Meaning of Liquid Assets

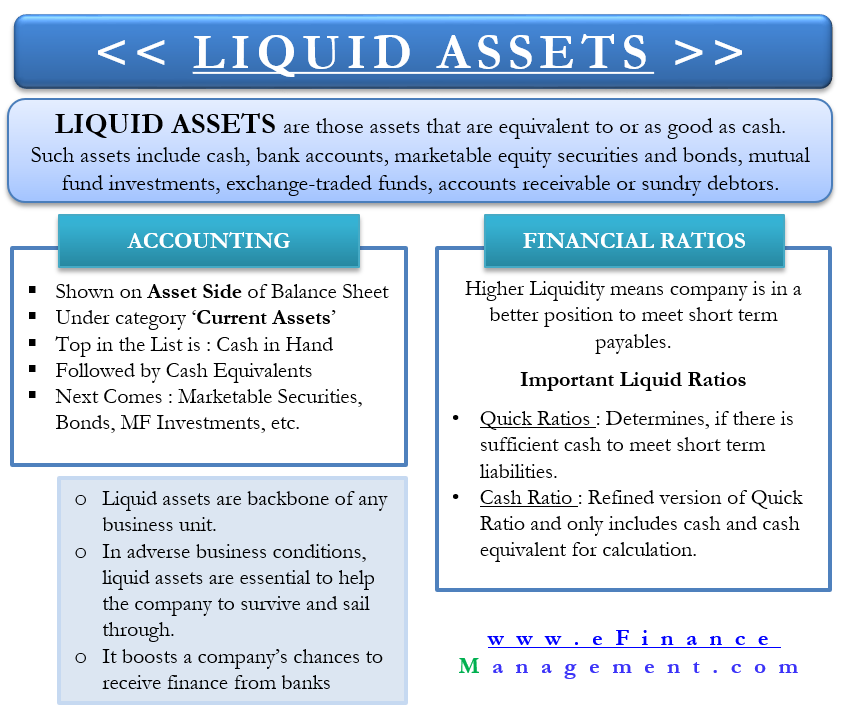

Liquid assets are those assets that are equivalent to or as good as cash. In other words, these are assets, the conversion of which into cash is easy and quick. The faster and easier the possibility of conversion, the more liquid that asset is. In accounting terms, liquid assets are cash or cash equivalents that are readily convertible to cash. Their liquidation is secure, meaning that the holder can convert them for cash without any issues. Also, it should happen in a short duration of time with little or no loss of value on conversion.

Features / Characteristics

Typical features of liquid assets are:

Easily Convertible / Transferable

The assets are convertible to cash easily and fast.

Economic Value

The assets have economic and financial value, and the value does not change substantially on conversion to cash.

Low Risk and Excellent Quality

These assets have an extremely low risk or nil risk of loss of value to the asset.

Deep Markets

These assets have developed securities exchanges or markets where the instruments trade without the risk of loss of value. The market makers are committed to the asset’s value like gold, treasury bills, and bill discounting markets.

Two Broad Categories / Types of Liquid Assets

What are Assets?

Asset per se is a financial resource and could be tangible or intangible forms. Examples are goods, outstanding collectibles, cash, inventories, land, buildings, etc. All these have a financial value attached to them. An individual, company, business, NGO, Government, or any society could be the owner of these assets. These assets are usable for future financial benefits in cash or kind. All these are not liquid assets.

As stated earlier, liquid assets are assets in the form of either cash or cash equivalent, which can be converted to cash with minimum time-lapse and effort. The conversion should be at such a price that there is no loss of value or, at the most, a bare minimum loss to the principal amount.

We can categorize the liquid assets into the following two types:

Cash

Cash means coins, currency notes, and bills received but not deposited or banked. Here, there is no loss of value.

Cash Equivalent

On the other hand, cash equivalents are the legal tenders, banker’s acceptance, bank accounts, G-sec (Government Securities), T-Bills, marketable equity securities and bonds, mutual fund investments, exchange-traded funds, accounts receivable, or sundry debtors. Cash equivalents are the assets where the minimum loss of value might occur. Liquid assets, particularly financial instruments, should have a ready, organized market wherein they can be easily converted into cash. Also, the market should have a large number of buyers and sellers for an easy interface and liquidity.

In the context of businesses, a term of about three months or 90 days is generally considered for recognizing and classifying assets as liquid assets. In other words, assets that can be converted to cash or equivalent within 90 days are called liquid assets.

What is not a Liquid Asset?

A rare commodity or an asset that does not have ready buyers is not a liquid asset. For example, let us consider the case of a unique piece of a diamond. It can be a costly and highly valuable asset for the owner. But it will take time to sell it. Also, finding a buyer willing to pay the correct price for it can be difficult.

Similarly, a building can be precious and economically significant for the owner, be it a company or an individual. But if a sudden need for money arises, it cannot be used for the purpose. Finding the correct buyer immediately for selling the landed properties will be difficult. Moreover, selling it during the running business will be a distress sale, and hence, there will be a significant loss of money realization as compared to its fair market value. Therefore, such assets will not qualify for being liquid assets.

Also Read: Liquidity Risk

On the other hand, if a company has invested in mutual funds and wants to liquidate it for urgent money needs, it can easily do so. There is a ready market for mutual funds redemptions/encashment. Also, they can be exchanged for cash at the present market value itself, and that is too quickly even at stock exchanges. Therefore, they are a form of liquid assets.

Examples of Liquid Assets

Common List of Liquid Assets

Following are some common examples of liquid assets. However, it’s not an extensive list but can definitely serve as a reference.

- Cash on hand,

- Savings and current account balance,

- Gold,

- Government bonds,

- Bank deposits,

- Certificates of deposits,

- Liquid mutual fund investments,

- Other money market instruments,

- Treasury bills,

- Accrued income,

- Accounts receivables,

Common List of Non-Liquid Assets

Current assets like inventories are not usually considered liquid assets.

- Property,

- Patents, Machinery,

- Land,

- Trademarks,

- Common stock,

- Private company bonds,

- Work in progress

- Inventories

Common stock or shares of companies though actively traded on exchanges, may lose value if sold in sizable quantities for liquidity by owners, so theoretically, they are considered illiquid.

Importance of Liquid Assets

Individuals, businesses, governments, NGOs, or any entity for that matter need liquid assets to meet contingent liabilities, routine operational expenses or take advantage of opportunities that may arise unanticipated during life or business.

Fights Contingencies

Liquid assets are the backbone of any business unit, be it a small firm or a big multinational corporation. Suppose a company has limited liquid assets and more amounts stuck in accounts receivable or inventory. In that case, it may face a liquidity crunch to meet its immediate financial obligations and working capital requirements. Furthermore, in adverse business conditions like recession or sudden fall in demand in the market, liquid assets are essential to help the company to survive and sail through.

Smooth Functioning

Liquidity needs are also there for planned payments of general or recurring nature called operating expenses or day-to-day expenses. Since they ensure the smooth functioning of households or businesses, you don’t need to run every time to make arrangements for such requirements. As a result, one can concentrate on business or other priorities.

Good for Fund Raising

Also, in times of adversities, the liquid assets can be leveraged to raise new funds for the businesses. Bank loans are readily available to companies with better liquidity ratios.

Hedge

This category cannot be ignored for individual personal finance also. It is used to hedge the overall investment portfolio against volatile or risky assets. Those immediate financial obligations, health issues, accidents, deaths, or other such human life cycle contingencies will also require the disposal of liquid assets.

Adequacy of Liquid Assets

The adequacy of liquid assets for an entity depends upon the nature of its commercial and financial activity, type of industry, or business. The health and circumstances of the individual or the company’s financial soundness are also determining factors.

Excess or short of liquid assets is not favorable for the holder.

If Liquidity is Very Tight?

Tight liquidity means less liquid assets. Tighter the liquidity, then the assets are not kept idle and are earning returns. However, tight liquidity also sometimes leads to chances of opportunity loss of investments and business. It could mean that the assets are blocked in higher interest rate instruments or poor cash flow.

If Liquidity is Very Loose?

On the other hand, excess of these assets leads to a loss of investment in more productive activities like running the business. Or it means that assets are not invested in more profitable avenues, lying idle. So everyone needs to strike a delicate balance between the two extremes.

Balanced Approach

Every individual or business needs to have adequate liquid assets for the diligent and smooth functioning of activities and peace of mind. Adequacy is also vital for taking advantage of unforeseen opportunities that may appear worth exploring.

An adequate amount of liquid assets on the balance sheet boosts a company’s chances of receiving finance from banks and financial corporations. A company can use these assets to make quick payments for its purchases, get higher discounts, and get the best deals from suppliers, improving the company’s overall performance and profitability.

To conclude, funds should be available to take benefit of the opportunities, and at the same time, there should not be any loss on account of idle funds.

Financial Ratios

There are many financial ratios to measure the liquidity and ability of a company to pay off its short-term liabilities. Higher liquidity ratios mean the company is in a better position to meet its short-term or immediate financial obligations. These obligations can be repaying creditors or even meeting working capital requirements in times of distress.

Net liquid assets = Cash balance + bank balance + receivables less current liabilities.

Current liabilities are the short-term or immediate payment requirements – Routine expense bills and current obligations.

The most common liquidity ratios for a company are:

Quick Ratio

This ratio determines if the company has sufficient liquid assets in hand to meet its short-term obligations. The formula for quick ratio is:

Current assets (including accounts receivable but not inventory) / Current liabilities

Therefore, the quick ratio is a good indicator of a company’s liquidity as it excludes mostly non-liquid inventory. A ratio of less than 1 indicates that the short-term liquidity position is unhealthy, and the company might require to fulfill near-term obligations by selling long-term assets.

Cash Ratio

This ratio is a further refinement of the quick ratio and includes only cash or assets equivalent to the cash for calculation purposes. It does not include accounts receivables for calculation. It is so because its realization may take some time.

The formula for calculating this ratio is:

Current assets (Only cash and assets similar to cash)/ Current liabilities

This cash ratio cannot be less than 0.2 for a company to be called sound. Creditors look at this ratio closely to understand whether this can meet the debt obligations of routine nature. It also means debt servicing smoothly and regularly. However, the cash ratio is not an accurate or popular measure as compared to the Quick ratio or Acid-test ratio.

Standard Benchmark

There can not be a one-for-all standard benchmark or indicator, as it varies with the type of business or industry and its requirements. Nevertheless, over the years, the classic outlook is that if the ratio of liquid assets to the operational requirements remains equal, i.e., around 1:1, then it is reasonable. In financial analysis parlance, this ratio is part of Liquidity Ratios.

Accounting Treatment of Liquid Assets

The listing of liquid assets happens on the assets side of the balance sheet. These assets are recorded in the broad category of “current assets,” which can be converted into cash within one year. Cash itself is topmost on the list. Then come cash equivalents like bank accounts which are as good as cash. Marketable equity securities and bonds, mutual fund investments, exchange-traded funds, etc., come next. They may take a few working days for liquidation.

Accounts receivable and inventory are semi-liquid types of liquid assets as their realization is subjective. And liquidation may take some time, even a few months. Fixed assets like land, building, machinery, etc., come last. Liquidation of such assets is not easy and can take considerable time too. These are more or less not liquid.

Please note that for banking companies and non-banking financial setups, liquid assets may be placed differently on their balance sheets.