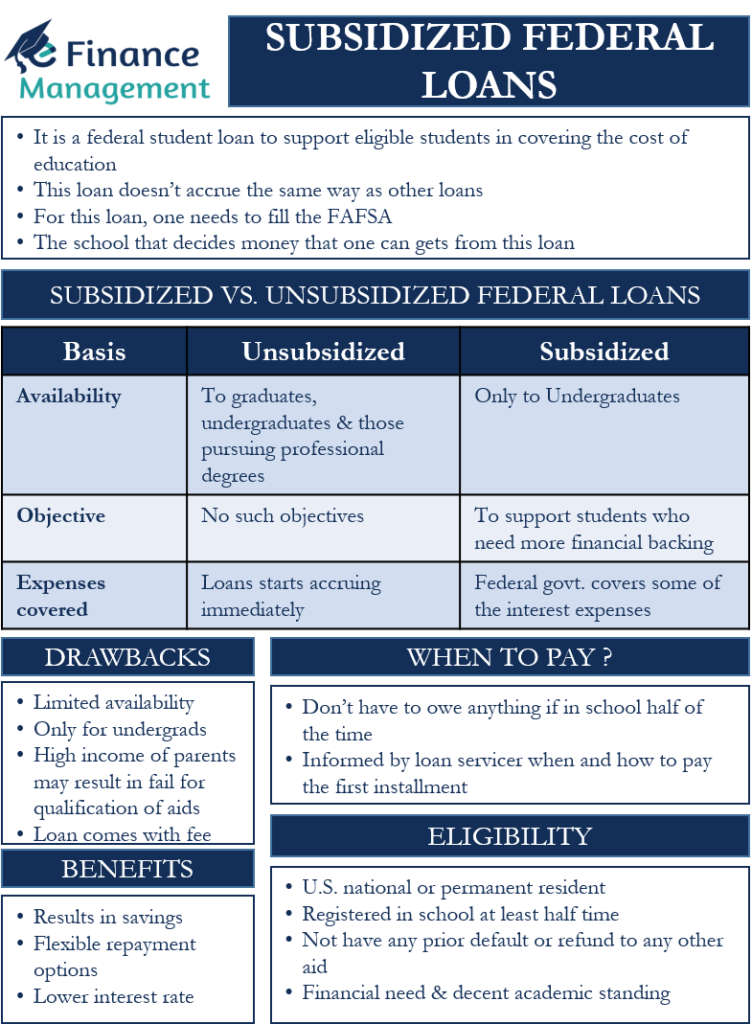

Subsidized Federal Loans is a term that one generally uses for a type of student loan. A subsidized federal loan is basically a federal student loan to support eligible students in covering the cost of education. This loan comes from the U.S. Department of Education and is available for the participating schools. As we know, the cost of studies is gradually increasing, and the student needs financial support. One can get private loans also, but that may have higher interest rates and security issues. Hence, the students prefer to go for Federal Loans, which have lower interest rates. About 43.4 million students have opted for Federal Direct Student Loans as of 2021.

Direct Federal Student Loans have two variants. One is subsidized, and the other is unsubsidized loans. Both these loans help to cover education costs for students. But what makes the two different is that the interest on the subsidized loan does not accrue the same way as on other loans. In a subsidized federal loan, the government covers the interest cost but only temporarily.

To apply for Perkins Loan, one must submit the FASFA (Free Application for Federal Student Aid) application. It is the school that decides the money that one can get from this loan. Moreover, this money can not be more than the students’ financial needs.

Subsidized vs. Unsubsidized Federal Loans

To better understand subsidized students’ loans, we must know the differences between subsidized and unsubsidized loans. We will list out below the key differences between both types of student loans:

- The subsidized loans are available only to undergraduates. However, unsubsidized student loans are available for all, whether they are pursuing a graduate or undergraduate program or a professional degree.

- The objective of subsidized loans is to support students who need more financial backing. And this is why students applying for this loan have to demonstrate financial need. In contrast, there is no such requirement for unsubsidized loans.

- In a subsidized loan, the federal government covers or pays the interest expenses on loan. Specifically, the government covers the interest (a) at least half-time during the schooling period, (b) for six-month after the student leaves the school, and (c)at the time of loan deferment. In contrast, the interest on unsubsidized loans starts accruing immediately. Moreover, the interest that remains unpaid before the grace or loan deferment period is capitalized.

There is, however, one significant similarity between these two types of loans. And it is that neither of the two applicants requires a credit check. Also, the interest rates on both the loans are the same but only for undergraduate students. The interest on such loans for undergraduates is 3.73% of that, which is disbursed during the period July 1, 2021, to 30th June 2022.

For all unsubsidized student loans, the interest rate is higher for all graduates and professional student applicants. The interest on such loans for graduates and professionals is 5.28% which is disbursed during the period July 1, 2021, to 30th June 2022.

Advantages and Disadvantages of Subsidized Federal Loans

Following are the benefits that a subsidized loan offers:

- Since the federal government covers some part of the interest expense, this loan results in a lot of savings.

- Such a loan comes with flexible repayment options that may not come with private loans.

- The interest rate is lower on this federal loan than on many other types of private student loans.

Following are the drawbacks that a subsidized loan offers:

- For all such loans, there remains a maximum limit up to which a student can borrow every year on an overall basis. Usually, the school decides the loan money a student would need. The school uses federal limits, students’ financial needs, and students’ years in school to determine the loan amount. In case a student needs more money, then they need to consider other loan options to get the balance money.

- This loan is only for undergrads. So, other (graduates and professional) students need to consider other loan options.

- A student applying for this loan needs to demonstrate a financial need. So, if their parents’ income is high, they may fail to qualify for the aid.

- This loan comes with a fee, and this fee hinges on the loan sum. The fee gets deducted from each payout.

Subsidized Federal Loans: Eligibility Criteria and How to Apply

To be eligible for this loan, a student is required to fulfill the following criteria:

- The applicant must be a U.S. national or permanent resident.

- One should be enrolled in the school at least half-time that participates in the Federal Direct Loan Program.

- Applicant must not have any prior default or refund to any other student loan or aid.

- Students should have financial needs.

- A decent academic standing.

To apply for this loan, applicants need to fill out the FAFSA. After this, the school and government authorities will review your application. And, if all is okay, you will get a sanction letter from the school detailing the loan money you are eligible for and if you qualify for a subsidized loan.

The applicant needs to sign a Master Promissory Note if he accepts the loan offer received. This note covers the details of various terms and conditions that you agree to avail of the loan. If you are a first-time borrower, you also need to go through online student loan counseling, which clarifies the financial obligations.

After all the formalities are over, the school will use the loan money to pay for students education-related expenses, including tuition fees, room rent, and more. If any money remains after paying for these expenses, then the school pays it back to the student. The student then needs to use it for education expenses.

Subsidized Federal Loans: When to Pay?

The best part of the subsidized federal loans is that if the student continues in the school at least for half time, then he does not owe anything. But, once the student leaves the school, the loan servicer from the school will inform the student of the due date of his first payment and how he needs to pay it.

A point to note is that a subsidized federal loan comes with different repayment plans. It is possible that authorities automatically assign the student a repayment plan. But, the applicants are free to change it. He should contact his loan servicer to get more details on the plan, including the best plan for the student.

Experts always recommend starting repaying the loan as soon as possible. Also, if one could shell out more than the installment, then it is even better. If one is paying more, then he can retire the loan early, as well as save on the interest in the long term. But, while making a bigger payment, the student must inform about the same to his loan servicer.

If the student has more than one loan, then paying extra on the subsidized federal loan should not be the only option. The student should evaluate the loan with the highest interest rate and the amount and then put the extra money towards that loan. One’s aim should be to put the extra money toward the more expensive loans.

Also, if one is facing issues with the repayment, then he must inform about the same to his loan servicer. The loan servicer will assist the student in understanding the options that the student may have to keep the loan in good standing. For example, the loan services could change the repayment plan to reduce the monthly payment. Or, one can also avail of deferment or forbearance that temporarily stops or reduces the payment.

Final Words

Subsidized Federal Loans could prove a great source of finance for students to fund their education. However, like with any other thing, this type of loan also has its own drawbacks and benefits. Their biggest benefit is that the government covers some part of the interest expenses, but they are only available for undergraduates. So, the student must evaluate these drawbacks and benefits, as well as his needs to decide whether or not he needs to go for this type of loan.

RELATED POSTS

- Federal Perkins Loan – Meaning, Eligibility, and Benefits

- Parent PLUS Loan – Meaning, Eligibility, Interest Rate, Benefits and Drawbacks

- Types of Interest Rates

- Types of Personal Loans – These Are The Options You Have

- Discount Rate – Meaning, Importance And More

- Unsecured Personal Loans – Meaning, Benefits, Criteria, and Application