An annuity is essentially a series of cash flows at regular intervals during the life of the annuity. It is a cash inflow for recipients/investors/lending institutions. At the same time, it is cash outflow for the payer/borrower, etc. This cash flow could be either a payment or a receipt, such as an insurance premium, EMI loan, dividend, etc. These payments are made in predefined periods or intervals and can be made weekly, monthly, or yearly. Usually, payment is made in an annuity at the end of a period. However, in an annuity due, payment is made at the beginning of the period.

In other words, in an ordinary or regular annuity, the regular payment refers to the period before its date. However, in an annuity due, the payment refers to the period after its date. The primary difference between the ordinary annuity vs annuity due is that the payment is made in advance or after the due date.

Although these are two different concepts, the difference in the amount of two annuities (keeping all other things the same) is very small. Furthermore, the formula for the types of annuities is also very similar. However, it is important that everyone knows the difference between the ordinary annuity vs annuity due.

Ordinary Annuity vs Annuity Due – Differences

The differences between ordinary annuity vs annuity due are as follows:

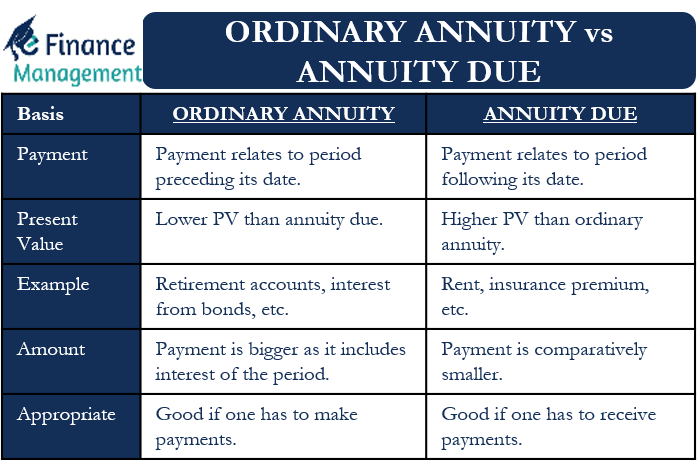

Payment

In an ordinary annuity, the payment you make is for the period preceding its date, whereas, in the payment in an annuity, due is for the period following its date.

Also Read: Present Value of Annuity

Present Value

We make the payment earlier in the annuity due, so its present value is usually higher than an ordinary annuity. This is due to the effect and principle of the present value of money and inflation. The PV in an ordinary annuity is comparatively lower as the payment has a time lag.

Read more about Present Value of Annuity

Formula

As mentioned above, there is a very small difference between the formulas of the two types of annuities. Basically, the difference we have to take into account in the formula is of one period. This is because, in one, the payment is at the beginning, and in another, it is at the end. So, the difference is one extra period.

If we want to calculate the future value of an annuity due, we first have to do the calculations in accordance with the ordinary annuity. Now, we have to consider the additional period, so we have to multiply the resulting number by an additional period, i.e. (1+i).

We need to make a similar adjustment when calculating the present value of an annuity due. First, we need to find the PV based on the formula for the ordinary annuity. Then, we need to make an adjustment for the one additional period. So, we need to divide the resulting number by the additional period, i.e., by 1 + i.

Also Read: Annuity Formula

Examples

The rent is a good example of an annuity due. Usually, you pay at the beginning of each month or in advance in a rent agreement. The insurance premium is also an example of the annuity due. We usually pay a premium for the insurance coverage during the entire period at the beginning of the period.

Retirement accounts are a good example of an ordinary annuity. Here you receive a fixed or variable amount at regular intervals and at the end of a period. A mortgage on a home is also an example of an ordinary annuity. Likewise, interest on bonds and stock dividends are an example of an ordinary annuity. The bond issuer usually pays twice a year, which is also at the end of the period.

Amount

In the case of an ordinary annuity, the payout is usually higher because it would include interest for that period. On the other hand, the payout may be lower for an annuity that is due at the beginning.

Appropriate

An ordinary annuity is good if you have to make a payment. The annuity due is good if you get a payment because you get the money earlier. However, we also have to consider the interest factor when choosing between the two types of annuity.

Final Words

One simple way to remember the difference between ordinary annuity vs annuity due is to take the place of a payer and a beneficiary and consider what situation is of benefit to you. If, for example, you are obliged to receive the money, it is better that you receive it at the beginning of the due period, and if you have to make the payment, it is better for you to make the payment at the end of the period of the ordinary annuity). In this way, you are able to keep your money for a further period.

When choosing between the two, however, you must not only rely on the status of the payer and recipient but also take other factors into account. Although the difference between the two is marginal, it can make a big difference to your savings in the long run. Therefore, you should consider both your risk level and investment objectives when deciding between the two factors. If possible, you can also seek the help of a financial adviser.

Continue reading – Perpetuity

FAQs

If you have to make payments, an ordinary annuity is better, and if you have to receive payments, an annuity due is better because it offers a higher present value.

The timing of the payment is the most fundamental difference between the two types of annuities. In the case of an ordinary annuity, the payment is due at the end of the period, whereas in the case of an annuity due, the payment is made at the beginning of the period.

The future value of the annuity due is higher than the ordinary annuity because it gets one extra period for accumulating interest.