Meaning of Factoring

Factoring is a financial service used for raising funds in the business whereby the business entity sells all of its bills receivable to an outside agency at a discount. The outside agency is called a factor. In this post, we are going to discuss advanced and maturity factoring.

Types of Factoring

Various types of factoring arrangements are possible depending on the terms of the agreement between the factor and the business owner. Listed are the types of factoring arrangements:

- Recourse & non-recourse factoring

- Advance and maturity factoring

- Bank participation factoring

- Full factoring

- Domestic and cross-border factoring

- Suppliers guarantee factoring

- Disclosed and undisclosed factoring

This article focuses on the two types of factoring, i.e., advance factoring and maturity factoring.

Meaning of Advance Factoring

Advance factoring can be with or without recourse. Under advance factoring arrangement, money is paid by the factor to the business in advance. However, not the entire amount is paid in advance, but a certain percentage of the receivables is paid in advance. The balance amount is paid on the guaranteed payment date. The held back amount is the margin ranging from 5% to 25%, which is paid post realization of money from the customers. The factor collects the agreed rate of interest for advance payment made to the business considering the short-term rate, turnover, financial standing of the business, etc.

Maturity Factoring Meaning

Maturity factoring, also known as collection factoring, is a type of factoring service in which the client sells his invoice to the factor. In return, the factor pays the client for such invoices either on the date of maturity or any date after the date of maturity. In this factoring arrangement, the factor does not pay the client any money in advance. For example, an invoice maturing on 25th August 2016 shall be either paid off on 25th August 2016 or any other date after maturity is decided between the client and the factor.

Also Read: Types of Invoice / Receivable Factoring

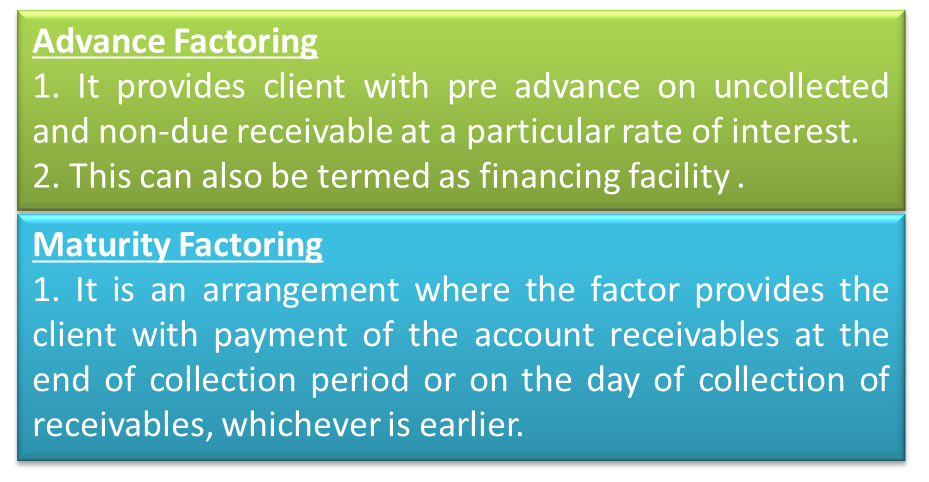

Difference between Advance and Maturity Factoring

Under advance factoring, the factor provides the client with pre-advance on uncollected and non-due receivable at a particular rate of interest. This can also be termed a financing facility. On the other hand, maturity factoring is an arrangement where the factor provides the client with payment of the account receivables at the end of the collection period or on the day of collection of receivables, whichever is earlier.

Conclusion

Factoring is an important aspect for any business that wants to remain focused on its main business activities rather than spending its energies on collecting payments from its debtors. Advance factoring and maturity factoring are two types of factoring services that the business may opt for depending on its suitability. Both factoring services serve the business with money for their invoices. If the business needs money for the invoice immediately, then it may opt for advance factoring. And if there is no immediate requirement of cash for invoices, then the business may opt for maturity factoring.

I think that it is very important that we understand factoring first before we use it for our business. This article is very knowledgeable. Thanks for sharing this article. This is very useful and helpful for me to understand factoring.

I am new to factoring. This article is really helpful. This definitely help me to understand factoring well. I think that this article will definitely help me to avoid problems regarding factoring.

Factoring is a sustainable of using your own assets -invoices- to finance your cash flow without having to borrow money from banks. You keep control of your finances and you grow with your own resources. Never tied up to the bank covenants the potential for growth is linked to your ability to produce and sell. In a sense is like working COD.