There are several ways to find out the worth of a stock, such as DCF (Discounted Cash Flow), PE Ratio, and more. There is one more (not so popular) method to get the value of a stock, and it is the Dividend Discount Model (DDM), a quantitative technique. This method assumes that the value of the stock (intrinsic value) is the discounted value or the net present value of the sum of all the future dividends that a firm would pay or expects to pay. The Dividend Discount Models are of three types – Constant Growth or Garden Growth Model, Variable Growth (Two-Stage and Three Stage), and Zero Growth models.

In this article, we will be discussing the Zero Growth Dividend Discount Model.

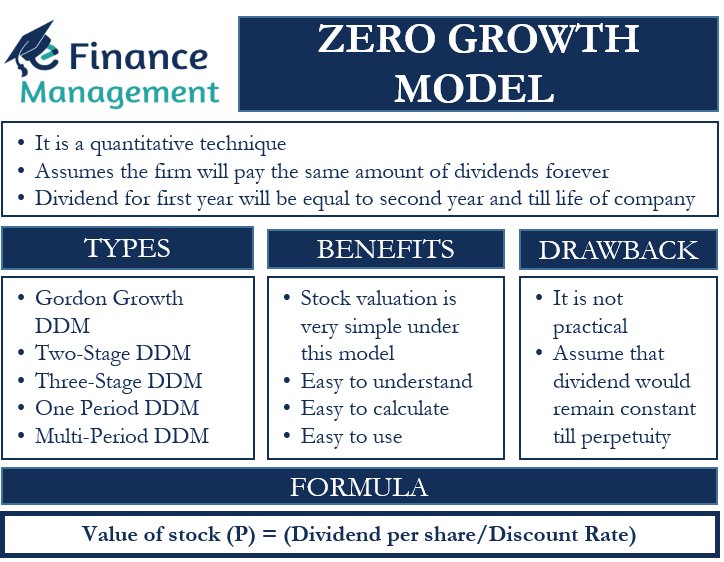

What is Zero Growth Model?

As the word suggests, this model assumes that the firm will pay the same amount of dividends forever. This implies that there will be zero or no growth in the dividend amount, and hence, named Zero Growth Model.

So, the dividend for the first year will be equal to the second year, the third year, up till the life of the company. The stock valuation is very simple under this model. The annual dividend is divided by the required rate of return, and the result is the stock value.

The primary benefit of this method is that it is easy to understand, calculate and use. And the biggest drawback of this model is that it is not practical. This is because if a firm grows bigger, then investors would expect the firm to give more dividends per share. Also, it is unreal to assume that the dividend would remain constant till perpetuity. There are several reasons why constant dividends may not be possible and feasible – need more funds for an excellent business opportunity, tax considerations may suggest skipping or lowering the quantum of dividends in a particular year, cash flow issue, business loss in a year, etc.

Also Read: Cost of Equity – Dividend Discount Model

Zero Growth Model – How to Calculate?

The formula to get the value of the stock using the Zero Growth dividend discount model is:

Value of stock (P) = (Dividend per share / Discount Rate) or (Div /r)

A point to note is that we use the same formula to calculate the value of perpetuity or a bond that never matures. We can also use this formula to get the value of the preferred stock, which usually pays a certain percentage of its par value as a dividend.

Let us better understand the calculation of a stock value using the Zero Growth Model through the following example.

Company A pays a dividend of $1.20 annually and expects to pay the same dividend till perpetuity. Moreover, Company B expects the required rate of return to be 7%.

Putting the values in the formula above to get the intrinsic value of Company A’s stock:

Intrinsic Value = $1.20 / 7%

= $17.14

Other Dividend Discount Models

There are a few more variants of Dividend Discount Models. We will discuss those models:

Gordon Growth DDM – It considers a perpetual dividend growth rate that remains the same throughout the forecasting period. Another name for this method is the constant growth DDM.

Two-Stage DDM – This method splits the forecast period into two periods. In the first period, it assumes an increasing growth in dividends, and in the second stage, it assumes a stable dividend growth.

Three-Stage DDM – This method splits the forecast into three periods. Along with the increasing and constant dividend growth, this method also considers a declining growth rate over time.

One Period DDM – This is rarely used. Here it is assumed that the investor is interested only to hold the stock for that one period, usually one year. Hence, he would like to know the intrinsic value of the stock for that period only. Because of one period holding, only one-period dividend expectation is taken into consideration.

Multi-Period DDM – This is the opposite of One-period DDM. Here the investor is willing to hold the stock for multi-year. The main problem in this model is the assumption of dividend flow over the multi-year.

Final Words

Zero Growth Model is the easiest and simplest way to determine the worth of stock. However, it is not popular among analysts because it is not practical. And it is very rare to find such stock in the actual world. Because in general, the expectations of investors will grow with the growth of the company, and they expect a growing dividend quantum over the years. Still, this method helps to give a rough idea of a company’s stock value.