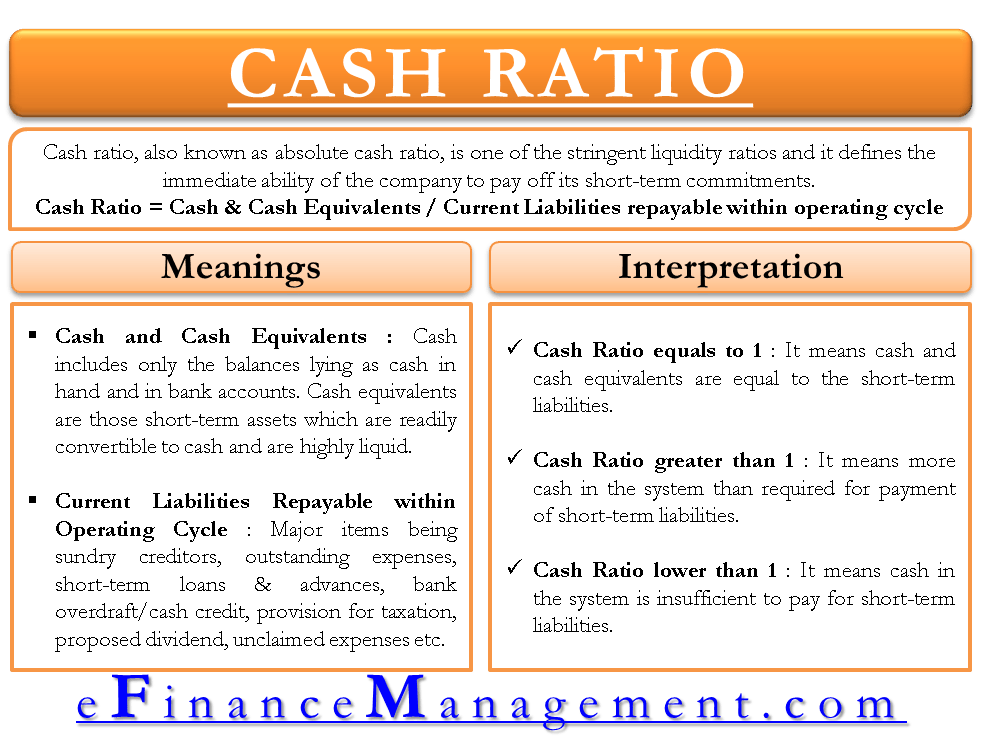

The cash ratio, also known as the absolute cash ratio, is one of the stringent liquidity ratios. It defines the immediate ability of the company to pay off its short-term commitments. Other vital liquidity ratios are the current ratio and quick ratio (or acid-test ratio). The cash ratio is helpful for creditors in assessing the probability of timely payment of their dues.

Calculation / Formula

The calculation of the cash ratio involves cash and cash equivalent to current assets and current liabilities. The formula for cash ratio is as follows:

Cash Ratio = Cash and Cash Equivalents / Current Liabilities payable within 12 months or Operating Cycle

Cash & Cash Equivalents

Cash includes only the balances lying as cash in hand and bank accounts. Cash equivalents are those short-term assets that are readily convertible to cash and are highly liquid, for example, stocks, bonds, government securities, treasury bills, bank deposits, money market instruments, etc. The primary purpose is to include only those assets whose encashment is readily possible within a very short time, say 3 months or so. Here, closing stock, debtors, and miscellaneous expenses are not considered because they are not the cash equivalent.

While calculating the ratio, the value of cash equivalents should be the net realizable value (NRV). NRV is the value or amount which can be realized if sold immediately. NRV is taken to avoid the risk of change in the market value of the investments.

Current Liabilities Repayable within Operating Cycle

This ratio intends to find out the capacity of the company to meet its short-term debts using its most liquid items. The short-term debts are debts repayable within 12 months of the operating cycle. Major items are sundry creditors, outstanding expenses, short-term loans & advances, bank overdraft/cash credit, provision for taxation, proposed dividend, unclaimed expenses, etc. The more the cash ratio, the more efficient the company is in paying off its short-term dues.

Example

Let’s assume a balance sheet of a company as on 31.03.2013 as follows:

Liabilities

Amount

Assets

Amount

Equity share capital

5,00,000

Fixed Assets

5,00,000

Reserves & Surplus

1,50,000

Investments

1,00,000

Unsecured Loans

70,000

Current Liabilities-Sundry Creditors-outstanding Expenses

-Provision for Tax

50,00018,000

12,000

Current Assets-Closing Stock-Debtors

-Cash in hand

-Cash at Bank

-Bank Deposit

-Treasury Bills

-Prepaid Expenses

50,00025,000

15,000

35,000

55,000

15,000

5,000

8,00,000

8,00,000

Cash Ratio

=

cash in hand+ cash at bank + bank deposit + treasury bills

sundry creditors +o/s expenses + provision for tax

=

15,000+35,000+55,000+15,000

50,000+18,000+12,000

=

1,20,000 / 80,000

=

1.5

Here, the cash ratio is 1.5, which signifies that there is excess cash after paying off current liabilities.

The interpretation of the cash ratio will vary from business to business. There is no such ideal ratio. Following is an indicative understanding of the ratio.

Cash Ratio equals to 1

It means cash and cash equivalents are equal to the short-term liabilities.

Cash Ratio greater than 1

It means more cash in the system than required to pay short-term liabilities. A company’s creditor will be happy with such a ratio as higher as possible because that will reduce the chances of any delay in paying his dues. But, on the other hand, the company would like to keep it low or optimized to suit its requirements because idle cash means unwanted loss of interest cost.

Cash Ratio lower than 1

It means cash in the system is insufficient to pay for short-term liabilities. A creditor of the company will assume more risk while extending credit to the company. In this case, they will rely on the company’s previous track record. The lowest possible cash levels with no delays in creditors’ payments in the company make the management happy because they see the savings in terms of interest cost on idle cash and effective cash management.

Various Other Interpretations of the High Levels of Cash in the Industry

Companies with large cash in the balance sheet indicate that there are limited growth opportunities available to the company; otherwise, such idle cash could have been used for expansion. From a mergers and acquisition point of view, these companies are the potential target for the acquirers. Last but not least, idle cash does not return anything, and hence opportunity cost of interest on idle cash is a direct dent in the company’s profits.

Sanjay Borad, Founder of eFinanceManagement, is a Management Consultant with 7 years of MNC experience and 11 years in Consultancy. He caters to clients with turnovers from 200 Million to 12,000 Million, including listed entities, and has vast industry experience in over 20 sectors. Additionally, he serves as a visiting faculty for Finance and Costing in MBA Colleges and CA, CMA Coaching Classes.

2 thoughts on “Cash Ratio”

Hello Sir,

The blog is awesome. I read the article and was great. This article extremely helps me. I also have a website that I mentioned in the website section. I also write blogs on finance. If possible kindly visit my website.

Thank you, Sir

Hello Sir,

The blog is awesome. I read the article and was great. This article extremely helps me. I also have a website that I mentioned in the website section. I also write blogs on finance. If possible kindly visit my website.

Thank you, Sir

Thanks Chayan for taking out time. I will surely visit your site. You can share URL with me. Best of luck.