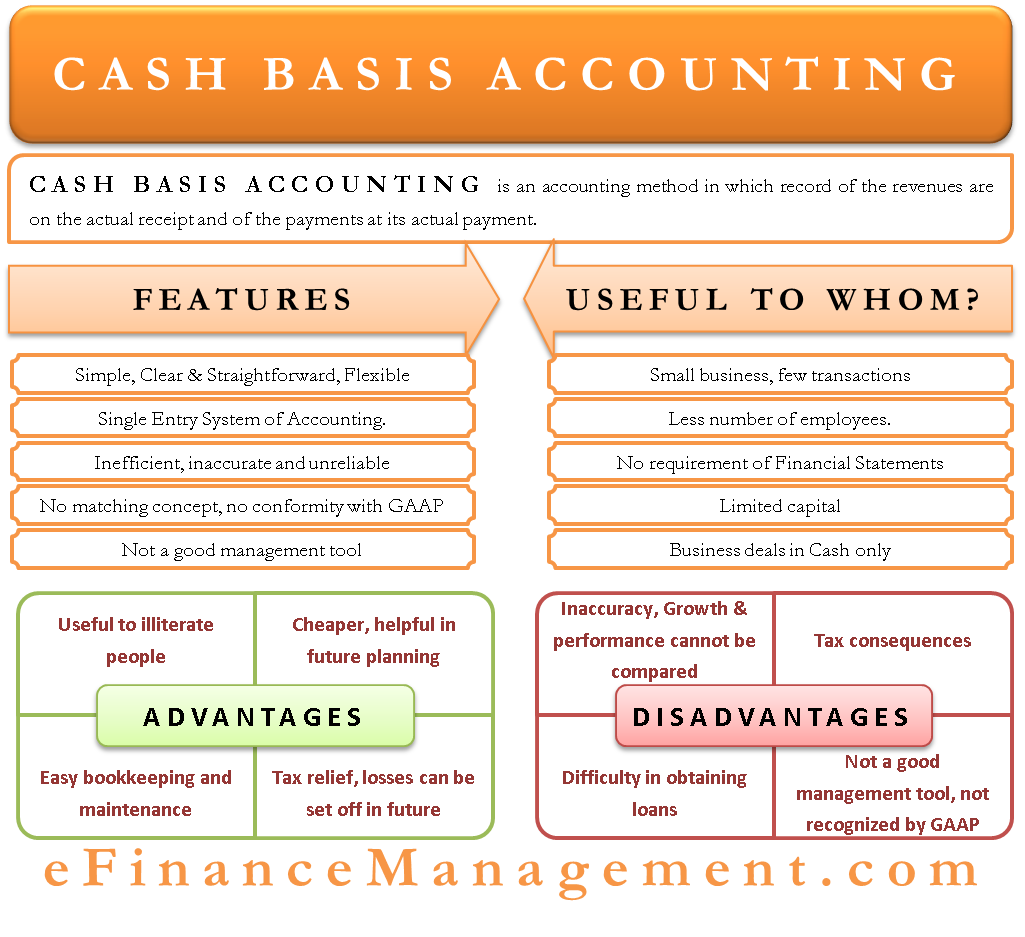

What is Cash Basis Accounting?

Cash basis accounting is an accounting method in which records of the revenues are on its actual receipt and of the payments on its actual payment. There are two forms of accounting, namely, Cash and Accrual.

Features of Cash Basis Accounting

- Simple, clear, and straightforward as accounting adjustments at the end of the year are not to be made.

- This method is flexible as one has the option of switching from Cash to an Accrual basis of accounting and vice versa.

- It follows the Single Entry System of Accounting.

- Not as efficient, accurate, and reliable as Accrual Basis of Accounting.

- No concept of matching revenues and expenses.

- It is not a good management tool as there is a time gap between the actual happening of the transaction and its actual receipt or payment (results).

- It doesn’t conform to the GAAP Provisions.

Example of Cash Basis Accounting

Donald follows the cash system of accounting. He is a small businessman dealing in the trade of Plastics. He has sold plastic containers to a customer and made an Invoice of $2000 on 26/10/18 (Friday). But, he has not received the payment on the same day. He received the payment of it on 29/10/18 (Monday). So, since he follows cash basis accounting, the invoice date is irrelevant. Hence, he recognizes this revenue in his books of accounts on 29/10/18.

Take another example of an expense. Say Donald is to pay $7000 for the salary to his employee. The due date of the salary is the 7th of the next month. But he couldn’t pay on that day. He paid for the salary on the 15th of the next month. Hence, the cash outflow is on the 15th, so expense recognition is also on the 15th only.

Cash Basis Accounting- Suitable to Whom?

- The one who has a very small business dealing with very few transactions.

- When one has a very less number of employees.

- When there is no requirement of any such record of Income Statement, Trial Balance, or Balance Sheet.

- A person has very limited capital.

- The business transactions are mostly in Cash.

Advantages of Cash Basis Accounting

- This system does not require expert accounting knowledge. It is just based on the actual receipt and actual payment of cash. So, small businesses and sole proprietors can easily record and maintain their transactions in a small notebook without preparing a separate set of systematic books.

- This is definitely cheaper than the accrual system of accounting. The reason is that the accrual system follows the double-entry system of accounting, which records each and every transaction in a systematic way. Therefore, the double-entry system requires software for efficient recording. There is no requirement for voluminous records and thereby software in a single entry system, and hence it is cheaper.

- Since it is simple and requires recording less no. of transactions compared to the accrual system, it is less time-consuming.

Disadvantages of Cash Basis Accounting

- Some lenders may require the accounts preparation as per the GAAP provisions and hence, would refuse to lend money.

- If the company wants to approve Audited Financial Statements, the accounts prepared under the cash basis of accounting are not considered.

- If one switches every year from accrual to cash basis accounting and vice versa, there will be a lot of burden on the administrator. He will have to keep calculating as to whether which income or expense is of which date? Say, in accrual accounting, income recognition is on the occurrence and not on its receipt. So, again this will increase the profits in one year, hence not showing accurate profits. Correspondingly, in the case of expenses as well.

- The Companies Act doesn’t consider this system.

- There is no requirement to maintain the books of the assets and liabilities. So, if one doesn’t take care of their assets, they might get misplaced or stolen.

- There are chances of discrepancies as one can show more expenses and less income involving unfair trade practices.

Difference Between Cash and Accrual Basis Accounting

| Points of Difference | Cash Basis Accounting | Accrual Basis Accounting |

| Record | Cash actually received or paid | Cash to be received or owed |

| Nature and Preparation | Easy | Complex |

| Preferable for | Small Businesses | Large Businesses |

| Type | Incomplete | Complete |

| Suitable for Taxation | No | Yes |

Read Difference between Cash Vs. Accrual Accounting for a more detailed article.

Wish you all the best