Meaning of Compound Interest

Compound Interest is the most prevalent form of calculating interest on loans, deposits, and investments. It is a form of interest on the principal amount plus all the interest accumulated to date. In simple interest, the fixed interest gets calculated in every period on the principal amount. But in the case of compound interest, interest is added to the last principal amount for calculating interest for the current period. In other words, the interest amount for the current period will be added to the principal or base amount. This amount will become the principal amount for calculating interest for the next period. Hence, it is a form of reinvestment of interest with every passing period.

In the case of deposits with a bank or investments with a financial institution, the depositor benefits from a higher interest amount under compound interest. But the situation becomes vice-versa in the case of loans. Here, the borrower needs to pay interest on the principal amount and the interest accumulated so far. Thus he has to pay more than in the case of simple interest. Interest compounding can be even daily, monthly, yearly, or as decided at the time of the deposit or loan. Interest will be higher with a greater number of compounding periods and vice-versa.

Calculation

The formula for compound interest calculation is:

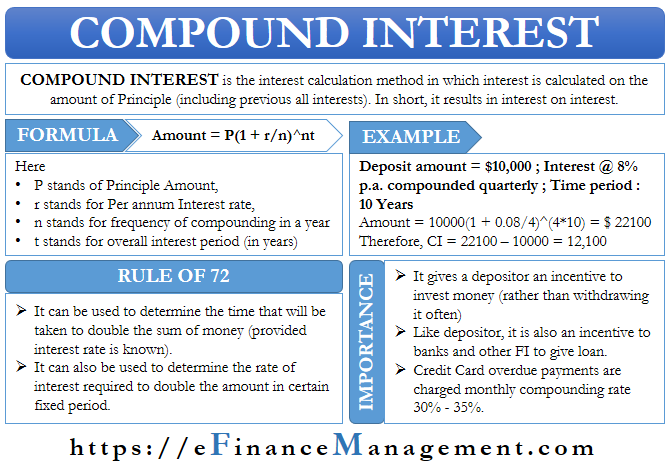

C.I.= P (1 + r/n)^nt

1) Compound interest needs to be calculated on the principal amount plus the interest which has accumulated so far.

2) “r” is the interest rate of the deposit or loan. The format for usage should be r/100. For example, if the interest rate is 8% p.a., we will use it as 8/100= .08 for calculation.

3) “n” is the compounding frequency for calculating interest. It is the number of times compounding interest will be compounded per year. If the compounding frequency is quarterly, n will be 12/3=4 in the formula.

4) “t” is the overall time for which interest calculation is to be done. It is usually in the yearly format. If compound interest calculation is required for five years, t will be 5 in the formula.

Example

Suppose a person deposits the US $10000 in a bank at an 8% rate of interest compounded quarterly. The period of the deposit is ten years. The amount he will receive after ten years will be:

10000 (1 + .08/4)^4×10

=10000 (1.02)^40

=10000 (2.21)

= US $ 22100

The Compound interest for the period is US $ 22100 – US $ 10000= US $ 12100.00

Continuing with the above example, suppose the compounding frequency is monthly instead of quarterly. The compound interest calculation will be as follows:

=10000(1 + .08/12)^12x 10

=10000(1.0067)^120

=10000x 2.23

=US $ 22300

In this case, the compound interest earned is US $ 22300 – US $10000= US $12300.00

Therefore, we see that even with the same number of years, the depositor receives the US $ 200 extra with a change in the compounding period from quarterly to monthly. It is the power of compounding.

Rule of 72

The “rule of 72” is an exciting concept associated with Compound interest. It can be used to determine the time it will take for a sum of money to double if we know the interest rate. Similarly, it can also be used to determine the rate of interest required for an amount of money to double in a fixed number of years. Therefore it helps to meet an individual’s investment goals.

Also Read: Types of Interest Rates

For calculation of compound interest using Rule of 72, you can use the Rule of 72 Calculator.

For example, suppose the current rate of interest offered by a bank on its savings deposits is five %p.a. If we have to determine the time it will take for the principal amount to double, we can calculate it. Simply we divide 72 by the current rate of interest.

=72/5 % p.a.

=14.4 years

Similarly, suppose individual plans to deposit the US $ 10000 and wants it to double in 10 years. The rate of interest required to make this possible is:

=72/10 years

= 7.2 % p.a.

Usage and Importance of Compound Interest

1) For a depositor, it gives him an incentive to keep his deposits intact and not withdraw them soon. Suppose he invests the US $ 100 in a bank at a 5% p.a. Rate of interest. His interest income for the first year will be 100 x .05x 1 = US $ 5. In case of simple interest, he will keep earning this same US $ 5 every year on his deposit. But in the case of compound interest, his interest income for the second year will be calculated by keeping the US $ 105 as principal. Thus his interest income will be= 105 x .05x 1= US $ 5.25.

It motivates a depositor to keep depositing more and more to earn higher interest and keep it with the bank for a longer duration.

2) Compound interest is widely used by banks and financial institutions while giving out loans. Like with deposits, it acts as an incentive for banks too to lend more and for a longer duration of time.

From the borrower’s point of view, it becomes essential to keep paying off interest as it accumulates so that he is not required to pay additional interest on the previous term’s interest amount too. Also, he should pay out more and more whenever possible to mitigate the impact of compounding.

3) Credit cards give a specified time for paying off interest-free dues. But once you miss the due date, these dues are charged with interest rates ranging from 30%-40% p.a., and that too on a monthly compounding basis. These dues spiral upwards at a speedy pace. Hence, it is preferable to pay off the due amount within the specified period.

Also, read Simple and Compound Interest.

Helpful