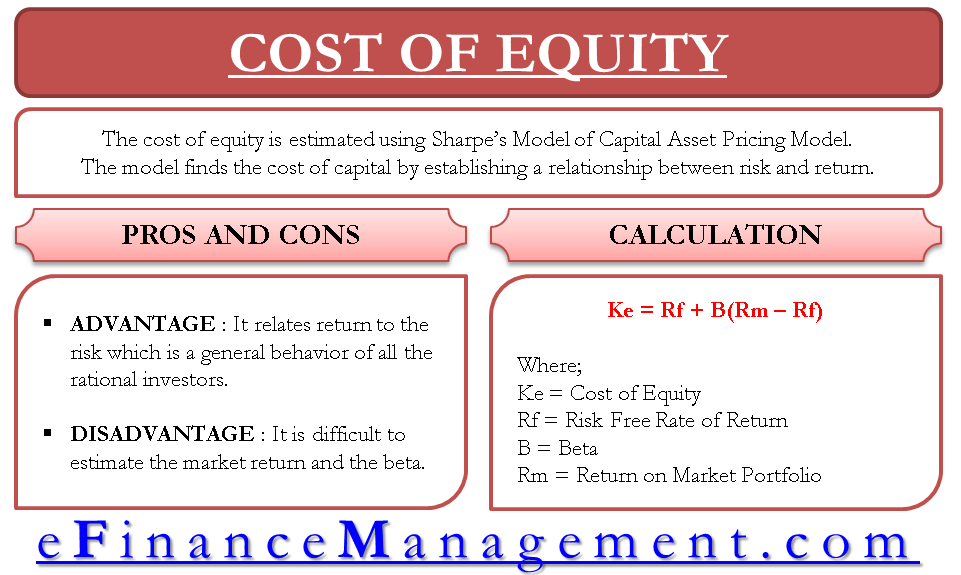

The cost of equity is estimated using Sharpe’s Model of Capital Asset Pricing Model. The model finds the cost of capital by establishing a relationship between risk and return. As per this model, at least a risk-free return is expected out of every investment and the expectation greater than that is dependent on the amount of risk associated with the respective investment. As per this model, the required rate of return is equal to the sum of the risk-free rate and a premium based on the systematic risk associated with the security.

Systematic Risk and Unsystematic Risk

Systematic Risk is that risk that is unavoidable by diversifying the investments. This risk includes the factors which affect the overall market and not a particular stock in the market viz. changes in economic conditions, inflationary situations all over the world, etc. Beta (β) is the measurer of this risk.

Unsystematic Risk is the stock-specific risk that affects only a particular stock price and not the whole market. Such a risk can be diversified and reduced to a great extent by diversifying a portfolio.

Capital Asset Pricing Model (CAPM)

The result of the model is a simple formula based on the explanation just given above.

ke = Rf + (Rm – Rf)β

ke = Required rate of return or cost of equity

Rf = Risk-free rate of return, normally the treasury interest rate offered by the government.

Rm = It is the expected return from the Market Portfolio.

β = Beta is a measure of risk in the equation.

Market Portfolio conceptually means the portfolio of shares containing all the shares trading in the market with their weights as their market capitalization. Practically, we can take a portfolio that has all the industries and has sufficient stock of each industry to diversify the stock-specific risks. The objective of taking the market portfolio is that we want a portfolio that has diversified all the avoidable risk and such a portfolio cannot be more than a market portfolio.

Beta is the measure of the responsiveness of an individual stock’s return due to a change in market return. The higher the beta of security, the higher would be the required rate of return by the investor. It impacts the required return because it has a direct multiplication impact on the premium. If the beta is 1, the stock return would be equal to the market return. If less than 1, a stock return would be less than the market return and if it is greater than 1, the required return of the stock is greater than the market return.

Example of Cost of Equity with CAPM

Suppose Rm is 20%, Rf is 8%, β is 1.2, the Rj would be

Rj = Rf + (Rm – Rf)β

= 8% + (20% – 8%)1.2

= 8% + 14.4%

Rj = 22.4%

In the above example, the risk-free rate of return is 8% and the market risk premium of the stock is higher than 20% i.e. more than the market return. It is because the stock beta is greater than 1 i.e. 1.2.

Also Read: Advantages and Disadvantages of CAPM

Refer to Models for Calculating Cost of Equity to learn about different models.

Advantage and Disadvantages of CAPM

Finding the cost of equity with the CAPM model is widely used. the primary advantage of this model is that it relates to return to the risk which is a general behavior of all rational investors. The disadvantage is that it is difficult to estimate the market return and the beta.

To learn more you can visit our article Advantages and Disadvantages of CAPM

Frequently Asked Questions (FAQs)

CAPM was developed by Willian Forsyth Sharpe

Beta impacts the required return because it has a direct multiplication impact on the premium. If the beta is 1, the stock return would be equal to the market return. If less than 1, a stock return would be less than the market return and if it is greater than 1, the required return of the stock is greater than the market return.

The formula for calculating CAPM is:

Rf + (Rm – Rf)β

Quiz on Cost of Equity – CAPM

This quiz will help you in taking a quick test of what you have read

Thank you for the website, it is a very usefull tool!

May I ask you what you would consider as the best asset pricing model?

Thank you very much.

Ralf