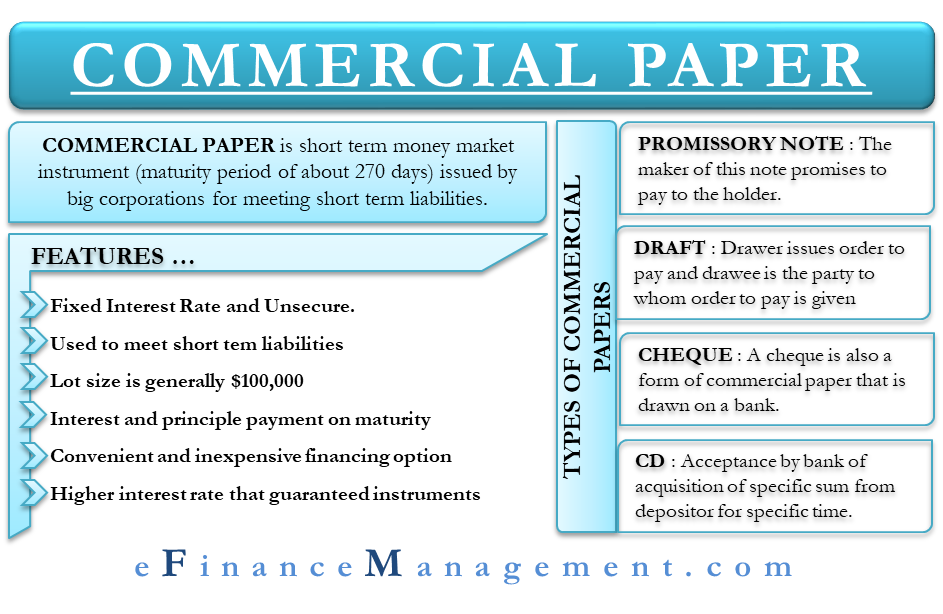

Commercial paper is a money market instrument with a maturity period of about 270 days. It is a standard short-term instrument, and big corporations usually issue it. These corporations primarily issue commercial papers to meet their short-term liabilities, such as accounts payable and inventories. Corporations issue commercial papers at a discount from the face value, and the discount depends on prevailing interest rates and the reputation of the issuer.

One distinguishing feature of commercial paper is that it is beneficial when dealing with a more substantial sum of money and does not require the use of cash. Since any collateral does not back this negotiable instrument, we can call it as an unsecured debt. Such features make it a convenient and cheap financing option for corporate with a good credit rating. On the other hand, wealthy individuals, financial institutions, big corporations, and money market funds buy these papers.

History of Commercial Paper

Article 3 of the Uniform and Commercial Code, applicable to all 50 states, governs commercial paper, the Virgin Islands, and the District of Columbia. The instrument first came into use about 100 years back. At the time, the New York businesses sold their short-term obligations to the dealers. The dealers, who purchase these obligations at a price less than their face value, would transfer them to a bank or any other investor. On maturity, the borrower would pay the investor the par value of the note.

The first dealer to deal in the commercial paper was Marcus Goldman of Goldman Sachs. After the end of the Civil War, Goldman Sachs was the biggest dealer in this financial instrument. After World War II, commercial papers became the most popular debt instrument in the money market.

Also Read: Euro Commercial Paper

Features

- They are unsecured and offer a fixed rate of interest.

- Usually, big corporations issue it to meet their short-term financial obligations, such as a new project or working capital needs.

- These instruments are usually in a lot of $100,000. Its size mostly makes them out of the reach of retail investors.

- The issuing entity promises to pay interest and principal at maturity.

- Not a viable tool for long-term obligations as there are better tools available for that purpose.

- It is a more convenient and inexpensive financing option than applying for a business loan. SEC does not make it mandatory to register the money market instruments.

- The majority of commercial papers have a maturity of one to six months.

- Investors get a higher interest rate than they get from any guaranteed instruments.

- FDIC does not take a guarantee for its payment. These instruments rely entirely on the reputation of the issuer, similar to any corporate bond or debenture.

- Rating agencies, such as Standard &Poor’s and Moody’s, rate them like any other corporate bond. Commercial papers with lower ratings offer a comparatively higher interest rate.

- Only investment-grade companies can deal in it. This means there is no junk market for such a money market instrument.

Types of Commercial Paper

As per the Uniform Commercial Code, there are four major types of Commercial Papers.

Promissory Notes

It is one of the most popular forms of commercial paper and is a written pledge to pay money. As per the promissory note, an individual, who is the maker of the note, promises to pay the holder. The payee could be anyone who has possession of the promissory note or a specific person named in the note. A note payable to the bearer is payable to anyone who presents it for remuneration and, therefore, is called a bearer paper.

A difference between a promissory note payable on demand and a time note is that the payee can redeem the former any time, while the latter has a specific date for payment. The time note will have the date on which day the holder is legally entitled to get the money. The issuer is under no obligation to pay the time note before the due date.

Draft

It is a three-party paper confirming the payment. In this case, the drawer issues the order to pay, whereas the drawee is the party to whom the order to pay is given. One of the most common examples of the draft is the cashier’s check. The draft (or the bill of exchange) is commonly used to safeguard payment in transactions involving shipping products overseas.

Buyers, who want to ensure the accuracy of goods before the payment goes for drafts, and sellers, on the other hand, might not want to rely solely on the buyer’s promise and would want to get the payment before delivery. Thus, in such a situation, sellers also prefer such notes.

Cheque

A cheque is also a form of commercial paper drawn on a bank. It is either payable on demand to a person specified or the holder. Since the individual or business has money in their bank account, the bank is under obligation for the amount in the account. Thus, it promises to make payments against cheques on accounts that have the needed money.

Certificate of Deposit

A certificate of deposit or CD is an acceptance by the bank of the acquisition of a specific sum of money from a depositor for a specific time. The bank promises to repay the amount with interest after maturity. In the case of CD, the bank is a maker and the drawee, while the person making the deposit is the payee.

Commercial Paper Trading

Usually, institutional investors, such as hedge funds, big financial companies, and more, sell commercial papers. Though small retail investors can also participate, there are a lot of restrictions, and they will need massive capital as well. On the other hand, a typical investor can also invest in the instrument via mutual funds, exchange-traded funds (ETFs), etc.

Final Words

Commercial papers are a common instrument in the money market, and their popularity arises from the fact that they are negotiable. It means one can transfer these papers freely to another party, either through endorsement or delivery. Also, it does not create any lien on the asset of the company. And the fact that they are tradable offers investors with an easy exit option. However, they require substantial capital investment and are not FDIC-insure as well. So, investors must keep these points in mind before considering investing in a commercial paper.

The content is very informative and simple. Every part is explained beautifully can you add some calculating examples along with content it will help to understand the business in the real world.