The regular letter of credit and standby letter of credit (LC & SBLC) are payment instruments used in international trade. However, there are some basic differences in the product, which we will discuss in the following post –

Meaning of LC & SBLC

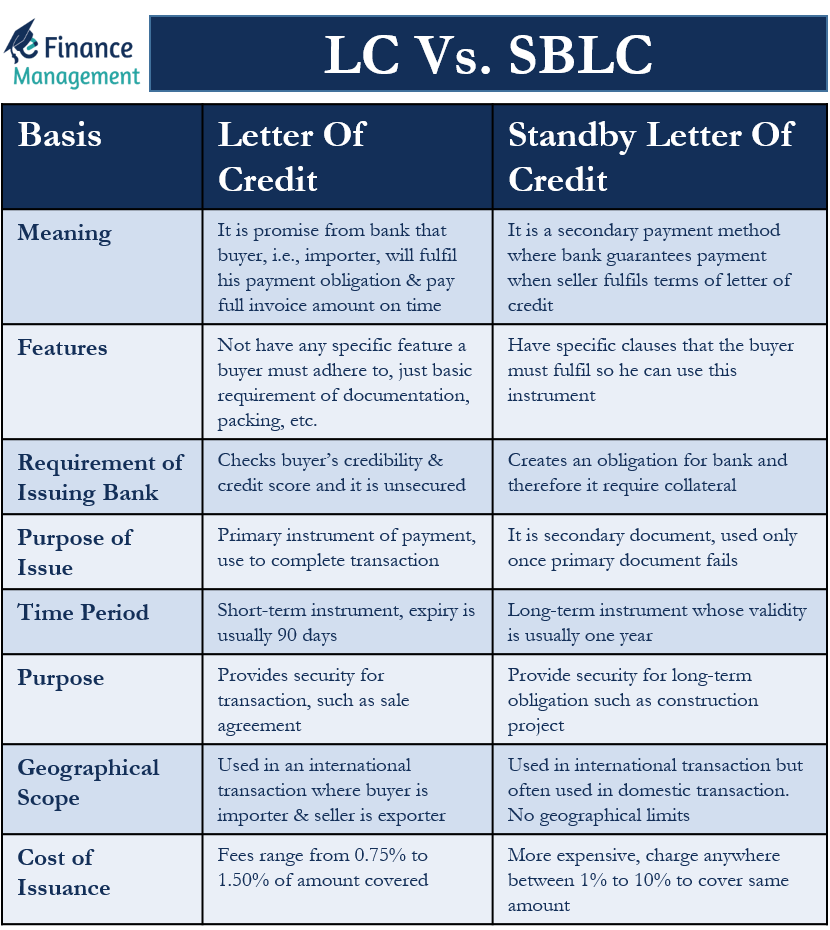

A letter of credit is a promise from the bank that the buyer, i.e., the importer, will fulfill his payment obligation and pay the full invoice amount on time. The role of the issuing bank is to make sure that the buyer pays. In case the buyer is unable to fulfill his obligation, the bank will pay the seller, i.e., the exporter, but the funds come from the buyer.

On the other hand, a standby letter of credit is a secondary payment method where the bank guarantees the payment when the seller fulfills the terms of the letter of credit. It is a kind of additional safety net for the seller. The buyer may not pay the seller for multiple reasons such as cash flow crunch, dishonesty, bankruptcy, etc. But as long as the seller meet’s the requirement of a standby letter of credit, the bank will pay.

Difference between LC & SBLC

Though both these instruments are issued by the bank at the request of the buyer and used for most international trade, there are basic differences in both the instruments. The key differences are:

Also Read: Standby Letter of Credit

Features

A letter of credit does not have any specific features that the buyer must adhere to complete a transaction. It does have basic requirements such as documentation, packing, etc. But all in all, it’s a plain vanilla payment instrument.

A standby letter of credit may have specific clauses that the buyer must fulfill so he can use this instrument. For example, Mr. Harry, who resides in the UK, agrees to buy 5000 pairs of socks from Mr. Chang, who resides in China. Mr. Chang does not want to take the risk, so he asks Mr. Harry to get a standby letter of credit. Mr. Harry obtains a standby letter of credit from HSBC bank, and he adds the following clauses –

- The material of the socks should be – 80% cotton, 20% polyester

- Each pair should be packed in a clear plastic bag having a logo tag

- There can be only a 1% defect margin, i.e., only one pair of defective socks in a hundred pairs is acceptable

Mr. Chang should fulfill all the above-mentioned performance criteria to be eligible for payment through a standby letter of credit. A regular letter of credit cannot have such performance criteria

The Requirement of Issuing Bank

When issuing a letter of credit, the bank checks the buyer’s credibility and credit score. Furthermore, it is usually the case that a buyer asks his banker for a letter of credit, i.e., the buyer is usually dealing with the said bank for a long time. So the letters of credit are usually unsecured.

Also Read: Types of Letter of Credit (LC)

Conversely, a standby letter of credit creates an obligation for the bank. Therefore the bank will require collateral in the form of security to issue a standby letter of credit.

Purpose of Issue

The letter of credit is a primary instrument of payment, so the goal is to use the letter of credit to complete the transaction. It provides security and assurance to the seller that the buyer will pay for the supply of goods. And this is the standard payment document used for an international transaction where mostly both the parties are unknown to each other.

In contrast, a standby letter of credit is a secondary instrument of payment. If a seller is paid by a standby letter of credit, it means that something went wrong with the buyer. However, the goal remains for all the parties involved to avoid using a standby letter of payment.

In other words, as the word standby itself suggests, a Letter of Credit is the primary document, and deals happen with that document mostly. And Standby Letter of Credit is a secondary document, used only once the primary document fails. Therefore, SLC remains a standby document and is used exceptionally.

Time Period

A letter of credit is a short-term instrument, where the expiry is usually 90 days.

A standby letter of credit is a long-term instrument whose validity is usually one year or so.

Purpose

A letter of credit provides security for a transaction, such as a sale agreement.

A standby letter of credit is often used to provide security for a long-term obligation such as a long-term construction project.

Geographical Scope

A letter of credit is usually used in an international transaction where the buyer is the importer, and the seller is the exporter.

A standby letter of credit is used in an international transaction, but it is also frequently used in domestic transactions. Its scope is not limited to any geographical area.

Cost of Issuance

A standby letter of credit is more expensive than a regular letter of credit. While the fees of a regular letter of credit range from 0.75% to 1.50% of the amount covered, a bank may charge anywhere between 1% to 10% to cover the same amount under a standby letter of credit.

Final Words

Both these instruments are extensively used in international and domestic trade transactions. The bank issues both at the buyer’s or importer’s request in favor of the seller or exporter of goods. It provides a payment assurance to the seller that the buyer will pay for the goods supplied, and his money will not be at stake. Moreover, in the case of a Standby Letter of Credit, it is a more prominent assurance to the seller that if he meets the obligations or performance criteria as per the SLC, then the buyer’s bank will have to make payment. This is irrespective of the situation of the buyer, which means the bank assures payment.

Quiz on LC Vs. SBLC

This quiz will help you to take a quick test of what you have read here.

Can a sblc open for one month