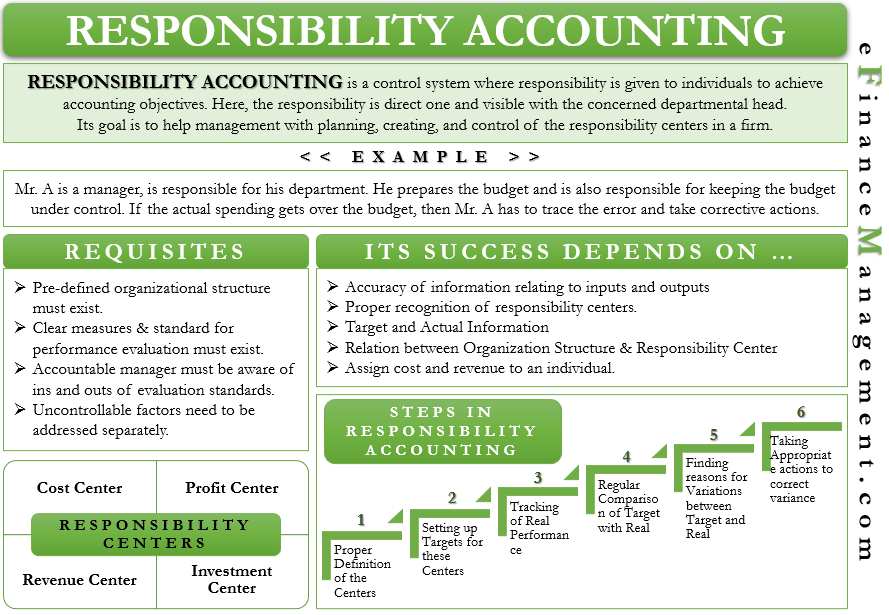

Responsibility Accounting helps management with cost and budgetary control. It focuses on the cost drivers but not on who uses or who is responsible for those drivers. On the other hand, responsibility accounting is a control system where responsibility is given to individuals to achieve particular accounting objectives.

In other mechanisms or control matrix, this responsibility still rests with the departmental managers, but it remains indirect. Whereas, in responsibility accounting, this is a direct one and visible with the concerned departmental head.

Responsibility accounting involves the budgeting and the internal accounting for every responsibility center in a firm. Its goal is to help management plan, create, and control the responsibility centers in a firm.

This type of accounting primarily involves preparing monthly and annual budgets for every responsibility center. It also takes into account the cost and revenue of a firm. The management maintains the monthly, quarterly, or yearly reports, then sent to the manager responsible for that department.

Also Read: Cost Accounting and Management Accounting

We can say every department in a company gets a report that includes its monthly budget, as well as the actual amount for the most recent month. The report may also have a year-to-date budget and actual spending.

Example

For example, Mr. A is a manager who is responsible for his department. He prepares the budget and is also responsible for keeping the budget under control. So for the efficacy of such a system, management must provide him all sorts of information, good or bad, about his department. It would make him fully aware of how things are moving and the areas where his strict attention is needed. If the actual spending gets over the budget, then Mr. A has to trace the error and take corrective actions. In all, we can say that Mr. will be personally accountable for his department’s performance.

Requisites of Responsibility Accounting

The following are must for efficient implementation of responsibility accounting:

- A company must have a clearly defined organizational structure that is understandable to all without any ambiguity.

- There should be clear measures and standards for the evaluation of performance.

- A manager who is accountable for a responsibility center must know all the evaluation parameters with utmost clarity in advance.

- All those accountability and evaluation parameters should be controllable at the level of the manager.

- Uncontrollable factors need to be addressed separately.

Responsibility Centers

The following are the types of responsibility centers:

Cost Center

It is a unit in a company that has control over the cost only, such as the production department. The cost center does not exercise control over other functions, such as revenues or investments. A point to note is that a manager responsible for any cost center is only responsible for the controllable costs and not uncontrollable costs.

Revenue Center

This unit is only responsible for generating revenues and not any other business function. The sales and marketing departments are an example of a revenue center.

Profit Center

Profit center is accountable for both costs and revenues. One example of this is the factory, whose cost is the raw material, and revenue is the products it transfers to other departments. Also, branches of a company in different regions are responsible for both costs and revenues.

Investment Center

Investment center has control over costs, revenues, and investments. Or, we can say the person is responsible for investing the assets of a company most efficiently. Such a cost center works as a separate entity, such as a corporate headquarters. A company measures the performance of an investment center by using ratios, such as ROI (return on investment), economic value-added, and more.

Steps of Responsibility Accounting

The following are the steps for its proper implementation:

- Properly define responsibility centers.

- Setting targets and responsibilities for the responsibility centers.

- Continuously track their real performance.

- Regularly compare the real performance with the set target.

- Find out the reason (or reasons) for a variance between the actual and target performance.

- Management takes action to correct the variance. Also, the management informs about the same to the responsibility center.

Components of Responsibility Accounting

The following are the components that help a company to implement this accounting system efficiently:

Inputs and Outputs

Effective implementation depends on the accuracy of information relating to inputs and outputs. The data on raw materials, such as labor hours and quantity, is input, while data on finished products is the output.

Responsibility Center

It is the most critical component. The full responsibility accounting system depends on the proper recognition of responsibility centers.

Target and Actual Information

Data on the target, as well as the actual performance, is fundamental to evaluate the performance of a responsibility center.

Inter-relation of Organization Structure with Responsibility Center

Fixing or assigning responsibility goes with a clearly defined organizational structure. Hence, for the successful implementation of responsibility accounting, clarity of organization structure is very crucial. Similarly, a company must develop this accounting system to be in line with the organizational structure.

Assigning Cost and Revenue to an Individual

For the success of this accounting system, a company must assign cost and revenue to an individual. This individual will be responsible for the responsibility center.

Advantages

The following are the advantages of responsibility accounting:

- It encourages the management to make a proper company structure and a person accountable for every responsibility center.

- The manager is directly responsible for the outcome of their department, and their direct attention and engagement with the activities and team remains very high. Since a manager is responsible for the performance of their department, they are more attentive and aware of the happenings. It also helps them to explain performance variation (if any).

- It assists in comparing the actual results with the budgeted.

- This system makes employees more responsible and serious towards their work as they are aware that they are always under review.

- Management also gets assistance in preparing the plan and structure for the future expenditure and revenue of a company.

- Since it also works as a cost control system, it makes employees more ‘cost-consciousness.’

- This accounting system ensures that everyone is aware of the company and individual goals.

- It gives management better control over the company’s operating activities.

- It results is prompt reporting, as well as quick corrective action.

Disadvantages

The following are the disadvantages of responsibility accounting:

- Often it gets difficult to meet the prerequisites of the successful responsibility accounting system. It makes the whole system inaccurate.

- Since the system requires the presence of highly skillful managers, it raises the cost for the company.

- This accounting system only works with controllable costs but does nothing about uncontrollable costs.

- If a company is unable to communicate the goals and responsibilities to the person properly, then the system may fail to give accurate results.

- Suppose a company is unable to identify and share the triggers and variances to the manager timely. Delayed sharing or half-cooked figures will create more issues than they may solve.

- There could be situations when there is a clash between the individual and company goals. It may thwart efficient implementation.

- In the absence of an effective reporting system, this accounting method may fail to give accurate results.

Final Words

Responsibility accounting could prove very useful if a company can implement it properly. It gives the management with all information it needs on cost and revenue to make a practical decision. Moreover, it provides more freedom for the managers to show their skills in meeting the objective of their responsibility center.