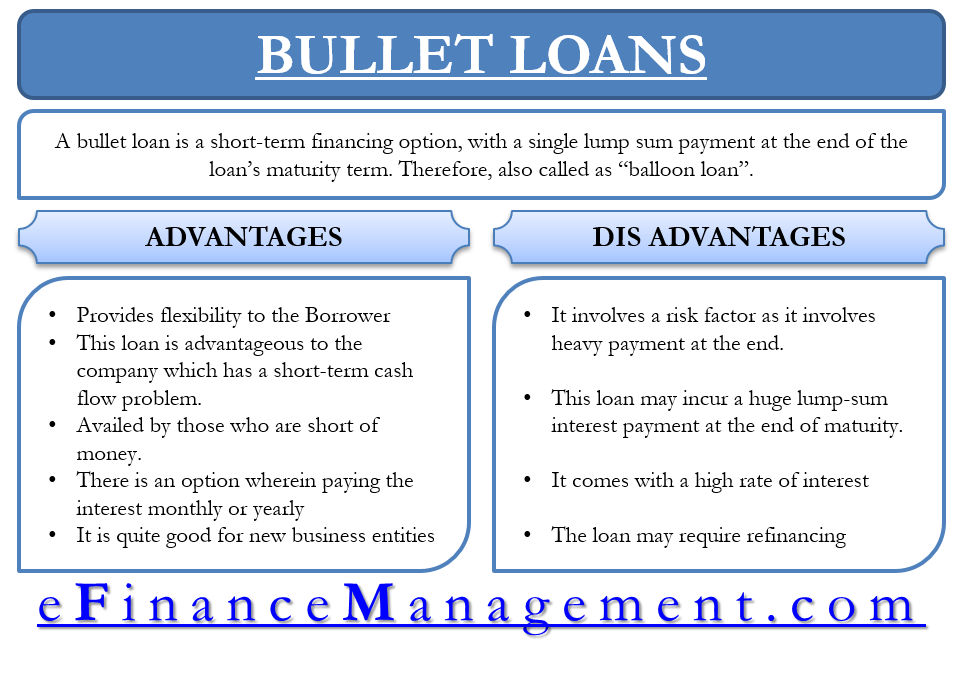

A bullet loan is a short-term financing option, with a single lump-sum payment at the end of the loan’s maturity term. Therefore, it is also called as “balloon loan.” All types of customers – especially the ones dealing with land contracts or real estate developments can avail of a bullet loan.

Bullet loans are classified as mortgages, notes, bonds, or other types of credit instruments. Further, a bullet loan has a fixed or floating rate of interest. Typically, it will charge a higher rate of interest when compared to standard loans.

How Does a Bullet Loan Work?

A borrower of the bullet loan is approved a maximum principal amount determined on the basis of repayment capability. The structure of the loan can be designed in different ways, depending upon the customer’s repayment attitude or payment conditions. The borrower can repay the loan in a single or regular interest payment mode. The regular payment mode is like monthly, annually, or yearly reducing the lump sum money at the maturity.

A lump-sum bullet loan includes accrual of interest as per the loan’s terms like monthly, annually, etc. It enables the borrower to make an entire payment on maturity. However, the borrower has the option to make regular interest payments and eventually reduce payoffs at the time of maturity.

Also Read: Balloon Payment

The latter is quite beneficial for the individual wherein the borrower expects a huge cash inflow, such as bonus or fixed returns. Apart from this, a periodic payment also lowers the financial burden at the time of repayment.

Example:

Suppose you take a loan of amount $1,900 and repay it back in a year at an interest of 10% annual compounding. In the case of a bullet loan, the person will pay $2,090 ($1,900 as principal plus $190 as interest) in a single payment mode.

Payment Types of Bullet Loans

In the US, the contract provisions that apply to the loan must state the payment of bullet loan to have “Truth-in-Lending.” The consumer should be informed of all charges, terms, and costs on the loan. This is the stipulation under this law.

This is done to make the borrower aware of his obligation as he may fall short of funds to repay the loan at maturity. A two-step payment plan is used here under which the borrower can avail of a reset option to reset the loan using current market rates and use amortizing payment mode. This option can be availed only if the borrower is still the owner with not less than 30 days late payment in the preceding 12 months and has no loans against the property.

Also Read: Types of Interest Rates

On the other side, in the plan without the reset option, there might be an expectation that either the borrower has sold the property or refinanced it by the end of the maturity. This clearly involves the existence of refinancing risk in this kind of bullet loan repayment.

Further, in the US, the Federal National Mortgage Association features such loan or mortgage payments based on a 30-year amortization.

Advantages of Bullet Loan

- Bullet loan provides flexibility to the borrower, especially the real-estate developers.

- The loan is advantageous for a company with a short-term cash flow problem.

- People who are short of money and expecting to receive money in the near term can avail it.

- Bullet loans come with an option wherein paying the interest monthly or yearly reduces the financial burden on the borrower at the time of repayment of the loan.

- The bullet loan is quite good for new business entities as it provides flexibility to borrow cash as and when needed.

Disadvantages of Bullet Loan

- The bullet loan involves a risk factor as it involves heavy payment at the end; the borrower may not have made preparations to repay the loan in one go.

- The loan may incur a huge lump-sum interest payment at the end of maturity

- A bullet loan comes with a high rate of interest.

- The loan may require refinancing, and the borrower may end up incurring more closing tasks.

Refinance By Selling

Further, people use bullet loans for buying a residential property and avoid high installments payments. However, it only works if the price of the property rises. At maturity, they can sell off the property that would be worth more or may refinance it.

On the contrary, if the property prices drop, this results in making borrowers suffer during the financial global crisis term. During this time, the borrowers could not sell the property due to lower prices but would have used the profit to meet the bullet loan payment.

Conclusion

Bullet loans are a useful tool for businesses in a short-term liquidity crunch, but banks require a high Loan-to-Value ratio. The value of the asset should cover the loan amount by a good margin. Loan-to-Value is defined as this. Usually, in a bullet loan, banks require 75% of the loan to be covered by the asset value. This is so they can sell it and get repaid in case of delays in payment.