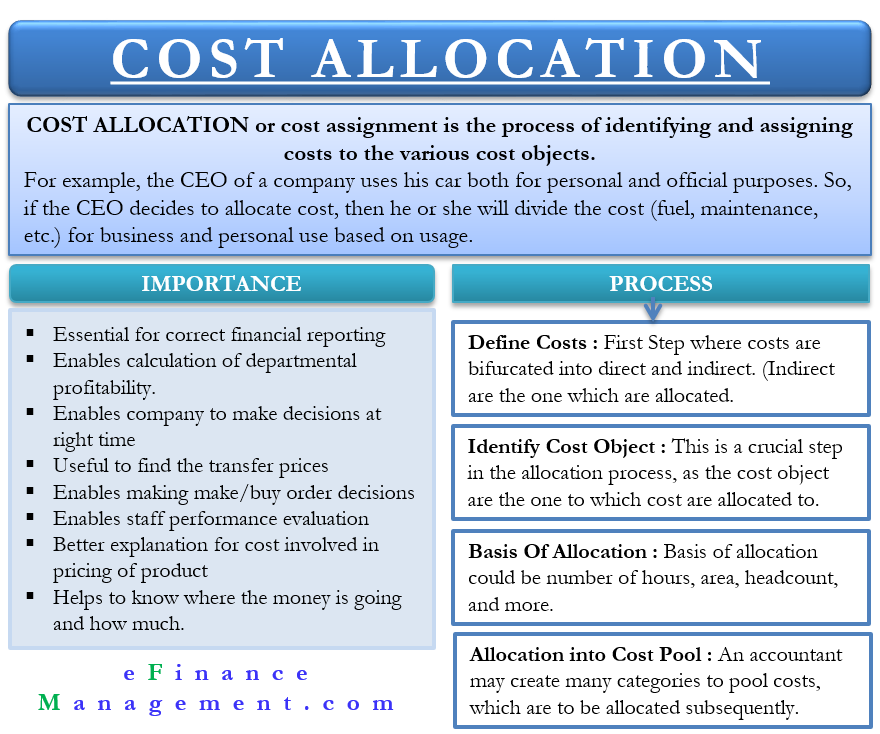

Cost Allocation or cost assignment is the process of identifying and assigning costs to the various cost objects. These cost objects could be those for which the company needs to find out the cost separately. A few examples of cost objects can be a product, customer, project, department, and so on.

The need for cost allocation arises because some costs are not directly attributable to the particular cost object. In other words, these costs are incurred for various objects, and then the sum is split and allocated to multiple cost objects. These costs are generally indirect. Since these costs are not directly traceable, an accountant uses their due diligence to allocate these costs in the best possible way. It results in an allocation that could be partially arbitrary, and thus, many refer cost allocation exercise as the spreading of a cost.

For example, a company’s CEO uses his car for personal and official purposes. So, if the CEO decides to allocate costs, then they will divide the cost (fuel, maintenance, etc.) for business and personal use based on usage.

Examples of Cost Allocation

The following examples will help us understand the cost allocation concept better:

- A company has a building in which there are various departments. One can allocate depreciation costs to the department on the basis square ft area of each department. This cost will then be further assigned to the products on which the department works.

- An accountant can attribute electricity that a production facility consumes to different departments. Then the accountant can assign the department’s electricity cost to the products that the department works on.

- An employee works on three products for a month. To attribute their salary to three products, an accountant can use the number of hours the employee gave to each product.

Cost Allocation – Importance

The following points reflect the importance of allocating costs:

- Allocating cost is essential for financial reporting, i.e., to correctly assign the cost among the cost objects.

- It allows the company to calculate the true profitability of the department or function. This profitability could serve as the basis for making further decisions for that department or service.

- If cost allocation is correct, it allows the business to identify and understand the costs at each stage and their impact on the profit or loss. On the other hand, if the allocation is incorrect, the company may end up making wrong or inconsistent decisions concerning the distribution of resources amongst various cost objects.

- The concept is also useful for finding the transfer prices when there is a transaction between subsidiaries.

- It helps a company make better economic decisions, such as whether or not to accept a new order.

- One can also use the concept to evaluate the performance of the staff.

- It helps in better explaining to the customers the costs that went into the pricing of a product or service.

- Allocation cost helps a company know where the money is going and how much. It will assist the company in using the resources effectively. Pool costs, if not allocated, may give an unbalanced view of the cost of various objects.

Cost Allocation Method

As such, there is no specific method to allocate costs. So, an accountant needs to use his or her due diligence to assign a cost to the cost object. Of course, they are considering the practice adopted in a similar industry. For instance, the accountant may decide to allocate expenses based on headcount, area, weightage, and so on.

Irrespective of the method an accountant uses, their objective should be to allocate the cost as fairly as possible. Or to allocate cost in a way that is in line with the nature of the cost object. Or to lower the arbitrariness in awarding costs.

Several efforts are underway to better cost allocation techniques. For instance, the overhead allocation for manufacturers, which was on plant-wide rates, is now based on departmental standards. Also, accountants use machine hours instead of direct labor hours for allocation.

Moreover, some accountants are also implementing activity-based costing to better the allocation. So, there can be several ways to allocate costs. But, whatever form the company selects, it is essential to document the reasons backing that method, and that need to be followed consistently for several periods.

A company can ensure documentation by developing allocation formulas or tables. Moreover, if a company wants, it can also pass supporting journal entries to transfer costs to the cost objects or do it via the chargeback module in the ERP system.

Also Read: Cost Hierarchy – Meaning, Levels and Example

Nowadays, cost allocation systems are available to assist in cost allocation. Such systems track the entity that produces the goods or services and the body that consumes those goods or services. The system also identifies the basis to distribute the cost.

The process to Allocate cost

As said above, there are no specific methods for allocating costs. Similarly, there is no particular process for it, as well. However, the process we are detailing is one of the most popular, and many companies use it for allocating costs. Following is the process:

Define Costs

Before allocating the cost, a company must define the various types of costs. Generally, there are three types of costs – direct, indirect, and overhead. Direct costs are those that one can easily attribute to a product or service, such as wages to factory workers or raw material for the specific product.

Indirect costs are ones that a company needs to incur for its operations, such as administration costs. Primarily, these are the costs that a company needs to allocate as it is difficult to attribute them directly to a product or service or any other cost object.

Another type of cost is an overhead cost, which is also an indirect cost. These costs are incurred for the production and selling of goods or services. Such costs do not vary based on production or sales. A company needs to pay them even if it is not producing or selling anything. Research and development costs, rent, etc., are good examples of such a cost.

Identify Cost Objects

The company or the accountant must know the cost objects for which they need to allocate the cost. It is crucial as we can’t assign costs to something on which we have no information. A cost object could be the product, customer, region, department, etc.

Basis of Allocation

Along with the cost object, the company must also determine the basis on which it would allocate the cost. This basis could be the number of hours, area, headcount, and more. For example, if headcount is the basis of allocation for insurance costs and a company has 500 employees, then the department with 100 employees will account for 20% of the insurance cost. Experts recommend choosing a cost allocation base that is a crucial cost driver as well.

A cost driver is a variable whose increase or decrease leads to an increase or decrease in the cost as well. For instance, the number of purchase orders could be a cost driver for the cost of the purchasing department.

Accumulate costs Into Cost Pool

An accountant may create many categories to pool costs, which are to be allocated subsequently. It is the account head where the costs should be accumulated before assigning them to the cost objects. Cost pools can be insurance, fuel consumption, electricity, rent, depreciation, etc. The selection of the cost pool primarily depends on the use of the cost allocation base.

Continue reading – Costing Terms.