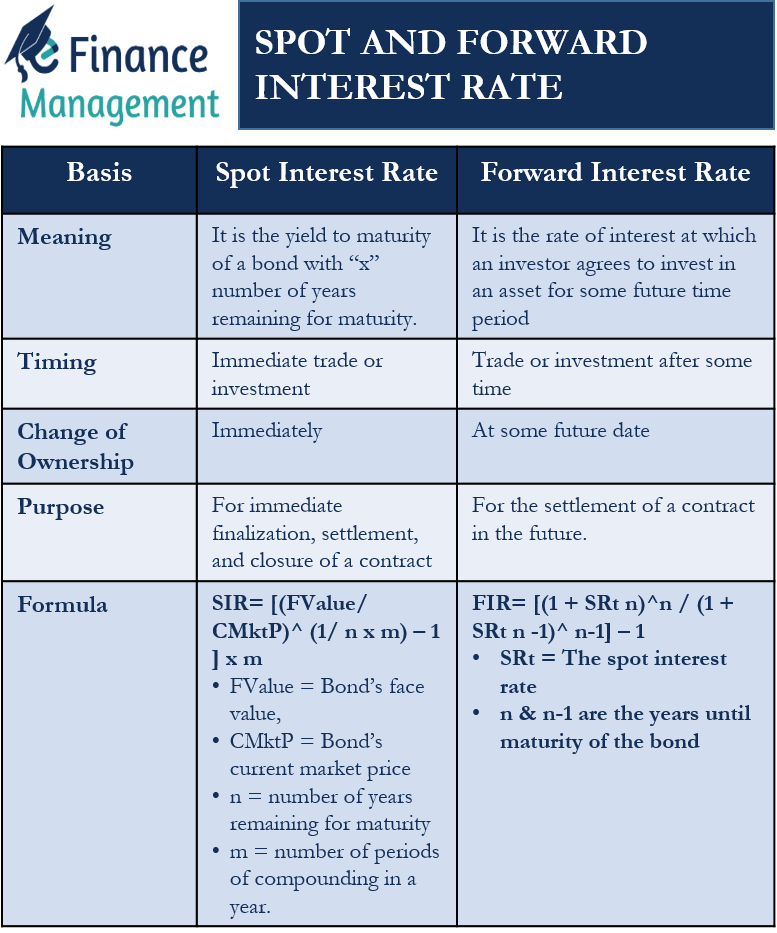

What do we Mean by Spot and Forward Interest Rates?

Spot interest rate is the yield to maturity of a bond with “x” number of years remaining for maturity. The bonds, in this case, are zero-coupon bonds. Such bonds do not make any coupon payment in their lifetime. In order to lure the investors, the issuer offers them a significant discount at the time of issue. But at the time of maturity, the bondholder gets the full face value of the bond. Forward interest rate is the rate of interest at which an investor agrees to invest in an asset for some future time period. He can also agree to borrow or lend money at the forward rate at some future point in time. Investors use the spot interest rates to calculate the forward interest rate on any asset. Both these spot and forward interest rates have a lot of differences.

The basis for the spot interest rate is the expectation of the possible future interest rates that should occur over the upcoming years until the maturity of that bond. Similarly, the forward interest rate is also based on expectations about interest rates and the performance of the markets. Therefore, the longer the time duration or the number of years until the maturity of a bond, the more unreliable and inaccurate these interest rates become. So there exists a similarity, too, as both these interest rates are based on the future interest rate scenario expectations.

What are the Main Differences between Spot and Forward Interest Rates?

There are a number of differences between the two types of interest rates. Some of them are:

Timing

Spot interest rate is of use to a buyer or a seller who wants to make an immediate trade or investment. It reflects the prevailing interest rate scenario in the economy.

Forward interest rate is of use to investors/traders who want to make a purchase or a sale after some time. However, they want to put a price tag on their purchase or sale and lock it in the present.

Also Read: Forward Interest Rate

Change of Ownership

In the case of a spot interest rate, the transfer of ownership of the underlying asset takes place immediately. The interest rate is for the spot or immediate settlement between the buyer and the seller.

In the case of the forward interest rate, the transfer of ownership of the underlying asset takes place at some future date. This date is decided at the time of the finalization of the contract. Only the interest rate is decided in the present. The actual delivery and payment of the asset take place at later pre-decided settlement date.

Purpose

Spot interest rate is of use for immediate finalization, settlement, and closure of a contract. It is the present rate for the bond and is generally not meant for speculative activities or for hedging risk.

But the forward interest rate is of use for the settlement of a contract in the future. It is a common tool for hedging risk by finalizing the interest rate for a transaction that will be completed at some future date. Also, traders and investors can use it as a speculative tool and exploit opportunities for arbitrage to earn out-of-the-way profits due to fluctuations in the interest rates.

Also Read: Spot Interest Rate

Calculation

Spot interest rate is the interest rate that we use to settle the present position in hand. Its calculation depends upon a number of factors such as the bond’s time until maturity, its face value and current market value, and the number of compounding periods in a year. We calculate the spot interest rate with the help of the following formula-

SIR= [(FValue/ CMktP)^ (1/ n x m) – 1 ] x m

Here, FValue = The bond’s face value, CMktP= The bond’s current market price, n= number of years remaining for maturity, and m = number of periods of compounding in a year.

Forward interest rate is primarily a factor of the spot rate. We use the spot interest rate and the time until maturity of the bond to calculate the Forward interest rate. The formula for the same is:

FIR= [(1 + SRt n)^n / (1 + SRt n -1)^ n-1] – 1

Here, SRt = The spot interest rate, n, and n-1 are the years until maturity of the bond.

Importance

Calculation of the implied spot interest rate can be done by using the forward interest rate. And similarly, we can calculate the forward interest rate from the spot interest rate. Because as we discussed earlier, both these have a common link and are derived ones. We can also use these interest rates to calculate the bond price.

However, the forward interest rate is technically the breakeven reinvestment rate. It is of use if an investor wants to choose between investments that offer a longer duration single maturity period or investment in two parts with two smaller duration maturity periods. This way, he can choose the best investment option that offers him higher profitability.

Graphical Presentation and Interpretation

Spot interest rates of bonds that have a similar credit rating but different maturity periods can be used to draw a spot curve.

In a similar fashion, we can draw a forward curve from forward interest rates. These rates should be for periods of equal lengths but at different points in time.

If two or more spot rates in consecutive periods show an upward trend, i.e., are getting higher, the forward curve will be above the spot curve. However, if the consecutive spot rates show a downward trend and are falling, the forward curve will be below the spot curve.

Two Hypothesis on Spot and Forward Interest Rates

Expectations Hypothesis

An investor can buy a bond for two or more years or choose an alternative investment strategy. He can sell the bond at the end of the first year and reinvest the proceedings in it again at the then-prevailing spot rate.

If the forward rate is the same as the expected spot rate at the end of the first year, the returns from any of the choices will be the same. But when there exists a difference between both these rates, the investor has an option, and he can make a better decision with this information. He can choose the better alternative between the two that maximizes his profits. And because of this, there exists an “expectations hypothesis.” According to it, the forward interest rate at the end of the first term or year should be equal to the then-prevailing spot interest rate. This situation will help create clarity and confidence in the investors’ minds. They can freely choose between bonds at the spot interest rate and forward interest rate without much difference in the expected profits/yields.

Liquidity Preference Hypothesis

According to the liquidity preference hypothesis, an investor will hold a bond as an investment for periods more than a year only if the forward rate is higher than the spot rate that the market expects at the end of the first year. Any risk-averse investor will sell off the bond at the end of the first year and repurchase it if the spot rate is higher at that point in time. Therefore, a higher forward rate than the spot rate will act as an incentive to investors to hold the more risky and longer-duration bonds.

Summary

Both types of interest rates are important to any investor/trader. They help him choose the best possible investment alternative that gives him maximum profits. However, if an investor wants to buy or sell a bond immediately, one will only have to do it at the spot rate. If one has time in his hands and is looking to hedge risk or earn speculative profits, one should look at the forward rate.