Overdraft (OD) and cash credit are widely used external sources of finance to avail short-term borrowing. Businesses use both cash credit and overdraft to manage short-term working capital requirements. The difference between bank overdraft and cash credit is on various aspects, which include the nature of the account, charges, and fees, amount, purpose, type of security, use of funds, interest rate, etc. Let us see in detail the difference between overdraft and cash credit.

Both these facilities are repayable on demand and classified as sources of finance/loans payable on demand. However, businesses rarely recall these facilities in real-life scenarios except in circumstances like a customer’s business and financial position going from bad to worse phase as time passes by. Or, in a case when the value of the security is extremely low during a period of revaluation of the security or during the renewal of the facility.

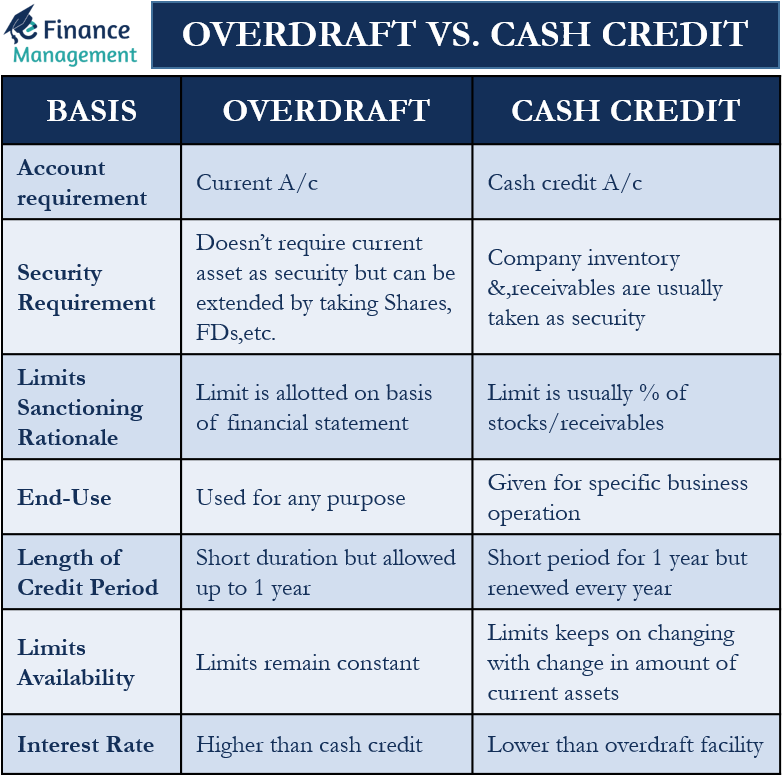

Although both these facilities are very similar in nature, one needs to understand the difference between overdraft and cash credit to understand which one to avail of.

Difference between Overdraft and Cash Credit

| Overdraft | Cash Credit | |

Meaning |

The overdraft facility allows the withdrawal of excess amounts in case of insufficient bank balance. | Cash credit is a short-term loan to finance working capital requirements. |

Type of Bank Account |

It is a facility of “excess withdrawal” given in the current account and, at times, even in the savings account. | One needs to usually open a separate cash credit account with a bank to avail cash credit facility. |

Security Requirement |

An overdraft facility does not necessarily require current assets as security. One can extend this facility by taking shares, other investments like FDs, and insurance policies as security. | Usually, the inventory and receivables of a business work as security for allowing a cash credit facility. |

Limits Sanctioning Rationale |

The rationale behind allowing a limit is usually the assets under consideration for collateral and also the financial statements of the company. At times, an overdraft limit may get approval even on the basis of the person’s credibility. | The limit in the case of a cash credit facility is usually a percentage of the stocks or receivables. |

Purpose |

The purpose of using the overdraft facility is not necessarily business. | Cash credit is specifically for business operations (as working capital). |

Length of Credit Period |

The duration of the overdraft facility is very short at times (say a month or even a week in some cases) but may extend for up to 1 year. | Cash Credit is usually for a short period. The limit allowed is for a period of 1 year and is renewed every year. In some cases, renewals or reviews may be stipulated half-yearly as well. |

Limit of Withdrawal |

The amount of the overdraft limit that the customer gets remains constant since the limits sanctioned are not based on current assets. However, if OD is against shares or insurance policy surrender value, the limit changes at periodic intervals based on the underlying security value. | The cash credit withdrawal limit keeps changing with the change in the amount of current assets kept as security. The withdrawal limit from the CC facility is called drawing power. |

Rate of Interest |

The interest rate on the overdraft facility is usually higher than the interest rate on the cash credit facility. | The interest rate on the cash credit facility is lower than what it is usually on the overdraft facility. |

Interest Calculation |

The interest is calculated on the amount overdrawn | The interest is calculated on the total amount of the credit allowed. |

Also, refer to Overdraft Vs. Loan

A GOOD INFORMATION SHARING

continuously I used to read smaller content that also clears their motive, and that is also happening with this paragraph which I am reading at this time.