Before we understand the Capital Expenditure Budget, let’s first try to clarify what the term Capital Expenditure stands for.

What is Capital Expenditure?

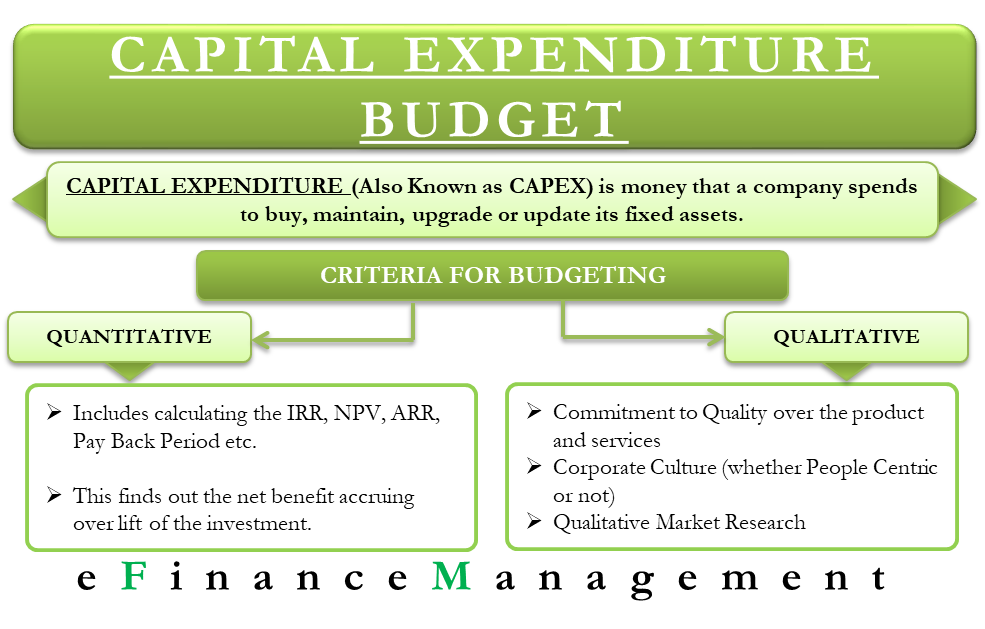

Capital Expenditure is the money that a company spends to buy, maintain, upgrade or update its fixed assets. The fixed assets of a firm include its land, buildings, vehicles, machinery, etc. Capital expenditure help create profits for a period that is longer than the current year. This distinguishes them from operating expenses since, in operating expenses, the expenses provide benefits only in the current year. E.g. for a firm that manufactures shoes, the expenditure incurred to purchase a piece of machinery that will cut the soles of the shoes is a capital expenditure. It is so because the machinery will give benefits for more time than the current year. At the same time, the expenditure incurred to pay the electricity bill is an operating expense since it won’t provide benefits beyond the current year.

Capital Expenditure Budget

Firms must budget for their capital expenditure simply because they don’t have unlimited funds. Every firm has limited funds. The goal of a firm is to use these limited funds to give it maximum benefits. So, firms take steps to ensure that it makes only those investments that are in line with the strategic requirements of the company. For this purpose, a firm uses several qualitative and quantitative decision criteria. A capital expenditure budget is a type of financial budget.

Quantitative Investment Criteria

Quantitative investment criteria may include calculating the Internal Rate of Return (IRR), Net Present Value (NPV) of the asset or investment, Payback Period (PB) of the investment, Accounting Rate of Return on investment (ARR), etc. All of which are discussed in a separate article on this website. These measures try to find out the net benefit which will accrue to the firm over the life of the investment.

Qualitative Investment Criteria

Commitment to Quality

This includes a firm’s commitment to the quality of the product or service it sells. So, suppose the firm has a high commitment toward the quality of the product. In that case, it may make an investment that enhances the quality of the product, which positively affects the customer’s perception of the company, etc. E.g., if a firm has a high commitment towards quality, it may make an investment in the customer care department which allows it to answer the phone calls in less than 30 seconds.

Also Read: Importance of Capital Budgeting

Corporate Culture

Another criterion includes the corporate culture of the firm. E.g., not every firm in the US will provide its employees with a very comfortable working environment like the ones at Google. If the corporate culture of a firm, e.g., is people-centric, it may make an investment that it believes will positively impact the morale of the employees. So, the firm may provide employees with bean bags in the office. Or buy a health insurance cover for them or some other investment that is consistent with the corporate culture.

Qualitative Market Research

Another criterion will be to first ask the customer what they want and then decide what investment the firm can make to fulfill those needs. It is always a better idea to ask the customers what problems they are facing than guessing about those problems from the comfort of your office room. If you approach existing happy customers, they happily share their genuine feedback in most cases. Analysis of such feedback helps in coming out with a list of improvements a product needs. Since the customer is the king, qualitative factors that matter to a customer are most valuable.

Budgeting for Capital Expenditures

The capital expenditure budget of a firm identifies the amount of money that the company will invest in long-term projects and fixed assets. Budgeting for capital expenditure also involves making a choice regarding whether to purchase the equipment using the existing cash balance or to take debt for the same. If the company doesn’t have enough money, saving for a future purchase will delay the benefits which the asset can provide in the current period. However, taking a debt will come at a cost in the form of interest payments.

Alternative to Capital Expenditure

Suppose the managers of a firm sit down to prepare the capital expenditure budget of the firm and realize that they have a much larger need for investment than they can afford. These situations are common to new firms which enter into a new business that demands massive investment in capital assets. So, what can the firm do then? In these cases, the firm also has the option of taking the assets that it requires on a lease, thereby avoiding the huge lump sum payment. There are many different ways of leasing equipment. E.g., taking an asset on the operating lease will convert the capital expenditure of the firm into an operating one. In this case, the firm will only need to make annual lease payments to the owner of the asset. These lease payments will show in the income statement as operating expenses.

Beautiful. Well captured!!