What do we Mean by Interest Rate Parity?

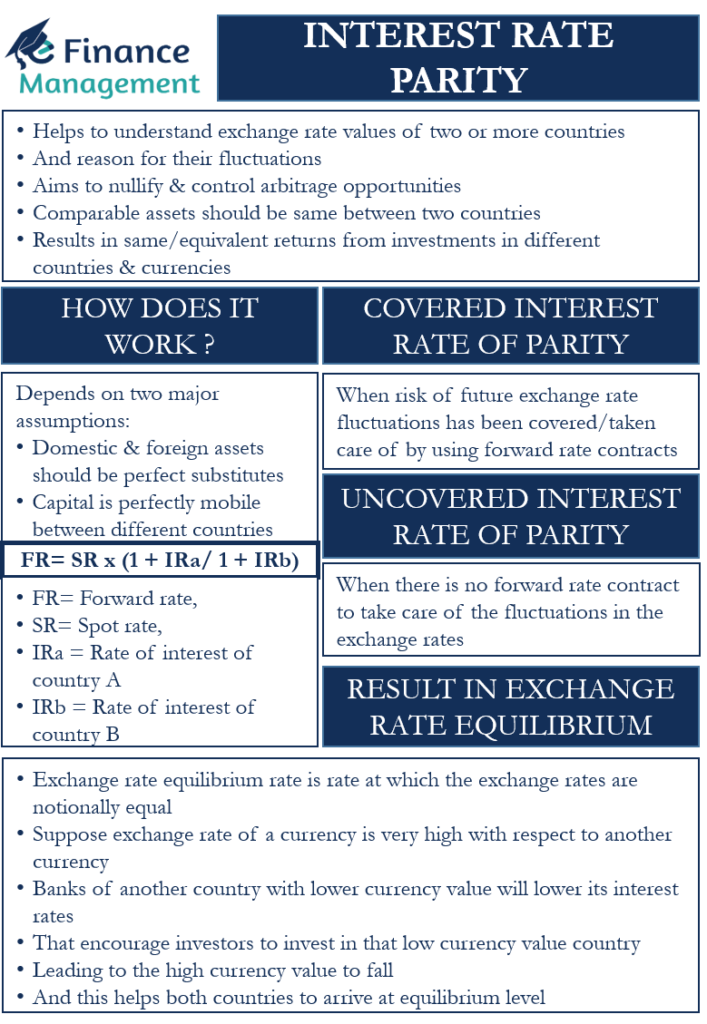

The theory of Interest rate parity is very significant in the field of international finance. It helps us to understand the exchange rate values of two or more countries and the reason for their fluctuations. A myriad of international investments takes place daily through the exchange of international currency with the motive of profiting from differences in exchange rates. Even a minor discrepancy in the spot exchange rate and the forward exchange rate can result in arbitrage opportunities, helping investors make quick and risk-free profits. Interest rate parity theory aims to nullify and control such arbitrage opportunities. According to this theory, the rates of return on two or more similar assets or the assets that are comparable should be the same between two countries.

The theory of Interest rate parity suggests that the rate of return on a deposit should be equal for all investors, irrespective of their choice of currency. There should be no arbitrage opportunities by investing in one currency and withdrawing and liquidating the investment in some other currency. Therefore, if an investor decides to invest in a bond in US dollars, he should get the same returns even if he converts the dollars into UK pounds first and then invests it in the same bond. The interest rates and the forward currency rates are inter-connected—the theory results in the same or equivalent returns from investments in different countries and currencies.

How does the Theory of Interest Rate Parity Work?

Interest rate parity depends upon the following major assumptions.

- Assets are Perfect Substitutes: The first assumption is that the domestic and foreign assets should be perfect substitutes for each other. In case an asset is not a perfect substitute, an investor may be willing to pay more for the superior asset, whatever the interest rate may be. Hence, the theory will not hold good.

- Capital Mobility: The second assumption states that capital is perfectly mobile between different countries. There are no charges associated with it. And there are no restrictions by various countries for its movements across.

- Arbitrage Opportunity: There are no arbitrage opportunities available.

- And the fourth is that the foreign exchange markets across the globe are in equilibrium.

An investor can earn arbitrage profits by a difference in the returns from domestic assets and returns from foreign assets. Also, an investor may try to borrow in a country with low rates of interest. He will then exchange the money for a foreign currency and invest it in a country with a higher interest rate. The investor can look at making arbitrage profits when he converts this investment back into his domestic currency at the time of maturity. Thus, the interest rate parity theory attempts to eradicate all possible arbitrage opportunities and scenarios.

Formula and Example

The formula for IRP is as follows:

FR= SR x (1 + IRa/ 1 + IRb)

Here, FR= Forward rate, SR= Spot rate, IRa= Rate of interest of country A, and IRb= Rate of interest of country B.

Let us understand the above formula with the help of an example. The present spot rate of exchange for a British pound to a US Dollar is 0.80:1. This means that for every 100$, we can get 80 pounds and vice-versa. Suppose the rate of interest in the UK is 4% at present. Hence, if we invest 80 pounds in a year, we can earn an interest of 3.2 pounds in a year, totaling 83.2 pounds.

Now suppose an investor in the US decides to invest his money in his country. He will later convert it into UK pounds at maturity. The current rate of interest in the US is 6%. We can calculate the forward exchange rate ratio with the help of the difference in the rates of interest as follows:

FR= [0.8 x(1+ .04)] / [ 1 x (1+.06)]

=(0.8 x 1.04)/ (1 x 1.06)= 0.785

The investor invests US$ 100 in his country at the present interest rate of 6%. The initial sum of US$100 will become $106 at the end of the year. Now he converts this sum into British pounds at the forward exchange rate of 0.785.

$106 x 0.785= 83.2 pounds

Therefore, we see that the end result of the investment is the same in both cases. Even if the investor had converted US$ 100 into British pounds at the spot exchange rate initially. He would have still ended up with 83.2 pounds only at the end of the year.

Hence, the interest rate parity theory makes sure that investors are not able to make undue profits by playing with the difference in interest and exchange rates between countries.

What is Covered and Uncovered Interest Rate Parity?

Covered Interest rate parity is a situation when the risk of future exchange rate fluctuations has been “covered” or taken care of by using forward rate contracts. The forward contract keeps the exchange rates in equilibrium. Thus, the investor becomes indifferent while choosing between investing in his own country’s interest rate and a foreign country’s interest rate. And the difference in the exchange and interest rate does not entice the investor as he is not supposed to earn anything extra.

On the other hand, uncovered Interest rate parity is a situation when there are no forward rate contracts to take care of the fluctuations in the exchange rates. The expectation of the spot rates only determines the parity in the interest rates. This means that the future rates have not been fixed or locked. However, there is not much difference between the spot rate and expected forward rate, making the two types of the theory- covered and uncovered, almost similar.

How does the Interest Rate Parity Theory Result in Exchange Rate Equilibrium?

The exchange rate equilibrium rate is the rate at which the exchange rates are notionally equal, and the theory of Interest rate parity holds or is valid. Suppose the exchange rate of a currency is very high with respect to another currency. Let the first currency be the British pound and the second currency be the US dollar. Thus, the value of the British pound is very high with regard to the US$. The condition of Interest rate parity is not met. The Central Bank will lower the interest rates. This will prevent the value of the pound from rising further.

This will mean that investors will earn higher returns on their investment in the US when they invest in US$. The residents of the US will not seek investment opportunities abroad and invest in their own country. Even the British will move their investment to the US to earn higher returns.

The demand for US$ will go up, and the British pound will start falling. Thus, the value of the pound will start falling, and the value of the US$ will start rising. Eventually, the exchange rates will come back to the equilibrium point. The Forex market will become stable, the exchange rates will stabilize, and the IRP will again be achieved.

Opposite Situation

The exact opposite will occur in case the value of the British pound is low, and that of the US$ is high. The rates of return on the British deposits will be much higher than the US deposits. This will result in an increase in demand for British pounds. The demand for the US$ will fall. Thus, the value of the pound will rise. The value of the US$ will fall until the exchange rates achieve an equilibrium. Again the Forex market will stabilize, and IRP will hold.

Conclusion

Interest rate parity is fundamental in international trade and finance. It prevents the exploitation of interest and exchange rate variations between the countries. However, the theory is widely criticized too. Because such a scenario does not exactly prevail all the time. And there do exist arbitrage opportunities.

Investors such as big banks and financial institutions with deep pockets can easily create or discover arbitrage opportunities arising out of exchange rate fluctuations. They will pump in millions of dollars and end up earning quick and easy profits. Moreover, this profit will be without bearing any risk. No risk is actually a possible situation. Bonds issued by strong nations such as the U.S. Treasury bonds never default on their payments. Hence, such investments are free of any risk.

Interest rate parity ensures a level and fair playing ground for each and every participant and investor. It helps to achieve exchange rate equilibrium. Moreover, the theory is especially beneficial to small and medium investors who cannot engage in cross-border investments due to the availability of limited resources.