Company debenture is one of the important sources of finance for large companies, in addition to equity stocks, bank loans, and bonds. Companies need to follow certain procedures for the issue of debentures to raise money. There are several ways of issuing a debenture, viz. at par, premium, or discount, and even for consideration other than cash.

Issue of Debentures

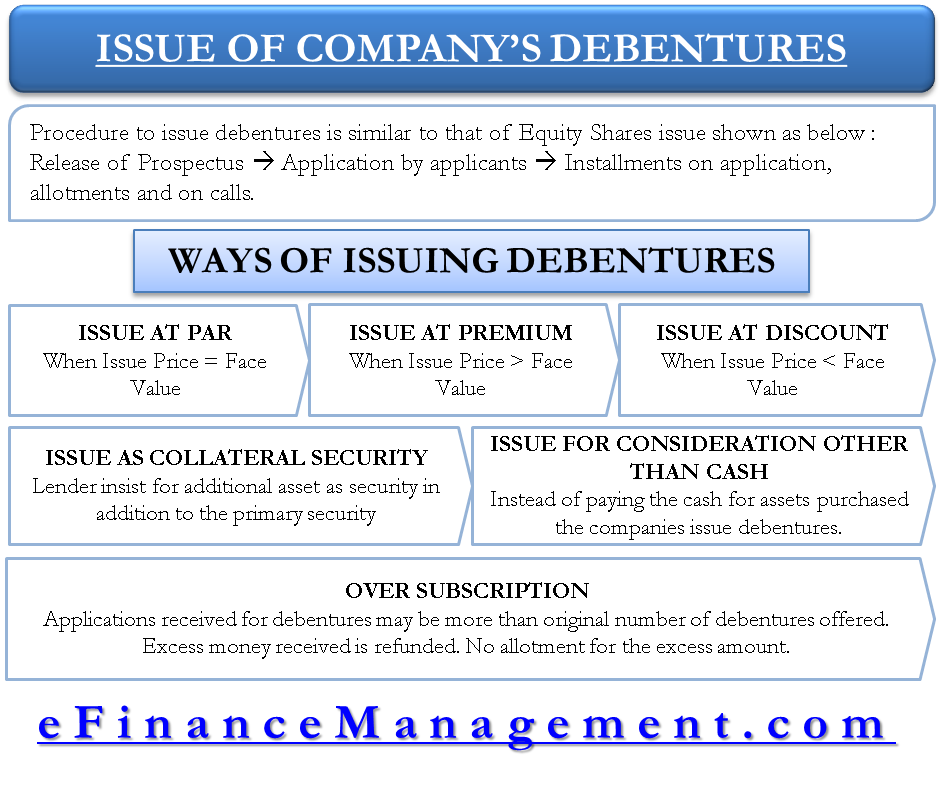

The procedure of issuing debentures by a company is similar to the one followed while issuing equity stocks. The company starts by releasing a prospectus declaring the debenture issuance. The interested investors then apply for the same. The company may need the entire amount while applying for the debentures or may ask for installments to be paid while submitting the application, on allotment of debentures, or on various calls by the company. As explained below, the company can issue debentures at par, at a premium, or at a discount.

Different Ways for Issuing of Debenture

Once the company invites the applications and the investors apply for the debentures. The company can issue debentures in one of the following ways:

Issue of Debenture at Par

When the issue price of the debenture is equal to its face value, the debenture is said to be issued at par. When a debenture is issued at par, the long-term borrowings in the liabilities section of the balance sheet equals the cash in the assets side of the balance sheet. Thus, no further adjustment is required to balance the company’s assets and liabilities. The company can collect the whole amount in one installment, i.e., on an application, or in two installments, i.e., on an application and subsequent allotment. However, there might be a scenario in which money is collected in more than two installments, i.e., on an application, on an allotment, and at various calls by the company.

Issue of Debenture at Discount

The debenture is said to be issued at a discount when the issue price is below its nominal value. Let us take an example – a Rs. 100 debenture is issued at Rs. 90, then Rs.10 is the discount amount. In such a scenario, the balance sheet’s liabilities and assets sides do not match. Thus, the discount on debentures’ issuance is noted as a capital loss and is charged to the ‘Securities Premium Account’ and is reflected as an asset. The discount can be written off later.

Also Read: Debentures in Accounting

Issue of Debenture at Premium

When the price of the debenture is more than its nominal value, it is said to be issued at a premium. For example, a Rs. 100 debenture is issued for Rs.105, and Rs.5 is the premium amount. Again, assets and liabilities do not match in such a situation. Therefore, the premium amount is credited to Securities Premium Account. And is reflected under ‘Reserves and Surpluses’ on the liabilities side of the balance sheet.

Issue of Debenture as Collateral

The debentures can be issued as collateral security to the lenders. This happens when the lenders insist on additional assets as security in addition to the primary security. The additional assets may be used if the complete amount of the loan cannot be realized from the sale of the primary security. Therefore, the companies tend to issue debentures to the lenders in addition to some other physical assets already pledged. The lenders may redeem or sell the debentures on the open market if the primary assets do not pay for the complete loan.

Issue of Debenture for Consideration Other Than Cash

Debentures can also be issued for consideration other than cash. Generally, companies follow this route with their vendors. So, instead of paying the cash for the assets purchased from the vendor, the companies issue debentures for consideration other than cash. In this case, also, the debentures can be issued at par, premium, or discount and are accounted for in a similar fashion.

Over Subscription

The company invites investors to subscribe to its debenture issue. However, it may happen that the applications received for the debentures may be more than the original number of debentures offered. This scenario is referred to as oversubscription. In the case of over-subscription, a company cannot allocate more debentures than it had originally planned to issue. So, the company refunds the money to the applicants to whom debentures are not allotted. However, the excess money received from allocated debentures applicants is not refunded. The same money is used towards allotment adjustment and the subsequent calls to be made.

Also Read: Characteristics of Debenture

Conclusion

Several companies decide to issue debentures to raise capital and other long-term finance sources. The companies need to follow the regulations and the procedure associated with issuing debentures. Further, they also need to account for debentures issued at par, premium, or discount accordingly.

Read more about Debenture and its Basic Features.