What is a Line of Credit?

A Line of Credit (LoC) is a kind of revolving credit or an open-ended loan. It is an arrangement by a financial institution, typically a bank, whereby a particular loan amount is sanctioned to the account of the borrower. The latter withdraws the balance as and when required. However, the beauty of this mechanism is that the interest is chargeable only on the amount actually used. The borrower can use the money whenever they want, as long as the withdrawal is within the maximum limit.

Such a loan facility works like a credit card. The borrower can use the LoC money whenever they want but need to pay it back on an ongoing basis to ensure the maximum limit is not breached. Though LoCs have a maximum limit, they do not have any expiration date. There are two kinds of LoCs – secured and unsecured. To understand the relevance and uses of both, we must be aware of the differences between Secured vs Unsecured Line of Credit.

Before we detail the differences between Secured vs Unsecured Line of Credit, it is imperative that you know what the two mean.

Secured vs Unsecured Line of Credit – Meaning

A secured line of credit uses collateral to secure the loan. This means that if the borrower fails to repay the loan, then the lender can take away the collateral. Or, the lender can legally sell the collateral to get back the loan amount. So, a secured line of credit is less risky for the lenders. And because of this security availability, they are able to offer better interest rates and other loan terms to the borrowers.

An unsecured line of credit does not involve any collateral. This implies that lenders are at more risk and have fewer options to recover the loan amount if the borrower defaults. Credit cards are a good example of an unsecured line of credit. Open overdraft is another example of such an unsecured line of credit.

Also Read: Differences between Loan and Line of Credit

Now that we have an idea of what the two terms mean let us take a look at the differences between Secured vs Unsecured Line of Credit.

Secured vs Unsecured Line of Credit – Differences

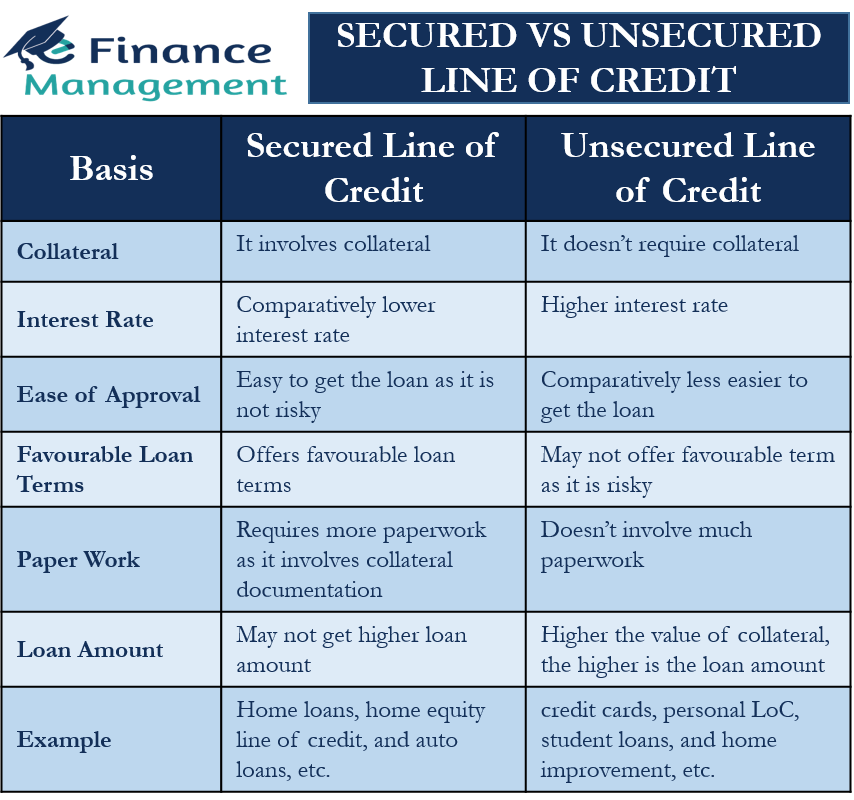

Collateral

Collateral is the primary difference between the two, and all other differences only stem from this primary difference. The secured line of credit involves collateral, but in an unsecured line of credit, the borrower is not required to give any collateral.

Interest Rate

Since secured LoC are low risk for the lender because of the use of collateral, these loans carry comparatively lower interest rates. On the other hand, unsecured LoC is riskier and thus, carries a higher interest rate.

Ease of Approval

It is easier to get a secured LoC than an unsecured LoC. This is because the lender will not hesitate to grant the LoC if the borrower is putting any collateral.

Also Read: Letter of Credit Vs. Line of Credit

Favorable Loan Terms

Secured LoC offers borrowers more favorable loan terms, such as longer repayment periods. In contrast, a lender may not be able to offer favorable loan terms on an unsecured LoC because it is riskier.

Paper Work

Secured LoC requires more paperwork as it involves collateral documentation as well. So, the approval process could take some time. On the other hand, the approval process for unsecured loans does not include much paperwork. Still, the process could take some time because the lender needs to verify the creditworthiness of the borrower.

Loan Amount

A borrower may be able to get a higher loan amount in a secured LoC. This is because the higher the value of collateral, the higher the loan amount. Whereas, in unsecured LoC, the amount is usually less.

Example

Home loans, home equity line of credit, and auto loans are some of the most popular types of secured LoC.

On the other hand, credit cards, personal LoC, student loans, and home improvement loans are examples of unsecured lines of credit.

Secured Vs Unsecured which is a Better Option?

On the basis of the points discussed above, one can easily conclude that a secured LoC is better than an unsecured one for both lenders and borrowers. This is because the former offers better loan terms, less interest rates, higher borrowing limits, and other benefits to the borrower. Like the lender, a secured LoC is a less risky option; thus, they get peace of mind that, in any case, they would get their money back.

However, even though a secured line of credit is better, it may not suit all the borrowers. Those who do not have any collateral to offer will have to take up an unsecured LoC. Also, those with high creditworthiness may also go for an unsecured LoC. Such borrowers will be able to get favorable terms in an unsecured LoC as well.

On the other hand, a secured LoC is good for those with assets like a home or car. However, they should be confident in paying back the loan because or else, if they fail, they may lose their collateral.

More importantly, whether you go for a secured or unsecured LoC depends largely on why you need the money. For instance, if you want money for everyday purchases, then an unsecured LoC, such as a credit card, would be more logical. On the other hand, if you want a larger amount of loan, then a secured LoC is a better option.