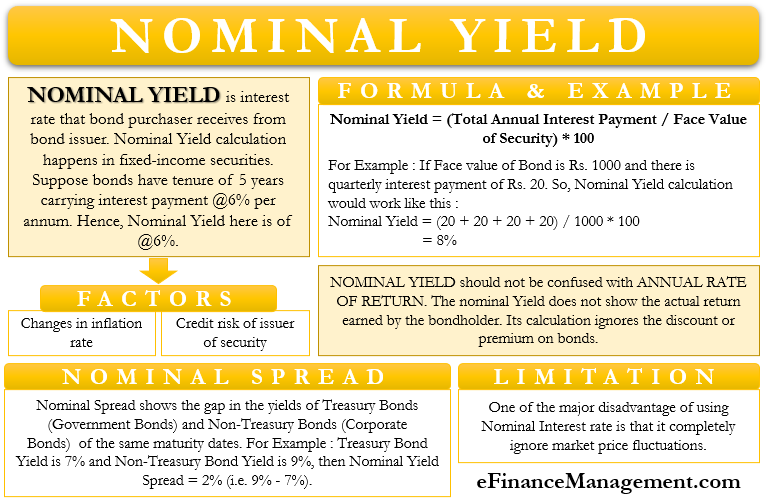

Nominal Yield: Meaning

Nominal Yield, also known as Nominal rate or Coupon yield, is the interest rate that the bond purchaser receives from the bond issuer. In other words, it is a fixed coupon rate that the bond issuer promises to pay to the bond subscriber for the whole lifetime of the bonds. Suppose the Bonds have a tenure of 5 years carries an interest payment every year at the rate of 6% per annum. Hence, a Coupon yield of @6% will be provided to the bondholders for a period of 5 years.

For the computation of Nominal Yield, all the annual interest payments are divided by the par value of the bond. Here the consideration is the total annual interest payments that are taking place. Whether the interest calculation and payments happen annually, biannually, monthly, or quarterly, all the interest payments are taken to calculate the nominal yield.

Here the expression of coupon rate or interest rate is always in percentage terms. The computation of the rate completely depends on the face value and interest payments of the bond. The Coupon rate of Bonds forms part of its name, like 6.5% ABC Bonds. Thus it becomes easy for the investors to compare various bonds by comparing their coupon rates.

Nominal Yield calculation happens in fixed-income securities, which promise to pay a fixed rate of return on their investment. Major fixed income securities are Bonds, Treasury Bills, Guaranteed Investment Certificates (GIC), certificates of deposits, convertible bonds and non-convertible bonds, etc.

Nominal Yield: Formula

Nominal Yield = Total Annual Interest Payments * 100

Face/ Par Value of a Bond

As shown above, all annual interest payments made by the bond issuer are taken into the calculation. Moreover, these interest payments are further divided by the par value of the bond. For the Nominal Yield calculation, the discount or premium, or issue price of bonds is not considered

Nominal Yield: Example

Face Value of Bond: Rs 1000

1st Quarter Interest Payments: Rs 20

2nd Quarter Interest Payments: Rs 20

3rd Quarter Interest Payments: Rs 20

4th Quarter Interest Payments: Rs 20

Nominal Yield = (20+20+20+20) * 100

1000

= (80/ 1000) * 100

= 8%

Components Determining Nominal Yield

Inflation Rate

While calculating returns on investments, the calculation of the inflation rate becomes very crucial. Because the actual or net rate of return varies with the change in the inflation rate, any increase in the inflation rate will mean a downward revision in the actual rate of return and vice versa. For example, if the Inflation rate is 7%, the return on investment or coupon rate is 10%, and as a result, the real interest rate would be 3% only (10-7). Thus if the inflation is higher than the Coupon Yield, it also has to be higher to compensate the investor from the loss of inflation.

As a result, at the time of the Nominal Yield’s computation, consideration of the inflation rate becomes very important.

Credit Risk of Issuer

Credit rating agencies like S & P Global Ratings, Moody’s, Fitch Group, etc., are continuously rating the companies based on their financial soundness. Thus the companies which are getting lower ratings are risky in nature. As a result, at the time of the computation of nominal yield, the company’s riskiness plays a very vital role. The higher the risk lower is the credit rating, and thus the higher the need for Nominal Yield. A higher Yield offer is to compensate for the riskiness of the investment.

Is Nominal Yield the Same as the Annual Rate of Return (ARR)?

The nominal Yield does not show the actual return earned by the bondholder. Calculation of the coupon rate considers the bond’s par value, and thus it completely ignores the discount or premium on bonds. At times, the issuance of bonds is on a discount or premium. In such a situation, the return on investment changes as well. If the bonds are in high demand, they command and trade at a premium and vice versa.

If the issuance of bonds is on premium, the Annual Rate of Return (ARR) will be lower than the nominal yield. In contrast to this, if the issuance of bonds is on discount, the Annual Rate of Return (ARR) will be higher than the nominal rate.

Thus the ARR would be equal to the nominal rate only if the issuance of bonds is at par value or face value.

Let’s understand this with an example:-

| Price of Bond | Annual Interest | Yield | Annual Rate of Return |

| 1000 | 50 | 5% | 5% |

| 1050 (Premium of 50) | 50 | 5% | 4.76% (50/1050) |

| 950 (Discount of 50) | 50 | 5% | 5.26% (50/950) |

Nominal Yield Spread

The measure shows the gap in the yields of Treasury Bonds (Government Bonds) and Non-Treasury Bonds (Corporate Bonds) of the same maturity dates. This Spread is useful in assessing the yield expectation from government and non-government entities within a given timeline.

For Example:-

The yield of Treasury Bonds: 7%

The yield of Non-Treasury Bonds: 9%

Nominal Yield Spread = 9% – 7% = 2%

Limitation of Nominal Yield

One of the Nominal rate’s biggest limitations is that it completely ignores market fluctuations in the prices of bonds. Considering only face value for computation is misleading. Therefore, the use of this indicator in isolation is not preferable. The actual return could vary from the coupon rate given. Thus Nominal Yield is not a foolproof matrix for calculating actual return as it ignores the current market value of the security.

Thus there exists an inverse relationship between interest rates and the prices of bonds. If there is an upward revision in the interest rate in the economy, then the prices of existing issued bonds decrease. This intends to compensate the new buyer of those bonds for having a higher effective yield though the nominal rate is low. Similar will be the situation if there is a decreasing trend of interest rate in the economy. And the bond prices will start increasing, and the existing investors will get a capital appreciation on the investment. Thus consideration of Market prices for calculating the actual rate of return is of immense importance.

Why Issuances of Bonds Occur?

Bonds are fixed-income securities and are often issued by organizations and the government. Central or State government issues bonds to gather resources/funds for their enhanced public expenditure programs. The funds so arranged and accumulated are put to use for providing better services to citizens.

On the other hand, companies also raise funds by issuing bonds to the public at large. The companies use these funds to augment their Research and Development (R & D) capacity or to finance their capital expenditures. Thus Bonds are the best-preferred choice when it comes to raising funds with the help of fixed-income security.

Conclusion

Nominal Yield is the first thing looked up by investors before investing. Though it doesn’t give an actual return, it still is best used for assessing Bonds. Moreover, it always remains a reference rate. Investors should not consider Nominal Yield in isolation. They should evaluate this reference rate together with Spread and ARR. It also helps compare government and non-government fixed securities returns and fixation of the nominal rate while issuing bonds or any other security. Since the coupon rate calculation depends on credit risk and inflation rate, it overcomes the limitation of both – currency value or purchase price reduction and the investment risk. Thus it is best to use this matrix with other types of Bonds yield.