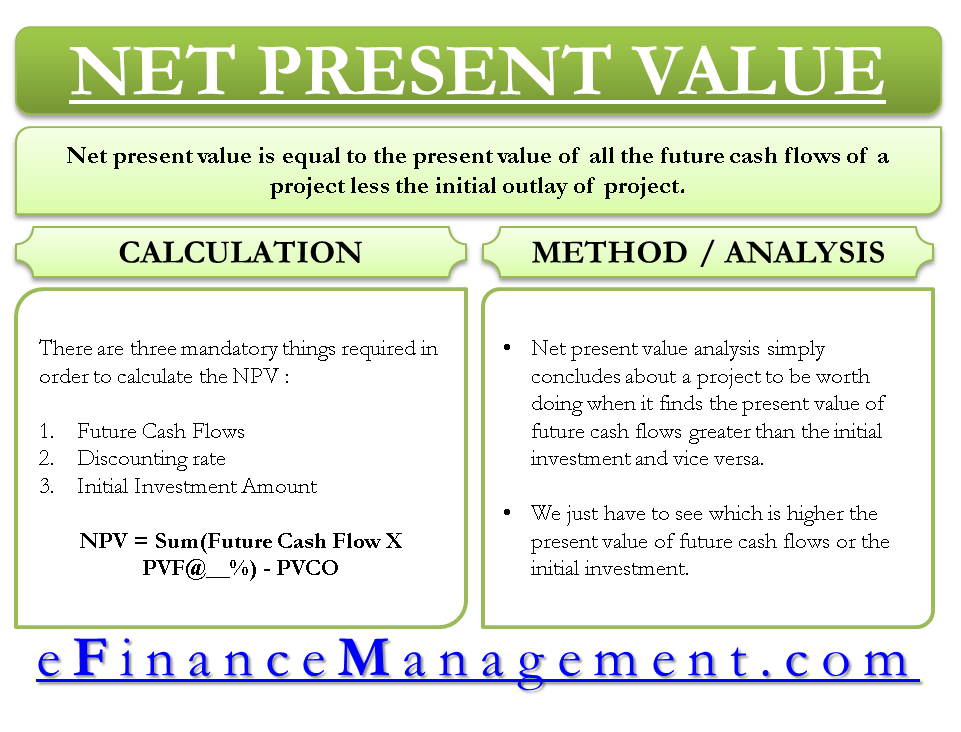

Net present value or NPV is a very well-known technique for analysis in the arena of finance. Net present value is equal to the present value of all the future cash flows of a project less the project’s initial outlay. It is very important and helpful in arriving at the decisions related to investment in projects, plants, or machinery.

Definition and Meaning of NPV

Net present value is the present value/today’s value of all the cashflows to be generated by an asset in the future. In other words, it is the value that can be derived using an asset. Alternatively, it is the discounted value based on some discount rate. Banks, financial institutions, investment bankers, venture capitalists, etc., are also widely used to assess an asset or even a business for arriving at its valuation.

Calculation of net present value requires three things, viz. stream of future cash flows (inflows or outflows), a discounting rate, and the initial investment amount. We need to discount the future cash flows to present value using the appropriate discount rate and deduct the initial investment from the total of all the present values arrived after discounting.

The formula for Net Present Value (NPV):

Net Present Value (NPV)

C1

C2

C3

Cn

=

—

+

—

+

—

……..

—

–

Initial Investment

(1+r)1

(1+r)2

(1+r)3

(1+r)n

Where Cn = Cash Flow at time n.

Future Cash Flows: Future cash flows are the expected cash flow to be received by the investor on the proposed investment. Discount Rate: It is the highest rate of return that the investor can earn by investing the same money in some other investment alternative. In other words, a discount rate is the opportunity cost of capital which means the cost of compromising the other opportunity. Initial Investment: The initial investment is the cash outflow at the beginning of the project, like the cost of machinery, etc.

Let’s understand NPV with an example. Suppose you bought machinery worth 2 Million Dollars, and it will fetch 0.5 Million Dollars every year for 6 Years, and there will be no scrap value for the machine. What should you do? Invest or Not? Apparently, somebody may say you are investing 2 million but getting 3 million, so you should go for it. Let’s say you have another opportunity to invest the same money @ 14% per annum. The following example explains that the opportunity is not worth investing in if your opportunity cost or discount rate is 14%. Cash flows are discounted by 14%, and we find that their present value is 1.94 Million. Would you enter into the deal if you are offered 1.94 Million in exchange for 2 Million today? Obviously, a rational person would not entertain that.

Cash Flow

Year

Amt

Discount Factor: (1/1+14%)^n

Present Value

C1

1

5,00,000

1.14

4,38,596

C2

2

5,00,000

1.3

3,84,734

C3

3

5,00,000

1.48

3,37,486

C4

4

5,00,000

1.69

2,96,040

C5

5

5,00,000

1.93

2,59,684

C6

6

5,00,000

2.19

2,27,793

Present Value of Future Cash Flows

19,44,334

Initial Investment

20,00,000

Project Not Worth

-55,666

Method and Analysis

The net present value method determines whether a project/investment is worth doing by comparing two things: initial investment and the total value of future cash flows. Net present value analysis concludes that a project is worth doing when it finds the present value of future cash flows greater than the initial investment and vice versa. It brings the complicated stream of cash flows into a simple weighing scale situation where you can easily know which is heavier. In our context, we have to see which is higher, the present value of future cash flows, or the initial investment.

Calculation of Net present value (NPV) and NPV tables

The calculation of the net present value is a little complicated due to the presence of power over the numeric values. There are pre-calculated tables of a combination of different discount rates and periods to make it simple. NPV tables are used for the sake of simplicity of calculations. Nowadays, all such applications are available in excel and are widely used. Not just a formula is available, but specific tools are also available.

Net present value has a close relation with capital budgeting. Capital budgeting requires extensive use of the NPV technique. NPV method is one of the chief methods used in capital budgeting.

We cannot deny that NPV is the best techniques for analyzing projects, but the final decision about the project cannot be made just based on this. It is always advisable to look at all the sides of the dice. There are many other metrics that are consulted, such as return on investment, profit margin, cash flows, return on assets, tax implications, different kinds of risks, etc.

Sanjay Borad, Founder of eFinanceManagement, is a Management Consultant with 7 years of MNC experience and 11 years in Consultancy. He caters to clients with turnovers from 200 Million to 12,000 Million, including listed entities, and has vast industry experience in over 20 sectors. Additionally, he serves as a visiting faculty for Finance and Costing in MBA Colleges and CA, CMA Coaching Classes.

4 thoughts on “Net Present Value (NPV)”

Simple and superb explanation. You are doing such great favor to the learners like me.

Thank you, sir.

")

")

")

Simple and superb explanation. You are doing such great favor to the learners like me.

Thank you, sir.

I concur with what was said above “Simple and superb explanation”

Yes I am very much impressed and indeed you have done a superb job – simple and straight forward. What more can I say. You are good.!!!!!!!!

Year Outlay (Investment cost in USD) Cash flow (in USD)

0 6,000 200

1 500 3500

2 0 2000

3 0 1000

4 150 800

If the interest rate is 10%; calculate the discounted payback period. Please help by giving the answer