Tax Accounting is a branch of accounting. As the name suggests, it helps a firm not to prepare its financial statements but to prepare its tax return. This accounting includes methods and policies that help the company to arrive at a taxable profit.

The tax or the taxable profit figure using tax accounting could differ from the income that one gets using the usual accounting. And the primary reason for this is that the tax rules may delay or accelerate the recognition of certain expenses. Moreover, entities may use different methods to calculate taxable profit so as to reduce their tax liability. A point to note is that such differences are only temporary as all liabilities and assets eventually get settled.

Such accounting stems from the IRC (Internal Revenue Code) and not usual accounting frameworks, such as GAAP or IFRS.

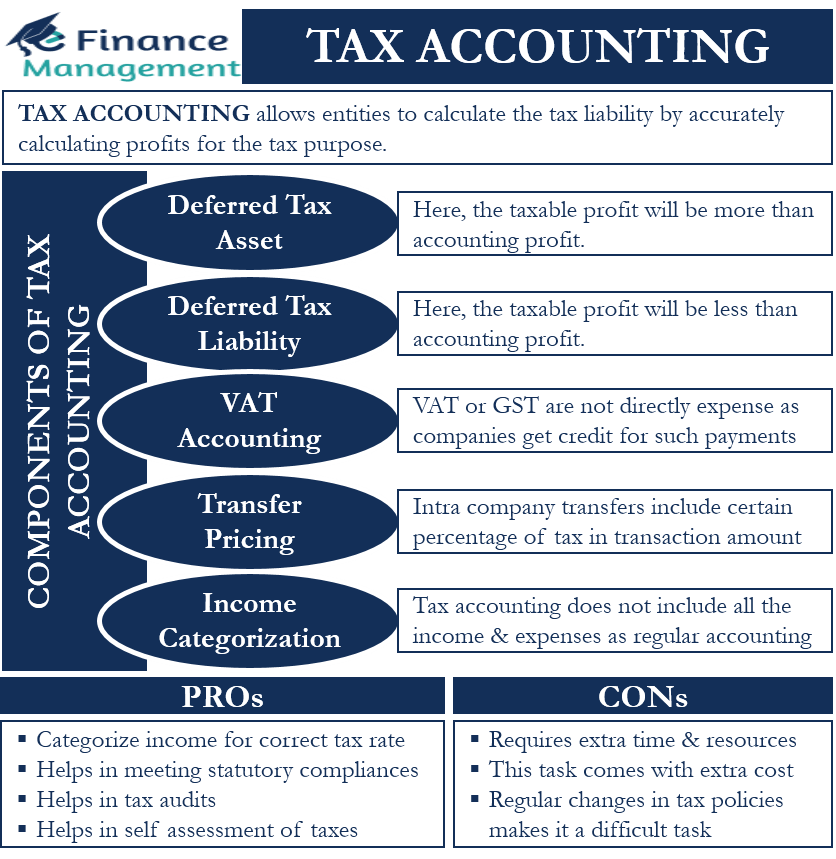

Components of Tax Accounting

There are certain items that result in a difference between the accounting and taxable profit. Some of those are detailed below:

Deferred Tax Asset

This component arises due to the timing issue when there is a difference between the book and taxable profit. For instance, provision for doubtful debt is treated as a deduction in the current year in usual accounting. But for taxation purposes, the provision for doubtful debt can only be allowed as a deduction if the amount is declared as bad debt, which may or may not happen in the current year.

Obviously, the taxable profit will differ in such a scenario. Instead, it will be more in the tax accounting than normal business accounting. The extra money that a business pays in taxes, due to the provision amount not being eligible for the deduction, will come under the deferred tax. This amount, however, will be realized in future years when the expense will be treated as deductible.

Also Read: Branches of Accounting

Deferred Tax Liability

This liability arises when the taxable profit is less than the accounting profit in the current year because of the timing difference. For example, a company is depreciating its assets using the straight-line method, and the depreciation amount comes at $1,000 a year. But, for the purpose of taxation, the company has to use WDV (Written Down Value method). The second method gives a depreciation of $1,500 in the first year. In this case, the company will get more deductions in the first year and thus, will have to pay lesser taxes. The amount of lesser taxes the entity pays is what we call deferred tax liability. However, in the later years, the depreciation under the WDV method will be less than the straight-line method. So the tax liability will eventually settle.

VAT Accounting

VAT (Value Added Tax) or GST (Good & Service Tax) is not directly an expense. This is because companies get a tax credit for the amount they have already paid. However, to claim such a credit, the companies need to follow a specific procedure regarding invoicing, registration, and more.

Transfer Pricing

In the current era of globalization, many companies open and operate facilities in different countries. There remains an exchange of goods and services amongst these units or facilities. Hence, such transactions attract the transfer pricing concept. The idea behind such pricing is that the related entity must not get the product or service at a lower cost than if the same product or service is sold to an unrelated third party. For instance, a company that operates an offshore office has to pay a certain percentage of tax on the expenses they incur in operating that office.

Income Categorization

In normal accounting, we consider all the receipts and payments for coming up with the profit. But not all receipts and payments come into the calculation for tax purposes.

On the basis of the above components, we can say that the tax accounting involves the following:

- Creating the tax liability for a tax payable or creating a tax asset for the current or future years.

- Creating a deferred tax liability or asset for attributing the temporary differences between the accounting and taxable profit.

- Using the above tax liabilities and assets to come up with the income tax expense for a period.

Pros and Cons of Tax Accounting

Below are the pros of tax accounting:

- This accounting helps to categorize the income for applying the correct tax rate.

- It helps the company to meet statutory requirements.

- This accounting helps offset the current and prior year losses in future years by filing tax returns.

- It helps with tax audits.

- It helps entities to self-assess and pay their taxes timely.

Below are the cons of tax accounting:

- A company needs to devote extra time and resources to carry out such accounting.

- Performing this accounting comes with extra cost.

- Tax policies change regularly, and this could make it difficult to meet statutory requirements.

- One can not do away with normal accounting. That, in any case, will need to be prepared, maintained, and reported as per the governing law and process of the country.

Final Words

Tax accounting is very crucial for all types of entities, including sole proprietorships, partnerships, individuals, corporations, and even non-profits. This is because it allows them to calculate their profit accurately for tax purposes. However, it is very important for the entities to stay up-to-date with the changing tax policies. If possible, entities can take the help of tax professionals to ensure they don’t miss anything.