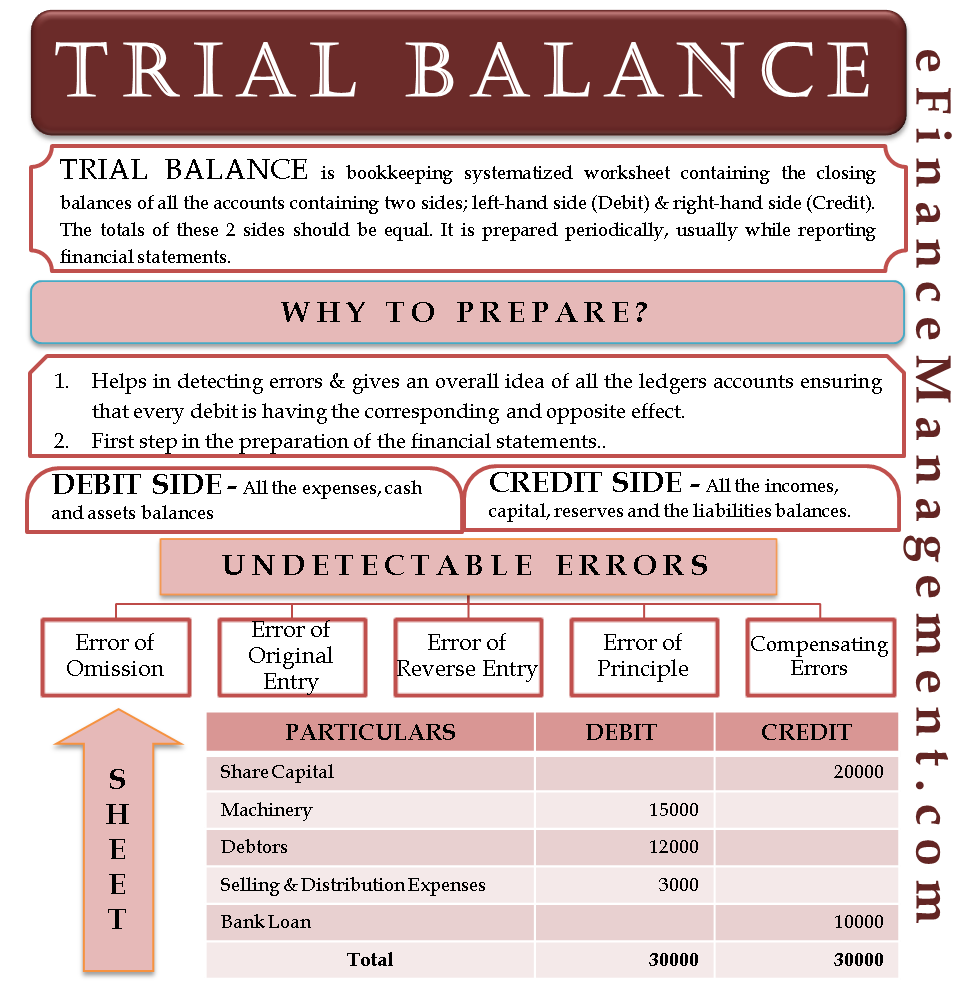

Trial Balance Meaning

The trial balance is a bookkeeping systematized worksheet containing the closing balances of all the accounts. There are two sides to it: the left-hand side (Debit) and the right-hand side (Credit). The totals of these two sides should be equal. It is prepared periodically, usually while reporting the financial statements. Generally, one doesn’t record the accounts having nil balances. If the total of the debit equals the total of the credit, it is considered balanced and error-free. However, even if it is tallied, there may be some errors not reflected. For example, one completely forgets to record a transaction that is material to record as per accounting, an error which set off with error, the error of principle, etc. A company also prepares a post-closing trial balance after passing the closing journal entries.

Why Prepare a Trial Balance?

- It helps in detecting the errors that are mathematically incorrect. Those incorrect errors may occur due to a single side effect of a transaction or any other such errors. Hence, one can detect the errors before preparing the financial statements.

- It is the first step in the preparation of the financial statements. The basis of the preparation of the financial statements (cash flow statement, income statement, and balance sheet) is the trial balance.

- It gives an overall idea of all the ledgers accounts, ensuring that every debit has the corresponding and opposite effect. Hence, ensuring accuracy in the double-entry system of accounting.

Debit and Credit Side

The debit side contains the expenses, cash, and assets balances, whereas the credit side contains the incomes, capital, reserves, and liabilities balances.

Read more about it at What is Debit and Credit.

Trial Balance Sheet

| Particulars | Debit | Credit |

| Share Capital | 20000 | |

| Machinery | 10000 | |

| Debtors | 1000 | |

| Selling and Distribution Expenses | 500 | |

| Drawings | 2000 | |

| Cost of Sales | 4000 | |

| Creditors | 8000 | |

| Cash | 10000 | |

| Furniture | 2500 | |

| Bank Loan | 2000 | |

| Total | 30000 | 30000 |

Also read Trial Balance vs Balance Sheet.

Undetectable Errors by the Trial Balance

When we do the totaling of the debit and the credit side, either the trial balance tallies or doesn’t tally. If it tallies, it ensures that there is an accuracy in the recordation of the transactions as per the double-entry system. This means there is a dual effect of all the transactions, and hence it is error-free. But there are many errors that it doesn’t detect, and hence, this is its limitation. Here we list out the errors the trial balance doesn’t detect.

Error of Omission

When somebody completely forgets to record a transaction or enter it into the books of accounts, the trial balance doesn’t affect it. The reason is that there is neither debit nor credit effect of the transaction, hence no problem of it getting tallied or not. It doesn’t tally when there are either of the effects (debit or credit). But since, due to the omission of the giving either of the effects, there is no interruption of the trial balance.

Error of Original Entry

When one enters the correct account, but with the wrong amount on both sides, the error is called the error of the original entry. Obviously, the same amount of debit and credit would not affect the trial balance as, again, there are two effects rather than one. One effect could not have tallied the trial balance, and hence, this error would not interrupt the totals of the trial balance.

Error of Reverse Entries

This error occurs when one enters the correct amount but on the wrong side, i.e., debit instead of credit, and vice versa. Since we affect both sides again, the trial balance will not show this error. Say a cash purchase of $250 should be purchase account debit and cash account credit. But say one wrongly affects the opposite side, i.e., debits the cash account and credits the purchase account. The same wouldn’t affect the trial balance.

Error of Principle

When one enters the correct amount and the correct side, but the principle is wrong, it wouldn’t affect the totals of both sides. Say, when one incurs expenses for the repairs of Machinery, the correct entry would be Repairs account debit to cash. But instead, somebody enters Machinery account debit to cash.

Compensating Errors

When an accounting error offsets another accounting error, these errors are called compensating errors. Compensating errors can be in the same or different accounting periods and in different accounts. These errors are difficult to detect. Which error offsets which error is not known, and hence, one can never detect such kinds of errors.