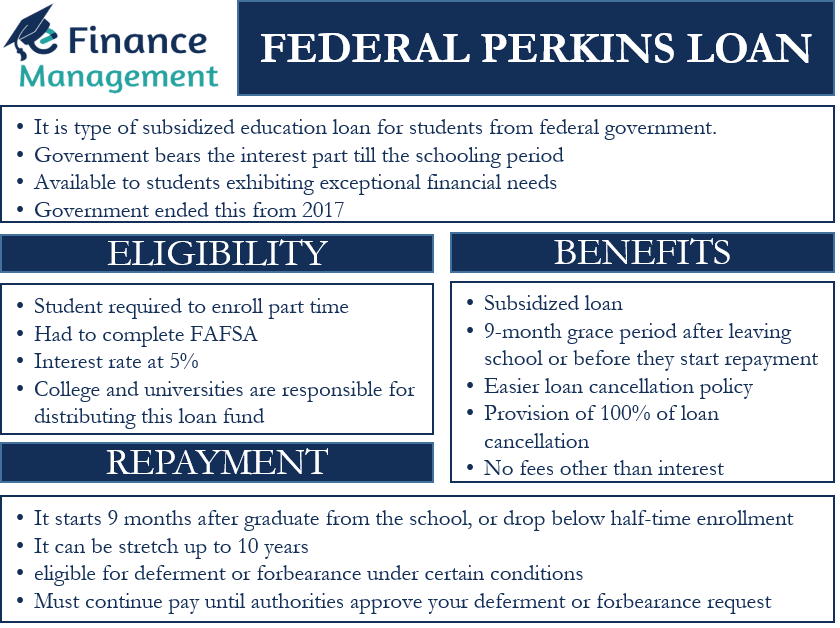

Perkins Loan was a type of federal education loan for students from the federal government. Under this, the government bears the interest part till the schooling period. This loan was available to students exhibiting exceptional financial needs. Perkins Loan featured a low rate of interest for undergraduate and graduate courses.

Perkins Loan dates back to the 1950s, and at the time, they were available only to students in need of financial support. Moreover, they were available only to students who were planning to take up mathematics, engineering, or a modern foreign language. Later, its scope was expanded to include students of all streams. However, this type of loan is not available anymore as the government ended it in 2017.

Eligibility and How to Apply?

To be eligible for the Perkins Loan, a student was required to be enrolled at least part-time.

For applying for Perkins Loan, one had to submit the FASFA (Free Application for Federal Student Aid) application. This helps to determine the financial need. This loan program was made available to more than 1,800 schools.

In terms of the interest rate, this loan was at a flat rate of 5%. A maximum loan of up to $5,500 each year was available for undergraduate students. The total limit for the full course was $27,500. Separately, a maximum of $8,000 per year was available for graduate and professional students. The total limit, in this case, was $60,000.

A point to note is that the Perkins Loan is a federal loan, but it is the college or universities that were responsible for its distribution. So, the maximum amount that one can get depends on the availability of the loan at your school. It means that even if you qualify for the full loan amount, there is no surety that you would be able to borrow the full amount every year.

Benefits of Federal Perkins Loan

These were the benefits available under Perkins Loan:

- It was a subsidized loan. So, the government was responsible for the payment of the interest part during the school term.

- Students get a 9-month grace period after leaving school before the repayment of the loan starts. Most other types of federal loans come with a 6-month grace period.

- This loan had an easier loan cancellation policy in comparison to other federal loans.

- For some public service fields (teacher, nurse, volunteering, and others), there was a provision of 100% of loan cancellation. Since this loan was for financially needy students, it was among the top in terms of loan forgiveness.

- This loan does not carry any other fees other than the interest. But, there was a late fee if the borrower made a late payment and a fee if the borrower missed any monthly payment.

Repayment of Federal Perkins Loan

Unlike many other types of student loans, it is the school that acts as a lender in Perkins Loan. So one had to work with the school, or any agency that represents the school, to get information on the repayment.

Generally, the repayment used to start 9 months after the student graduating from school or drops below half-time enrollment. The maximum repayment period of this loan could have gone up to 10 years. About the monthly repayment amount, it was dependent upon the loan amount, repayment period, etc.

This type of loan was also eligible for “deferment” or “forbearance” under certain conditions. However, the loan should not be in default status. Deferment allows the borrower to temporarily postpone the payment, and no interest accrues for that period. One had to fill out a deferment request form with their respective school to get a deferment.

If one was not eligible for deferment, then one has the choice to go for forbearance. Under forbearance, one either postpones or lowers the payment or extends the repayment period. However, the interest continues to accrue under forbearance, and the borrower needs to pay it. For forbearance, also one needs to apply with one’s school or the agency representing one’s school. The student needs to accompany his application with documents supporting his case for forbearance.

A point to note is that the student must continue to make payment until the authorities approve the deferment or forbearance request. If one discontinues the payment, it may push the loan into default.

There are also scenarios when this loan can be discharged, or the borrower will not have to pay it back. These scenarios are death, total and permanent disability, bankruptcy, and if the school shuts down before the course completion.

There is also an option for consolidation. So, if you combine your Perkins Loan with your other student loans, then you get more repayment options based on your income.

Final Words

Federal Perkins Loan was a crucial source of finance for students. It is estimated that 528,000 students used this loan in the 2014-15 academic year. The authorities initially decided to end the program in 2015 due to budgetary issues. But, in 2015, the authorities came up with Federal Perkins Loan Program Extension Act, intending to phase this loan program in two years. The expectations were that Congress would completely overhaul the student loan system by then. The Perkins loan program finally ended in 2017. And as per the instructions, no disbursement could happen after the 30th of June 2018 for the already sanctioned loan. The authorities, however, are still in the process of coming up with a replacement for the Perkins Loan Program.