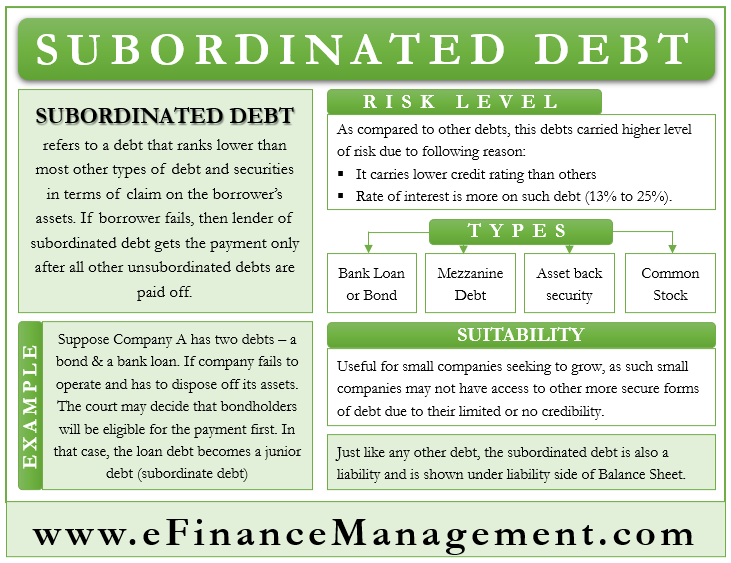

Subordinated debt is a debt that ranks lower than most other types of debt and securities in terms of claims on the borrower’s assets. In simple words, we can say that if a borrower defaults, the lender of the subordinated debt will get the payment only after the payment is made to all other debt holders. We can also call it a junior debt, subordinated bond, or subordinated debenture. It is the opposite of unsubordinated debt.

After a company or a person files for bankruptcy, it is up to the court to decide the ranking of the debts. A debt that a court decides is not a priority will be subordinated debt. The assets of the bankrupt company will first be used to repay the unsubordinated debt. Then any funds left after paying the unsubordinated debt will go towards paying the junior debt. Thus, it is possible that lenders of such debt receive partial payment or no payment at all.

Risk Level in Subordinated Debt

A junior debt can either be secure or unsecured. It carries a lower credit rating than most other types of debt. It means the rate of interest would be more on such a debt. Generally, such a debt comes with an interest rate of 13% to 25%. It may also come with additional benefits so as to compensate the lender for the higher risk.

Because of its payment rank, this debt is riskier than other types of debt. The risk in debt is inversely proportional to the ranking of the debt. This means that the debt gets riskier if its rank lowers, or the risk reduces if the ranking improves. Thus, it is very important that creditors properly evaluate the creditworthiness of the borrower before extending the debt.

Example of Subordinated Debt

Company A has two types of debt. The first is a bond worth $5 million maturing after 5 years, and the other is a loan from a financial company of $1 million due after four years. Because of the coronavirus pandemic, Company A fails to operate and had to dispose of all its assets. The court decides that the bondholders will be eligible for the payment first. And the loan from the financial company will be paid after that because it is a junior debt.

Types of Subordinated Debt

Following are the types of junior debt:

Bank Loan or Bond

A bond issued by a bank could be junior debt. Unlike expectations, subordinated debt is very popular in the banking industry. It is a smart option for the banks because interest payments are tax-deductible. A study in 1999 found that banks issue such a debt to improve their risk level. Banks, however, generally offer such a loan to big corporations and only after evaluating their cash flows and creditability.

Mezzanine Debt

Mezzanine debt is also an example of junior debt. This debt ranks higher only to the common shares of stock at the time of the payment. It is a hybrid debt.

Asset-backed Security

An asset-backed security is also a type of junior debt. A lender issues such a debt in tranches or portions. The senior tranches rank high in terms of payment. An example of an asset-backed security is a mortgage-backed security.

Common Stock

Common stock is another example of junior debt. Preference shares rank higher than the common stock, while debentures rank higher than preference shares.

Whom It Useful To?

Though riskier, such a type of debt could prove very useful for small companies seeking to grow. Since these companies are new and without much credibility, they don’t get access to other, more secure forms of debt. However, lenders may be willing to offer them loans but at a higher interest rate being, carrying a higher risk. Thus, such a loan provides a small company with a chance to boost its operations.

The company taking such a loan should have consistent cash flows or be capable of serving such a debt. Also, such a loan helps a company to save their equity for a future sale or keep it making payments to the employees.

A junior debt may also cost less than the equity investments from outside sources. Thus, many businesses prefer such a debt than seeking equity investment.

Limit to Loan

Even though a junior debt is useful for some companies, there is a limit to which a company can take such a debt. Taking too much of such debt may make it difficult for a company to service the debt and, at times, sustain its operations as well. There are no fixed rules to determine how much debt is enough. But, there are some measures that may give a signal about the rising debt level. These measures are:

- Suppose a company’s total debt to EBITDA ratio is 5 to 6 times. Generally, a senior debt makes up 2 to 3 times of debt to EBITDA. Thus, the remaining space is for the junior debt.

- If the EBITDA to cash interest is around 2 times, then the company should take it as a warning sign.

- If the minimum equity funding hits a 30%-35% level, it is also a warning sign of high debt.

Senior Debt vs. Subordinated Debt

If a company liquidates its assets to pay the debt, the debt that is first in line to get the payment is the senior debt. The debt that ranks lower in terms of payment priority is the junior debt.

Since junior debt ranks lower, they are riskier than senior debt. Generally, senior debt is secure, while junior debt may or may not be secured. Because they are riskier for the lender, a junior debt carries more interest rate than senior debt.

Accounting of Subordinated Debt

Like any other debt, a junior debt is also a liability for the borrower. Therefore, like other debts and liabilities, the subordinated debt will also be listed on the liabilities side of the balance sheet. In the liabilities, the current liabilities come first, then comes senior or unsubordinated debt under the long-term loans. After this, we show the junior debt on the balance sheet. When someone gets a junior debt, their cash account increases. The loan account also goes up for the same amount.

Final Words

Subordinated debts are very risky, and that is why big companies try to avoid them. However, they are an important source of finance for smaller, lesser-known companies. For the lenders also, it offers an attractive return, but it is important that they evaluate and continuously monitor the creditworthiness of the borrowers.

EXPLANATION IN A VERY SIMPLE WAY. EXCELLENT ARTICLE