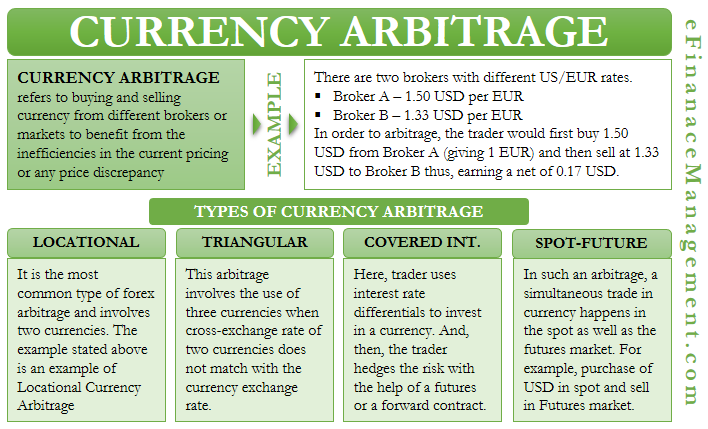

Arbitrage is a trading strategy in finance that is possible due to the inefficiencies in a market. And currency arbitrage is no different. In this, a currency trader benefits from the price difference in quotes by various brokers or in a different market to make a profit. In simple words, we can say it means buying and selling currency from different brokers or markets to benefit from the inefficiencies in the current pricing or any price discrepancy, if any.

Let’s consider a simple example to understand currency arbitrage. Suppose there are two different brokers – A and B – for US/EUR currency pair. Broker A sets the price at 1.5 dollars per euro, while Broker B sets the rate for the same currency pair as 1.33 dollars per euro.

To execute a forex arbitrage, the trader would first convert one euro into dollars with Broker A. Then. The trader will go to Broker B and convert dollars into euros. First, when a trader turns one euro into a dollar, he gets 1.5 dollars. Then he converts 1.5 dollars into euros to get 1.33 euros. This way, the trader makes a profit of about 0.17 euros.

Currency arbitrage exists not because of the movements in the currency rates but due to the differences in quotes. Currency traders usually go for a two-currency arbitrage, like the one in the example. There is also a three-currency arbitrage, but it is infrequent.

Types of Currency Arbitrage

Following are the common types of forex arbitrage:

Locational Arbitrage

Locational arbitrage is the most common type of forex arbitrage and involves two currencies. We have already given an example of this type of arbitrage above. Let us take another example, but this time with a Bid/Ask spread.

Suppose Bank A has USD 1.52/1.57 for GBP, while Bank B quotes USD 1.58/1.60. In this case, the trader would buy one GBP from Bank A at $1.57 and sell it to Bank B at $1.58. This way, the trader makes a profit of $0.01 per GBP.

Let us take the same example, but with a different bid/ ask spread. Bank A quotes USD 1.52/1.57 for GBP, but Bank B quotes USD 1.56/1.60. In this case, the arbitrage opportunity does not exist. If a trader buys GBP at Bank A for $1.57 and sells to Bank B at $1.56, the trader will incur a loss of $0.01 per GBP.

Triangular Arbitrage

As the name suggests, this arbitrage involves the use of three currencies. Such a type of arbitrage exists if the cross-exchange rate of two currencies does not match with the currency exchange rate.

In triangular arbitrage, we calculate the cross-exchange rate of two currencies and then compare it with the actual rate in the exchange. Thus, we can say the triangular arbitrage benefits from the irregularities in the cross rates. For instance, we can use USD/EUR and USD/GBP to calculate the cross-exchange rate of GBP/USD.

Let us take an example to understand this arbitrage. Suppose, at a given time, the following are the exchange rates – USD 1.4/EUR, USD 1.7/GBP, and EUR 1.5/GBP. Now, a trader needs to calculate the cross-exchange rate for EUR/GBP, using USD/EUR and USD/GBP.

In our case EUR/GBP will be 1.7/1.4 = 1.21. However, the actual EUR/GBP quote is 1.5. So, we can say that arbitrage opportunity exists. Let’s see how:

In this case, we first convert USD 1.7 into 1 GBP, then we convert this GBP into 1.5 EUR. Now, we turn this 1.5 EUR back into USD (1.5 * 1.4) to get 2.1 USD. We made a profit of $0.4 in this trade.

Covered Interest Arbitrage

Under covered interest arbitrage, a trader uses interest rate differentials to invest in a currency. And then, the trader hedges the risk with the help of a futures or a forward contract.

Uncovered interest rate arbitrage also exists. It is the same as covering one, but it does not have a futures or forward contract. In this type of arbitrage opportunity, the conversion happens between a local currency with a lower interest rate to other currencies with a higher interest rate.

Spot-future Arbitrage

In such an arbitrage, a simultaneous trade in currency happens in the spot as well as in the futures market. For example, you purchase USD in the spot market and then sell the same in the futures market to make a profit if there is any irregularity in pricing.

Currency Arbitrage – Risk

Arbitrage is supposed to be risk-free, but we can’t say the same about forex arbitrage. Forex traders face execution risk. It is the risk that the arbitrage opportunity may get lost because of the fast-moving nature of forex markets.

Because of the use of computer systems and algorithms, the price gaps or irregularities get quickly filled, resulting in fewer arbitrage opportunities. The key to currency arbitrage is timing because the trader needs to buy and then sell the currency instantly. Since the currency market is very liquid, there exist only a few opportunities for arbitrage. Moreover, these opportunities last just for a few seconds (or even a split of seconds) as the prices rapidly converge.

The forex market is heavily computerized and automated to take benefit of such split-second irregularities. Despite this, there exist arbitrage opportunities due to the volatile nature of the markets and price quote errors. But, the price discrepancies now last only for a sub-second in comparison to several seconds or even minutes earlier.

Final Words

Usually, high-frequency traders exploit currency arbitrage opportunities. Such traders deploy high-speed algorithms that not just identify any irregularity in the pricing but also execute the trade quickly. Such traders usually invest a considerable amount of time and money in developing algorithms and programs to identify pricing irregularities.

Also, it is because these traders only that markets get more efficient. Once these traders identify or benefit from any irregularity, the computer systems quickly fill the gap, making it impossible for others to benefit from the same trade.