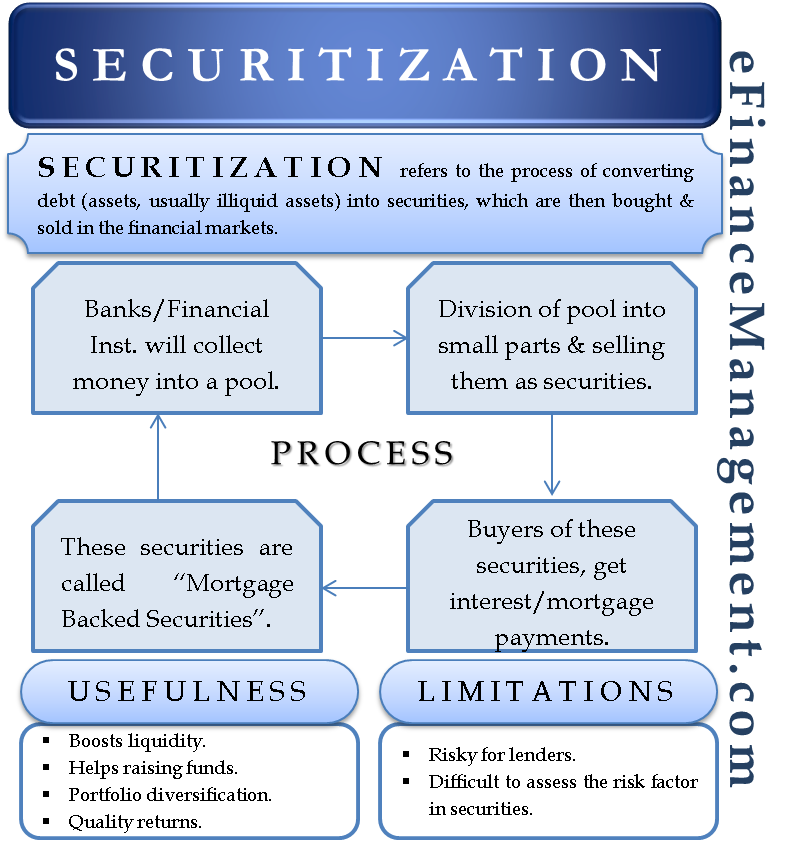

Securitization refers to the process of converting debt (assets, usually illiquid assets) into securities, which are then bought and sold in the financial markets. If you notice, the first line calls debt an asset. This is because debt is a liability for the borrower, but it is an asset for the lender. One can trade securities (created from securitization) similar to stocks, bonds, and futures contracts.

In simple words, securitization is a process where a financial company combines several of its assets into consolidated financial instruments or securities. Then, financial companies issue these securities to the investors, who earn interest.

We also know such securities by the name asset-backed security (ABS), or collateralized debt obligation (CDO), or also mortgage-backed securities (MBS). ABS usually pools different assets like a credit card, auto loans, and more, while MBS pools mortgage only.

What’s the Process of Securitization?

As said before, banks or financial institutions securitize primarily illiquid assets. One can easily convert a liquid asset into cash, for example, gold. On the other hand, assets that can’t be easily converted to cash are illiquid assets. Real estate is a good example of it. Finding a buyer for a property is not always an easy task.

Also Read: Asset Backed Securities

Similarly, mortgages are valuable assets but are mostly illiquid. Mortgages are usually backed by real estate, which again is illiquid. Though mortgages offer a healthy return in the form of the homeowner paying interest, it can take many years (as long as 30 years) to realize it in full. Thus, to realize the full potential of these illiquid assets, banks or financial institutions covert mortgages into liquid assets via securitization.

A question that arises now is how the bank or other financial institutions securitize an asset.

First, a bank or financial institution collects thousands of mortgages into a “pool.” Then, it divides those pools into small parts and sells them as securities. Buyers of these securities get the right to the interest or mortgage payments by the homeowners. Since mortgages back these securities, they are also called “mortgage-backed securities.”

How does Securitization Help?

Securitization helps in boosting liquidity in the market. Moreover, it helps financial companies to raise funds. If a company has already exhausted its funds by giving loans but wants to provide more loans, then it can use securitization to raise more funds. Such a company can club its assets in the form of a financial instrument and then issue them to the investors. So, the process helps the companies to raise funds and give more loans.

For the investors, such instruments help them diversify their portfolios and earn quality returns.

Such security has no almost effect on the borrower, whose mortgage has been pooled. All the terms – agreed between the lender and the borrower – remain intact at the time of taking the loan. A possible change could be that the borrower may be asked to send interest payments to a different address.

Also Read: Secured Loans

Is it Safe?

Such securities are a safe bet as long as the homeowners, whose mortgages were pooled, make their interest payments on time. But, this is not always the case. The 2008 financial crisis is a good example of it.

One disadvantage of securitization is that it may encourage lenders to loan money to high-risk people. This is because, after the securitization, the lender has no money at stake as the risk transfers to the investors.

A similar thing happened in the 2008 housing bubble. Owing to unwise lending by the banks and financial institutions, a record number of homeowners started defaulting. Due to this, the mortgage back securities lost their value.

Following the crisis, the US central bank had to step in to ensure liquidity in the financial markets. The bank, at the time, started buying such securities from the investors through quantitative easing (QE) operations.

Another disadvantage of such securities is that it becomes difficult for the investor to assess the risk in the security. Since ABS consists of many debt instruments, like mortgages, credit card debt, auto loans, and more, it can sometimes make it hard for the investor to evaluate the risk properly.

Thank you, for making it simpler

Well explained,

Thank you.