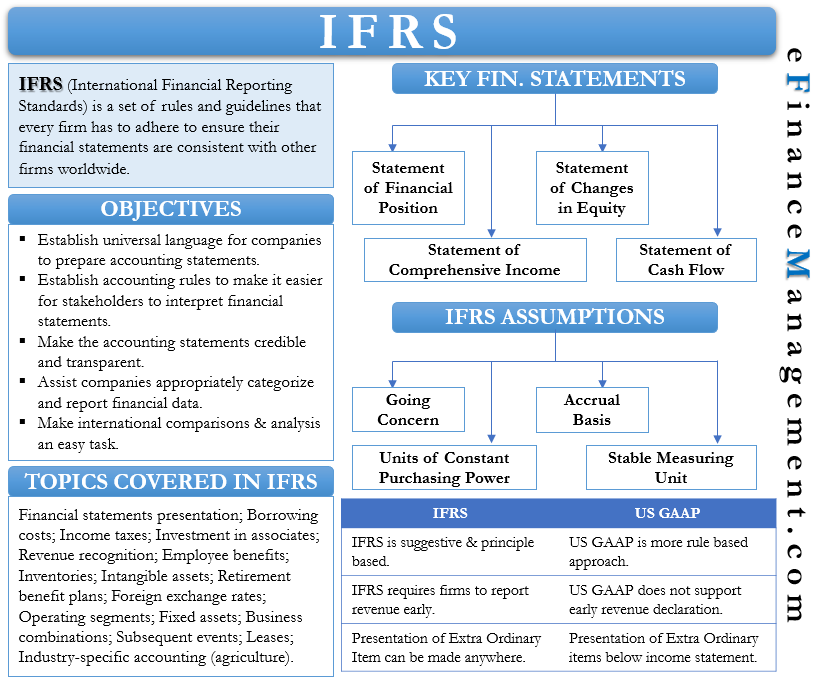

IFRS is the abbreviation for International Financial Reporting Standards. It is a set of rules and guidelines that every firm has to adhere to ensure their financial statements are consistent with other firms worldwide. These rules determine how a company should record a transaction in the accounting books, among other things. The use of IFRS helps to ensure the transparency and credibility of the accounting statements. And this, in turn, allows third parties to make decisions by going through these financial records.

IFRS mandates that all companies follow it uses the same rules and standards to prepare their financial statements. It means there is uniformity in the financial statements across firms, segments, and nations. And, in turn, it gets easier to evaluate the numbers of two or more companies. The benefit to the companies is that investors are more likely to trust and invest in companies that are transparent and follow standard accounting and disclosure norms.

IFRS History

Initially, the IFRS was known as IAS (International Accounting Standards), and it issued standards from 1973 to 2000. In 2001, when IASB (International Accounting Standards Board) took up the responsibility for developing new accounting standards, the name was changed to IFRS.

More than 100 countries currently follow these standards, including the EU, South America, and many Asian countries. However, few countries like the US and the UK follow their accounting standards known as GAAP (Generally Accepted Accounting Principles).

Also Read: GAAP vs IFRS – All You Need To Know

Objectives

The following are the objectives of IFRS:

- To establish a universal language for the companies to prepare the accounting statements.

- To establish accounting rules to make it easier for the stakeholders to interpret the financial statements, irrespective of the business location.

- Make the accounting statements credible and transparent.

- To assist companies in appropriately categorizing and reporting financial data.

- It makes international comparisons and analysis an easy task.

Topics Covered

IFRS has set rules and guidelines for a range of areas. These topics are – financial statements presentation; Borrowing costs; Income taxes; Investment in associates; Revenue recognition; Employee benefits; Inventories; Intangible assets; Retirement benefit plans; Foreign exchange rates; Operating segments; Fixed assets; Business combinations; Subsequent events; Leases; Industry-specific accounting (agriculture).

IFRS has also set mandatory rules for some business components of various key financial statements. In other words, it provides for what all should be part of those specific financial statements. And these are:

Statement of Financial Position

IFRS mandates the components of how to report and prepare the balance sheet.

Statement of Comprehensive Income

The statement of comprehensive income means preparing a statement of income. It could be one single statement for all income sources. Or, one can prepare it in several parts, such as a profit and loss statement, other income statements, and more.

Statement of Changes in Equity

Another name for this is the statement of retained earnings. Based on the inputs, It concludes any increase or decrease in the retained earnings during the period.

Also Read: Presentation of Financial Statements

Statement of Cash Flow

It categorizes all the cash transactions into Operations, Investing, and Financing.

Apart from these statements, entities following IFRS also need to provide an overview of their accounting policies. Also, a parent firm needs to prepare individual reports for every subsidiary.

IFRS Assumptions

All the rules, regulations, and guidance provided under IFRS are based upon four key accounting assumptions. And these assumptions are:

Going Concern

The first and foremost assumption is that the sole concept will guide all number crunching, evaluation, estimation, and recording that the business or the company will continue its activity. In other words, the business continues for the foreseeable future, and there is nothing like business is coming to an end.

Accrual Basis

This assumption implies that a business will recognize the impact of transactions as they occur and not when it results in cash inflow and outflow. In other words, a transaction happening or an event is essential rather than the exchange of money, which can occur in advance or later on.

Stable Measuring Unit

This assumption implies that all financial transactions and recordings will consistently happen in the common standard currency across accounting periods. It further directs that a company will record the assets and liabilities at their acquisition value or original cost.

Units of Constant Purchasing Power

This assumption implies a few exceptions to the stable measuring unit concept in certain situations, such as inflation or deflation.

IFRS and US GAAP

Even though both these accounting standards have similar objectives, there are many differences between the two.

1. The first and primary difference between the two is that IFRS is suggestive and principle-based. On the contrary, US GAAP is based on rules. Principle-based frameworks are flexible, while rule-based ones are more rigid.

2. Another difference is the treatment of revenue. IFRS requires firms to report revenue early. It could mean higher revenue in comparison to GAAP.

3. There is a difference in the treatment of some expenses as well. For instance, a company may not treat the spending on developing its business or for its future as an expense. The company can capitalize on it. However, as per GAAP, it is an expense, whereas, under IFRS, capitalization of such expenses is possible under certain circumstances.

4. Another difference is in the accounting of inventory. There are two popular methods to track and value inventory – first in first out (FIFO) and last in first out (LIFO). IFRS requires companies to use FIFO, but GAAP allows companies to use either of the two.

5. Moreover, there is a difference in the presentation of extraordinary items in the income statement. GAAP shows extraordinary items below the income statement; however, no such segregation is there in IFRS.

Read GAAP vs. IFRS in its detailed article.

Efforts to Integrate The Two Standards

Work is ongoing to reduce the variance between the GAAP and IFRS. Still, one expects some differences in the financial statements using these two accounting frameworks. The ultimate objective is to merge GAAP into IFRS, but it could take a long time to achieve this feat.

Once there is a merger of both guidelines, it would result in substantial cost savings and avoidance of duplicate efforts for the companies that do business in the US and other countries. Such companies won’t have to pay to get their financial statements to transform into other frameworks to meet the regulatory requirements.

Final Words

The primary objective of the IFRS is to make financial statements comparable across the globe. Even though it is the most popular accounting standard across the world, it is yet to achieve its objective fully. It is because of the presence of US GAAP and other accounting standards. Nevertheless, work is ongoing to consolidate accounting standards across the globe.

Quiz on IFRS

This quiz will help you to take a quick test of what you have read here.

Very informative Piece on the basics. Thank you.