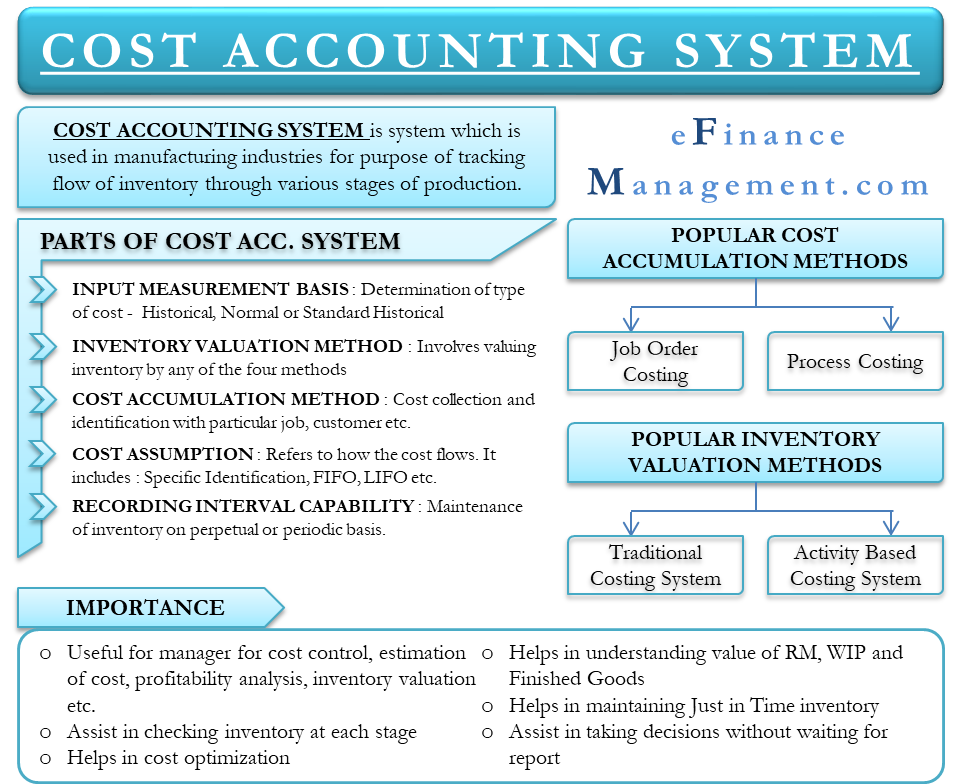

Manufacturers use cost accounting systems to keep a tab on the production activities using a perpetual inventory system. In simple words, the cost accounting system is meant to simplify the work of the manufacturers, who need to track the flow of inventory on a continuous basis through various stages of production.

Basically, a company deploys the cost accounting system to track the raw materials even before the production process begins. Eventually, these raw materials convert into finished goods in real-time. Once the raw materials enter the production, the system tracks and record the use of the materials by crediting the raw material account and debiting the goods in the process account.

For example, when raw materials move from one process to the next, the cost accounting system tracks the progress. Also, it feeds the progress in the computerized system. This helps the production managers and cost accountants to check the inventory in each stage of the production.

Parts of Cost Accounting Systems

A cost accounting system has five parts:

Input Measurement Basis

The cost accounting system starts with determining the type of costs that flow into the inventory accounts. There are three types of Input Measurement Basis – Historical, Normal Historical, and Standard Historical.

Also Read: Cost Accounting and Management Accounting

Inventory Valuation Method

This involves valuing the cost of inventory. One can value inventory in four ways – Throughput, Direct, Full absorption, and Activity-based.

Cost Accumulation Method

It primarily refers to the method by which costs are collected and identified with particular jobs, orders, customers, departments, batches, and processes. There are four ways to accumulate cost – Job Order, Process, Backflush, and Hybrid.

Cost Assumption

It refers to how costs flow through different inventory accounts. A point to note is that cost assumption deals with the flow of costs and not the flow of work. There are three types of cost assumptions – Specific Identification, FIFO, and Weighted Average.

Recording Interval Capability

A company can maintain inventory on a perpetual or a periodic basis.

Importance

- Management uses cost accounting systems to estimate the cost of the products for profitability analysis, cost control, and inventory valuation. In order to analyze whether the process is profitable or not, it is important to understand the accurate cost of products. Moreover, to plan the budget and understand the cash flow of the company, it is important to understand the products that are profitable and the ones that are not.

- It allows management to check the raw materials in each stage of production.

- It helps the business to lower the cost of the business operation by identifying and controlling relevant items. Thus, it leads to profit maximization.

- Costing system also helps understand the closing value of materials inventory, work-in-progress, and finished goods inventory for preparing the financial statement.

- Since management is aware of the inventory numbers, it is able to maintain just-in-time inventory systems. In just-in-time inventory systems, the company orders the raw material when they need it. It saves the company from storing the raw materials and thus, saves costs related to storage, security, and obsolescence.

- The real-time part also helps the management to make decisions without waiting for reports.

Popular Cost Accumulation Methods

As said above, there are four methods of cost accumulation method, but the two popular ones are;

Job Order Costing

Under the Job Order Costing system, the manufacturing costs are accumulated for each job. A company usually adopts this approach to deal with the production of unique products and special orders. Job order costing fits perfectly for an event management company, a niche category seller of the furniture, and so on.

Process Costing

Process costing accumulates the manufacturing cost separately for all processes. Businesses where the production process involves different departments and cost flows from one department to another rely on process costing. For instance, chemical producers, oil refineries, and more rely on this type of cost accounting system.

Popular Inventory Valuation Methods

There are four methods to value inventory, but the two most popular ones are;

Traditional Costing System

Under this system, single overhead rates are calculated and are applied to each job and department. One of the shortcomings of this system is that there could be unexpected expenses incurred within the manufacturing process at times. This could have a great effect on the estimations of profits.

Activity Based Costing (ABC)

Under this method, the manufacturing overhead cost is assigned to the products in a much more logical way compared to the traditional approach. In activity based costing method, the cost is first assigned to the activities that leave a direct impact on the overhead costs. After that, the cost of these activities is assigned to the products that are actually demanding the activities.

Activity-based costing also has a few drawbacks. This method is complex and expensive. Therefore, only large organizations can afford to deploy the activity-based approach to value inventory.

Cost Accounting System vs. Financial Accounting System

- Cost Accounting Systems deal with cost control and reduction. The Financial Accounting System focuses on actual and projected results, or the profit and loss statement items.

- A cost accounting system is important to the executives within the company, such as the account manager. The financial accounting results hold more importance for outside parties, such as creditors, investors, and government regulators.

Final Words

Cost Accounting Systems are useful for all kinds of business, be it manufacturing or trading products, or even a company dealing in services. There are several types of cost accounting systems available for all kinds of businesses. One can choose the best by looking for the one that best allocates costs to manufacture goods—for example, allocating by manufacturing complexity, product lines, production volume, production process, and more. Additionally, to ensure the effectiveness of the system, it is crucial that management understands the cost of production and calculate it correctly.