The value of money can be expressed as the present value (discounted) or future value (compounded). These both are the concepts of the time value of money. A $100 invested in a bank @ 10% interest rate for 1 year becomes $110 after a year. From the example, $110 is the future value of $100 after 1 year, and similarly, $100 is the present value of $110 to be received after 1 year. They are just reciprocal of each other.

Future Value

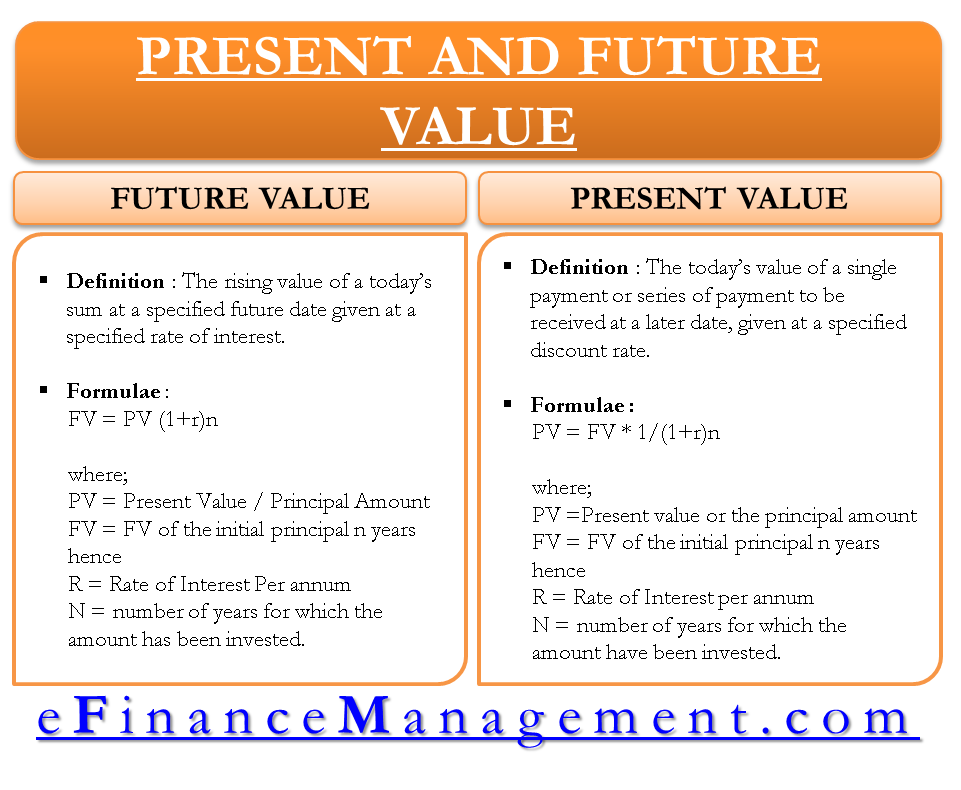

Definition of Future (or Compounded) Value

It can be defined as the rising value of today’s sum at a specified future date given at a specified interest rate. The compounding technique calculates it.

Future Value Example with Compounding of Money

Compounding of money is the value addition in the initial principal amount after defined intervals at a given interest rate. For example, if Mr. A invests $1,000 for say 3 years @ 10% interest rate compounding annually, then the income will rise as follows:

| First Year: | Principal at the beginning | 1,000.00 |

| Interest for one year (1000*0.10) | 100 | |

| Principal at the end | 1,100.00 | |

| Second Year: | Principal at the beginning | 1,100.00 |

| Interest for the year (1100*0.10) | 110 | |

| Principal at the end | 1,210.00 | |

| Third Year: | Principal at the beginning | 1,210.00 |

| Interest for the year (1210*0.10) | 121 | |

| Principal at the end | 1,331.00 | |

This calculation process is known as compounding, and the sum arrived at after compounding the initial amount is known as Future Value. In our example, the future value of $1000 is $1331 after 3 years @ 10% interest rate compounding annually. Similarly, a present value of $1331 is $1000 under the same conditions.

Future Value Formula and its Explanation

This was a very simple example. In practical use, there can be 20 years in place of just 3 and more frequent compounding than annual. Following the formula helps determine the future value of any sum very easily.

FV = PV (1+r)n

Where,

PV = Present value or the principal amount

FV = FV of the initial principal n years hence

r = Rate of Interest per annum

n = a number of years for which the amount has been invested.

In this equation, (1+r)n is the compounding factor that calculates the principal amount along with interest and interest on interest. It is called the “Future Value Interest Factor.”

Now, if we solve the above example with the given formula, we get

=1000(1+0.10)3 = Rs. 1,331/-

The formula is helpful to calculate the amount invested for longer maturity periods, say 10-20 years, very quickly and easily.

For calculation, you can use FVIF Calculator

Multiple Compounding Periods

The compounding period refers to the no. of years/months for which the interest is made due. These can be monthly, quarterly, half-yearly and annually, etc. For example, if the interest is charged on a monthly basis, then the annual interest rate ‘r’ shall be divided by 12, and no. of years’ n’ shall be multiplied by 12. So, when the frequency of compounding is more, the effective interest amount is also more.

Rule of 72 Trick

There are a general question in an investor’s mind How many years will it take to double my money? ‘Rule of 72‘ is a user-friendly mathematical rule used to quickly estimate the ‘rate of interest’ required to double your money given the ‘number of years of investment and vice versa. It is specifically called the rule of 72 because the number 72 is used in its formula.

Formula for Rule of 72

For calculating the number of years required to double your money given the rate of interest, the formula is:

Number of years = 72 / Interest

Example: At 8%, money takes 72/8 or 9 years to double it.

Or

For calculating the rate of interest required to double your money given the number of years of investment, the formula is:

Rate of Interest = 72 / Number of years

For example, a 10-year investment requires a 72/10 or 7.2% rate of interest p.a. to double itself.

Present Value

Definition of Present (or Discounted) Value

It can be defined as today’s value of a single payment or series of payments to be received at a later date, given at a specified discount rate. The process of determining the present value of a future payment or a series of payments or receipts is known as discounting.

Present Value Example with Discounting of Money

In absolute terms, discounting is the opposite of compounding. It is a process for calculating the value of money specified at a future date in today’s terms. The interest rate for converting the value of money specified at a future date in today’s terms is known as the discount rate.

We will take a reverse example of future value as explained above. Mr. A has an offer to get $1331 after 3 years if he pays $975 today. A market interest rate is 10% with annual compounding. What should Mr. A do? To pay $ 975 or not. To decide whether he should pay $975 or not, he should be able to compare his proposed outflow of today with today’s value of $1331 to be received after 3 years. Referring to the table above, we know that the present value of $1331 after 3 years is $1000. So, Mr. A should definitely pay $975 because there is a clear-cut benefit of $25 over and above the interest earnings.

This calculation process of present value is known as discounting, and the sum arrived at after discounting a future amount is known as Present Value.

Present Value Formula and its Explanation

The formula to calculate the present value is as follows:

PV = FV / (1+r)n

Or

PV = FV * 1/(1+r)n

Where,

PV=Present value or the principal amount

FV= FV of the initial principal n years hence

r= Rate of Interest per annum

n= number of years for which the amount has been invested.

In this equation, ‘1/(1+r)n‘ is the discounting factor which is called the “Present Value Interest Factor.”

Our current example can be easily solved with the formula –

PV = FV * 1/(1+r)n

PV = 1331 * 1/(1+10%)3

PV = 1331 * 1/(1+0.10)3

PV = 1331/1.13

PV = 1331/1.331

PV = 1000

Also read – Present Value of Annuity

Present Value vs. Future Value: Interest Factors (PVIF) and (FVIF) Tables

PVIF and FVIF tables are available to facilitate the ease of calculations. Following is an example of an FVIF table with various periods and percentages of interest. For example, in our case, we have to look for r =10 and n= 3; the value is 1.331. From this only, we can find PVIF by dividing it by 1, 0.751 (1/1.331), or a separate table is also available.

| FVIF | Rate of Interest (r) | ||||||

| Period (n) | 1% | 2% | 3% | 4% | 5% | 6% | 7% |

| 1 | 1.010 | 1.020 | 1.030 | 1.040 | 1.050 | 1.060 | 1.070 |

| 2 | 1.020 | 1.040 | 1.061 | 1.082 | 1.103 | 1.124 | 1.145 |

| 3 | 1.030 | 1.061 | 1.093 | 1.125 | 1.158 | 1.191 | 1.225 |

| 4 | 1.041 | 1.082 | 1.126 | 1.170 | 1.216 | 1.262 | 1.311 |

| 5 | 1.051 | 1.104 | 1.159 | 1.217 | 1.276 | 1.338 | 1.403 |

| 6 | 1.062 | 1.126 | 1.194 | 1.265 | 1.340 | 1.419 | 1.501 |

| 7 | 1.072 | 1.149 | 1.230 | 1.316 | 1.407 | 1.504 | 1.606 |

| PVIF | Rate of Interest (r) | ||||||

| Period (n) | 1% | 2% | 3% | 4% | 5% | 6% | 7% |

| 1 | 0.99 | 0.98 | 0.971 | 0.962 | 0.952 | 0.943 | 0.935 |

| 2 | 0.98 | 0.961 | 0.943 | 0.925 | 0.907 | 0.89 | 0.873 |

| 3 | 0.971 | 0.942 | 0.915 | 0.889 | 0.864 | 0.84 | 0.816 |

| 4 | 0.961 | 0.924 | 0.888 | 0.855 | 0.823 | 0.792 | 0.763 |

| 5 | 0.951 | 0.906 | 0.863 | 0.822 | 0.784 | 0.747 | 0.713 |

| 6 | 0.942 | 0.888 | 0.837 | 0.79 | 0.746 | 0.705 | 0.666 |

| 7 | 0.933 | 0.871 | 0.813 | 0.76 | 0.711 | 0.665 | 0.623 |

Calculator Trick

This table can be easily made over the calculator. Let the interest rate be 1%. The steps are:

- First, convert the percentage to decimals: 1/100=0.01

- Add 1: 1+0.01= 1.01

- Now Divide 1 by the step 2 result: 1/1.01=0.990

- Now press equal to sign (=) on the calculator so many times as the number of years, and you will get the series on factors year-wise. You can match the results with the table.

- Prepare your own table as per the rate of interest.

Thus, the above concepts enable us to judge in certain terms whether it is beneficial to receive or spend money now or later. This concept is widely used for project decisions and evaluation. One can make general decisions for projects by calculating their payback period. But accurate decisions call for calculating the present value of future income so that we know the exact returns the project will give and thus can decide upon the project’s viability. Similarly, if the future value of a certain amount is calculated, it adds attractiveness to the investment proposals.

Continue reading – Present Value of Uneven Cash Flows.

Quiz on Present and Future Value