan and Start Making Payments

After the applicant is satisfied with the lender, loan terms, and loan agreement, one should accept and sign the loan documents. Once the applicant receives the funds, it is preferable that one sets up an auto-payment mechanism for the regular installments. This will help one to avoid missing any due dates and payments. Also, if one can, try to make extra payments. This would help the borrower to retire the loan early.

Online Signature Loans

The loan where the applicants submit the application with an online signature and the loan is approved with that online signature is known as Online Signature Loan. It is commonly used in United State.

Signature Loan: What it is Used For?

Usually, borrowers use this type of loan for the following purposes:

Debt Consolidation

If you are able to get a signature loan at a rate less than what you are paying on the credit card or your other loans, then it is better to consolidate all loans under one signature loan.

Emergency Needs

Such loans have a quick approval time. And this feature makes them perfect for meeting sudden expenses, such as medical needs.

Major Purchases and Life Events

If one needs large sums for bigger items like a car or creating capital assets like a home, then one can also go for such a loan. The applicant can also use this loan to meet wedding expenses or to pay for the vacation.

Final Words

If the applicant is looking for a quick short-term loan, then a signature loan could be an excellent choice. But before going for this loan, one must ensure their repayment plan is ready. In a repayment plan, it is important to review the borrower’s budget, monthly expenses, and sources of income. Such a loan may fit the need but could prove expensive as well. So, before selecting a particular loan, one must evaluate all the other options to arrive at the best favorable rates and terms.