Statement of Stockholders Equity (or statement of changes in equity) is a financial document that a company issues under its balance sheet. The purpose of this statement is to convey any change (or changes) in the value of shareholder’s equity in a company during a year. It is a required financial statement from a US company whose shares trade publicly.

Business activities that have the potential to impact shareholder’s equity are recorded in the statement of shareholder’s equity. Or, we can say it shows all equity accounts that may affect the equity balance, such as dividend, net profit or income, common stock, and more.

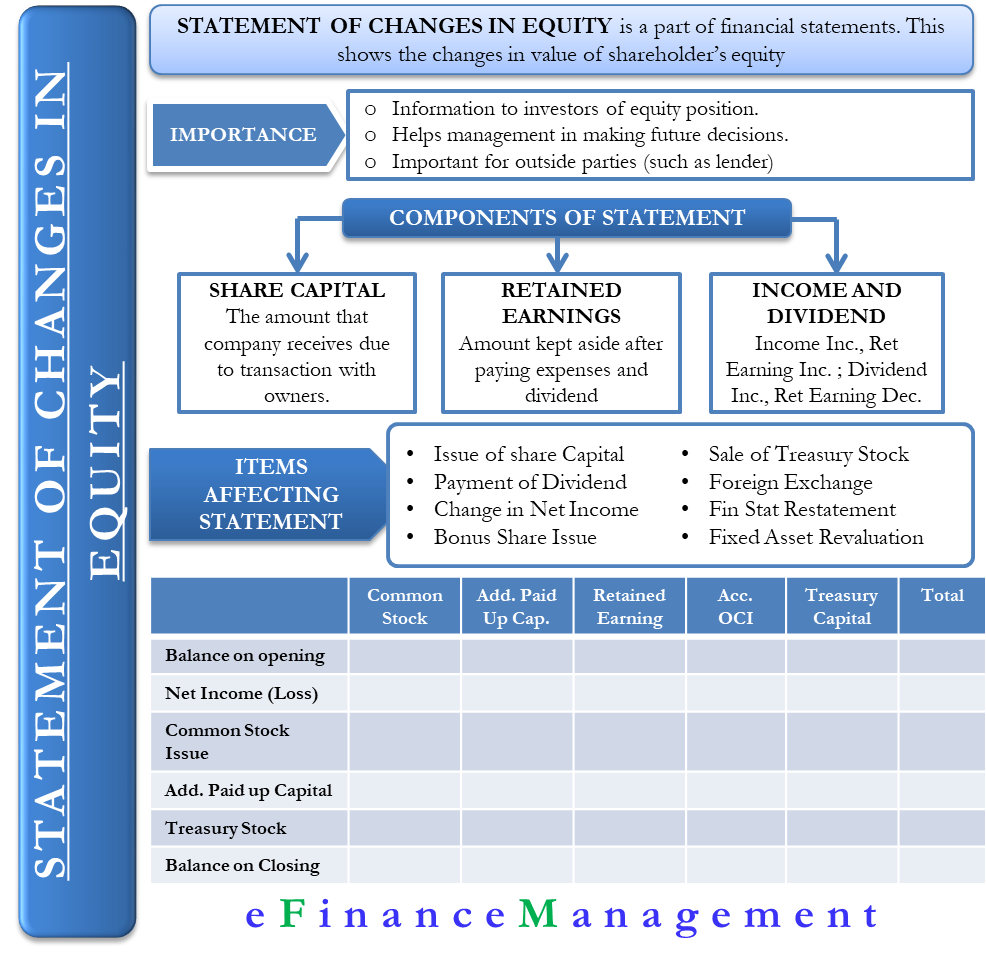

Importance of Statement of Stockholders Equity

Usually, a company issues the statement towards the end of the accounting period to give information to the investors about the equity position and sentiment towards the company. The statement allows shareholders to see how their investment is doing. It also helps management make decisions regarding future issuances of stock shares.

The statement is also of importance to the outside parties. For instance, those who gave a loan to the company would want to know how the company is maintaining the minimum equity levels to meet the debt agreements.

Also Read: Statement of Retained Earnings

Calculation of Shareholder’s Equity

Shareholder’s equity is basically the difference between total assets and total liabilities.

Shareholder’s equity = Assets – Liabilities

Another way to calculate Shareholder’s Equity = Contributed Capital + Retained Earnings

Components of Stockholder’s Equity

Several components affect the shareholder’s equity. These factors, however, can be divided into a few broader categories such as:

Share Capital

This includes the amount a reporting entity receives due to a transaction with its owners.

Retained Earnings

The amount that a company keeps aside after paying all the expenses and dividends is known as retained earnings. A company may use retained earnings for various purposes such as re-investing, expanding, new product launches, etc. An increase or decrease in retained earnings directly affects the stockholder’s equity.

Net Income and Dividends

Retained earnings increase with an increase in net income and drop if net income drops. Similarly, retained earnings drop with the increase in dividend payment and vice versa.

Other relatively less popular components are Treasury stock Capital reserve(s), Revaluation surplus, profit or loss from the sale of securities, and gains and losses on cash flow hedge.

Items Affecting Shareholder’s Equity

Primarily there are two types of changes that affect the shareholders’ equity. First, the changes resulting from transactions with the shareholders, and second, changes due to any change in total comprehensive income. Both these factors have several sub-factors, which are listed below;

- The issue of new share capital increases the common stock and additional paid-up capital components.

- Payment of cash dividends lowers the retained earnings of the company.

- Net income increases the retained earnings, whereas net loss decreases them.

- Treasury stock purchase increases the stock component and brings down the net shareholders’ equity.

- Bonus share issue impacts the additional paid-up capital, retained earnings, and common stock.

- Sale of treasury stock drops the stock component and impacts the retained earnings along with additional paid-up capital. This, however, increases the total shareholders’ equity.

- Foreign exchange might increase or decrease the foreign exchange reserve.

- Financial statement restatement might occur due to the change in accounting principle, and it affects retained earnings.

- Fixed asset revaluation affects the revaluation surplus by increasing it. Similarly, the reversal of the revaluation of fixed assets may decrease the revaluation surplus.

Format of Statement of Stockholder’s Equity

Since the statement includes net income/loss, a company must prepare it after the income statement. Like any other financial statement, the statement of stockholders’ equity will have a heading showing the name of the company, time period, and title of the statement.

Usually, the statement is set in a grid pattern. The statement typically consists of four rows – Beginning Balance, Additions, Subtractions, and Ending Balance. Beginning balance is always shown in a fixed line followed by additions and subtractions. The addition consists of all the new investments and net income in case the company is profitable. In case the company incurs a loss, it will show a net loss for the year under the subtractions in addition to the dividends (if any).

The last line of the statement of stockholders’ equity will have the ending balance, which is the outcome of the beginning balance, additions, and subtractions. There could be more rows depending on the nature of transactions a company may have.

The statement may have the following columns – Common Stock, Preferred Stock, Retained Earnings, Treasury Stock, Accumulated other comprehensive income or loss, etc. There could be more columns if required.

Example

Below is an example of the grid pattern statement of stockholder’s equity.

XYZ Ltd

Statement of Stockholder’s Equity for the year ending December 31, 2019

| Common Stock | Additional Paid-in Capital | Retained Earnings | Accumulated Other Comprehensive Income | Treasury Stock | Total | |

| Balance on January 1 | – | – | – | – | – | – |

| Net Income (Loss) | 197,100 | 197,100 | ||||

| Common Stock Issued | 10,000 | 10,000 | ||||

| Additional Paid-in Capital | 20,000 | 20,000 | ||||

| Treasury Stock | (2,000) | (2,000) | ||||

| Balance on December 31 | 10,000 | 20,000 | 197,100 | – | (2,000) | 225,100 |

Another Method

Another way to prepare the statement is to use a single column of numbers instead of the grid style. In this method, all items are listed in a single column, starting with the opening balance of shareholders’ equity and then adjusting for any changes during the period. The number of rows is similar to in grid one.

Example

XYZ Ltd

Statement of Stockholder’s Equity for the year ending December 31, 2019

| Balance on January 1 | $61,000,000 |

| Issued shares for cash | 16,000,000 |

| Purchase of treasury stock | (3,000,000) |

| Net Income | 5000,000 |

| Cash Dividends | (1,600,000) |

| Stock Dividends | 0 |

| Balance on December 31 | 77,400,000 |

Interpretation and Decisions based on Stock Holders Equity Statement

This statement is an important one and helps the management as well as the shareholders/investors to take or understand certain decisions. This statement guides for those decisions that could be:

Further Issue of Shares

This statement can give an understanding of whether any further issue of equity or common stock is possible or not. For example, if the company has already issued all the shares, then in the normal course, no more shares could be issued. Similar way, if there exists a partly paid share, then the company can use the opportunity to garner resources by making those shares fully paid up by making a final call.

Buy Back of Shares

If the company is of the opinion that there are excess liquidity and a large number of shares under circulation. And this excess circulation is adversely affecting the value or worth of the shares. Or if there is a panic selling by the investors either based on rumors or at the instance of the competitors. Then the company management can make a decision to buy back part of the floating shares, thereby providing value to the shareholders.

Dividend Declaration

The quantum and distribution of shareholding help the management in taking a judicious decision with regard to the declaration and distribution of the dividend. And to conserve and plough back the resources for the growth of the company where the ROI is greater.

Employee Stock Option Plan (ESOP)

This statement again helps the management in making a decision with regard to floating a scheme for ESOP. The quantum thereof, threshold, etc. ESOP is the scheme where the employees get the right to subscribe for and hold the equity stock of the company. This statement depicts the success of the scheme, the quantum already taken up, and the money collected under the scheme.

Thanks really these is so Interested and I like it.

Hey,

Thanks for the detailed info.