What is Peer-to-peer Lending?

Peer-to-peer lending (P2P) is a relatively new form of debt financing. It is a type of crowd-funding that addresses the needs of both – people who want loans and those who want to invest. P2P allows people to borrow and lend money without the help of an official financial institution. So, it eliminates the middleman from the process, thus leading to lower costs. This article will address both advantages and disadvantages of peer-to-peer lending.

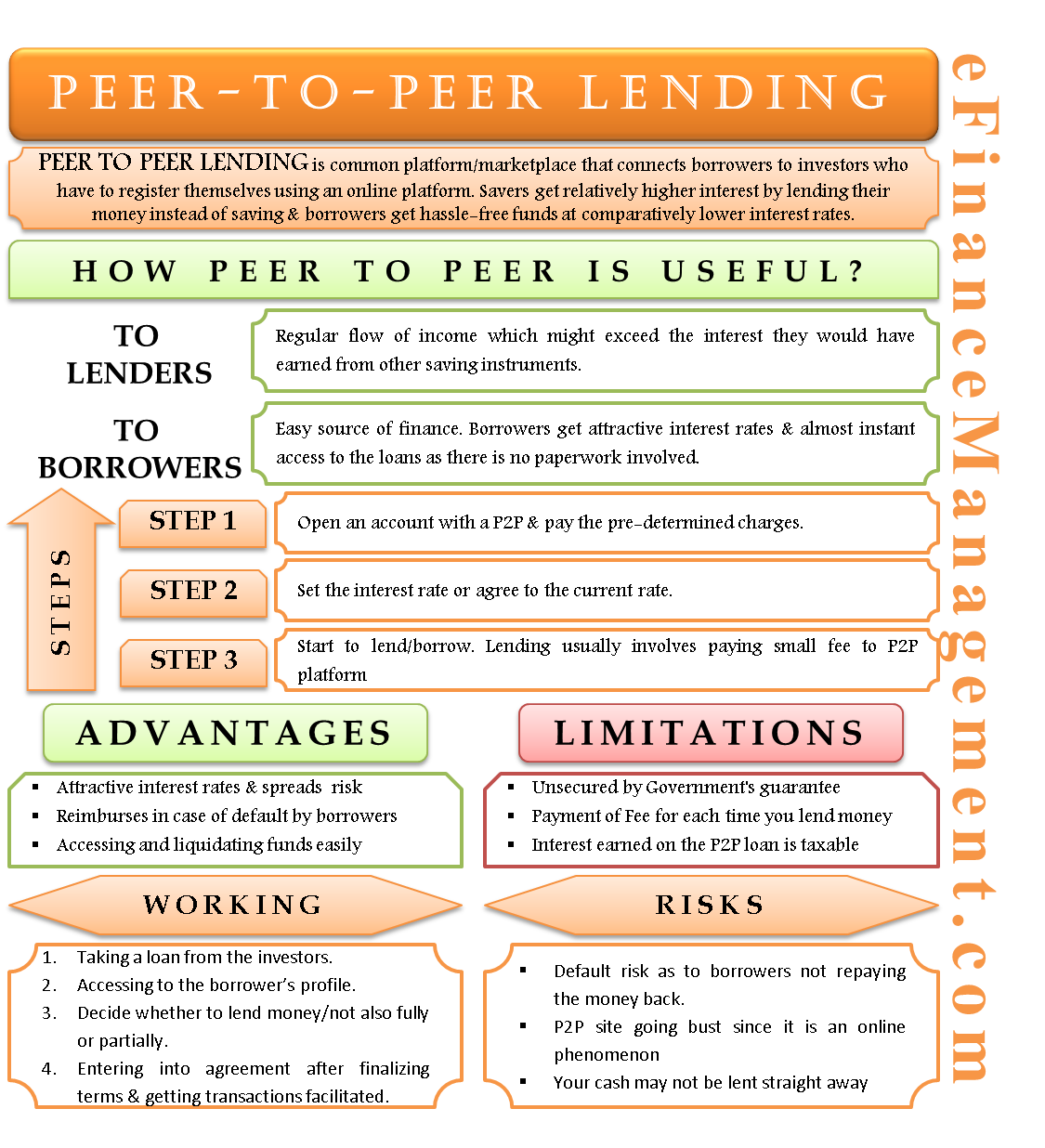

A common platform or marketplace that connects these borrowers to investors is called a P2P platform. Normally, peer-to-peer lending uses an online platform, where lenders and borrowers have to register themselves. The concept behind P2P lending is that savers get relatively higher interest by lending their money instead of saving. And, borrowers get hassle-free funds at comparatively lower interest rates in comparison to the market.

How to Get Started with P2P Lending?

There are mainly three steps to start with P2P lending;

- At first, you will have to open an account with a P2P and pay the pre-determined charges.

- Then you have to set the interest rate or agree to the current rate.

- And, finally, you can now start to lend or borrow. Lending usually involves paying a small fee to the P2P platform (like 1% of the loan amount).

Peer-to-peer lending is a relatively new form of finance that hasn’t been tested over the long term. So, some unexpected issues might crop up at any time. Investors, therefore, are advised not to put all their assets into the P2P model. Also, they must carry out extensive research while selecting the best P2P platform and the borrower.

Advantages of Peer-to-peer Lending

The following are the reasons to answer the question – “Why P2P Lending?”

- P2P lending ensures a regular flow of income for a lender which exceeds the interest they would have earned from other saving instruments, like fixed deposits, recurring deposits, and more. This provides opportunities for lenders to earn attractive interest rates.

- For borrowers, P2P lending is an easy source of finance. Borrowers get attractive interest rates and almost instant access to the loans as there is no paperwork involved.

- P2P platforms help you spread your risk by allocating capital to multiple loans.

- If borrowers default, most P2P platform assists with legal actions and even reimburses lenders.

- Many P2P platforms allow you to liquidate your funds even before the end of the term. This helps you, in case you have some urgent requirements for money.

Disadvantages of Peer-to-Peer Lending

Peer-to-peer lending can be risky, and thus, it is very important that lenders understand the risks associated with it.

Default Risk

Unlike traditional saving, the money in P2P lending is not secured by a government guarantee. There are always chances that the person to whom you are lending fails to repay. It must be noted that the money lent via a P2P platform is usually not covered under any law. However, many P2P platforms maintain contingency or provision funds to pay the lender if a borrower defaults. Also, some platforms help the lender initiate legal actions against the defaulting borrower.

Also Read: Advantages and Disadvantages of Bank Loans

P2P Site Going Bust

Since P2P is mostly an online phenomenon, there is always a chance of the platform going out of business. In such a case, you may lose all your money. However, many countries have regulations in place to force the platform to keep lenders’ money separate from their own money.

Your Cash may not be Lent Straight Away

You are not entitled to any interest on the cash waiting to be lent out. To avoid such a scenario, you must go for easy terms to attract borrowers. Also, interest earned on the P2P loan is taxable. But, you can consult a tax expert to help you lower your tax liability.

Fees Charged by P2P Platform

You will need to pay a fee to the P2P platform each time you lend the money.

How does Peer-to-Peer Lending Work?

In the traditional banking system, people who need loans approach banks. The bank then carries financial checks on the applicant’s credit history and, if satisfied, extends the loan after extensive paperwork. However, those with poor credit history may not qualify for a bank loan. Even if they qualify, the bank will charge a higher interest rate.

To avoid such higher interest rates and get a loan easily, such borrowers may go for peer-to-peer lending. In P2P, borrowers take a loan from investors who are ready to lend at an agreed interest rate. Lenders have access to the borrower’s profile on the P2P platform. This helps them to decide if they want to lend money to a particular borrower or not.

Also Read: Sources of Credit

Further, it is up to the lender to loan the full amount or only a portion of the asked amount. If a borrower gets a partial loan, they may approach another lender on the platform for the balance amount.

Borrowers and lenders enter into an agreement after finalizing the loan amount, interest rate, and repayment terms. P2P platforms facilitate the transactions but are not responsible for the default beyond their policies.

Great piece of information over here.

In my opinion, Peer to peer lending, also known as P2P lending, is a technology enabled system where individual investors fund loans to individual borrowers. Also called marketplace lending, peer-to-peer lending is a growing alternative to traditional lending.